Irwin G. Stein is a Corporate, Securities and Real Estate Attorney, Educator and Author with more than 40 years of experience living in the United States of America. He runs his own blog (http://laweconomicscapital.com) and has written books such as „Investment Schemes, Scams & Strategies retirees should avoid“ (https://www.amazon.com/Irwin-G.-Stein-Esq./e/B0153PWMFW).

Irwin and I have been connected at LinkedIn for some time and in course of the last one to two years we had a number of heated discussions about the risk and opportunities of Bitcoin and other cryptocurrencies. Even though, I disagree with Irwin on many points of view, I respect his professionalism and enthusiasm and I consider him as competent sparring partner for discussions, that allows me to double-check and further develop my own points of view.

On March 6, 2018, Irwin published on his Laweconomicscapital.com blog an article under the headline „Bitcoin, BS and Banking“, which pretty much summarises his points of view on Bitcoin&Co including many arguments I have repeatedly seen in his postings and comments (see: http://laweconomicscapital.com/2018/03/bitcoins-bs-and-banking/). Since the article comprises some unsubstantiated allegations, which are again and again circulated in the public to unsettle inexperienced readers, I decided to write this reply. In the following you will find my comments on all statements provided in Irwin’s article. I have put Irwin’s original statements in quotation marks and numbered them consecutively from 1 to 28, so that interested readers are able to directly compare his arguments and my counterarguments with each other.

I would like to clarify ahead that I am neither a „European socialist“, nor a millennial, lawyer or financial markets expert. I hold a degree in business informatics and I have been working almost 30 years most of the time in executive positions e.g. as Head of Corporate IT Audit, CIO/CTO, Head of Business Administration, or Account General Manager for international conglomerates such as Siemens, Hewlett Packard or ThyssenKrupp. Consequently I am familiar with topics such as Governance, Risk and Compliance (GRC) paired with a strong understanding of technology as enabler, threat or disruptor for old and new business models.

My major motivation to write this reply to Irwin Stein’s article is the following: Everybody, who is interested in politics and economics, should be aware, that the global financial industry has produced a long series of asocial, immoral or even illegal machinations in course of the last 40 years – in many cases at taxpayer’s expenses with losses for the public purses in a magnitude of two- or three-digit billions or even trillions of USD not being uncommon (I will come back to this point in a minute). These machinations had and still have a very negative impact on the values, morale and stability of our societies – at least in Europe. Almost 10 years after the breakout of the last global financial crisis in 2008, many European countries – particularly the Mediterranean countries – still suffer under the aftermath of this avoidable crisis. The rise of extreme left and right wing parties in Europe as well as the election of Donald Trump as President of the United States of America are from my point of view being strongly (if not even decisively) influenced by the machinations of the financial industry and its significant consequences for middle and lower class people. Blockchain technology offers opportunities to disrupt and fundamentally change the rules of the game in this rotten system and I consider it as important to separate facts from biased opinions and unsubstantiated allegations.

Facts kill opinions. So, let’s get down to the details and compare the statements in Irwin’s article argument by argument:

- Irwin Stein: „I do not believe in Bitcoins because the whole idea behind them smacks of alchemy. For centuries, going back to classical Greece, people believed they could turn lead into gold. A great many, otherwise intelligent people spent a lot of time in this pursuit from the Middle Ages into the 20th Century. In the latter half of the 19th Century people believed that the new Industrial Age would come up with a mechanical contraption to solve every problem. There were people peddling mechanical contraptions which claimed that you could put a lead bar in one end and a gold bar would come out the other. The process or internal workings of the machine were not disclosed and they became known generically as “black boxes”.“ REPLY: Bitcoin and its underlying Blockchain technology is not a „black box“, therefore this introduction is misleading. Anybody, who is interested in this technology can understand it. As good starting points for learning, what Bitcoin and Blockchain is all about, I would offer my blogs „Crypto Assets – the most important Q&A“ published on December 23, 2017 (see: https://kubraconsult.blog/2017/12/23/cryptocurrencies-the-most-important-qa/) and „The most important facts and milestones on Bitcoin and Blockchains“ published on August 27, 2017 (see: https://kubraconsult.blog/2017/08/27/the-most-important-facts-and-milestones-of-bitcoin-and-blockchains/).

- Irwin Stein: „Today, thanks to new technology, you can buy a machine, plug it in and every so often it will send a few lines of computer code to an electronic wallet. You can then exchange that code for a lot of cold hard cash. That is exactly what a Bitcoin is, just computer code that can be replicated by a machine. They may have value today; but sooner or later those lines of computer code are more likely than not, to become worthless.“ REPLY: So what? 92% of money supply in our conventional fiat money system only exists virtually in computers, as described in my blog „Why Bitcoin&Co. are by far not the biggest issue in our global financial system“ published on November 28, 2017 (see: https://kubraconsult.blog/2017/11/28/why-bitcoinco-are-by-far-not-the-biggest-issue-in-our-global-financial-system/).

- Irwin Stein: „For these lines of code to retain value people must be willing to buy them after they are manufactured. As the price increases, more and more people will likely start manufacturing them especially if the next generation of machines are more efficient or cost less. Sooner or later there will be more code in the market than the market wants and the price will drop. That of course is just basic economics.“ REPLY: The U.S. Federal Reserve as well as the European Central Bank (ECB) have flooded the markets with trillions of USD/EUR from the printing press since the breakout of the global financial crisis in 2008. The balance sheets of both Central Banks have been blown up into a magnitude of more than four trillion USD in course of the last 10 years. In combination with the zero-interest policy of the Central Banks this has caused significant negative side effects such as bubbles in the stock and real estate markets. The external value of the Euro dropped from approx. 1.60 USD/EUR in 2008 down to 1.05 USD/EUR in 2017. As a consequence taxpayers, consumers, tenants and savers in Europe heavily suffer under the monetary policy of the European Central Bank dominated by its major intention to avoid bankruptcy of overindebted countries and business banks particularly in the Mediterranean countries of the Euro Zone. Are these huge market manipulations caused by governments and their vicarious agents a nullity from your point of view?

- Irwin Stein: „Basic economics is something that is often absent from any discussion about crypto-currency. It seems that many people who support crypto-currency, who are passionate about it and who are absolutely certain that it will prevail and disrupt the world are people who have technical backgrounds. Some of those who are most adamant in the defense of crypto-currency have backgrounds in totally unrelated fields. They gained their insight into finance by having a credit card or reading economic theory in magazine or blog articles.“ REPLY: So, what is your point here? In many cases people with strong technical background and weak financial/legal background perform discussions with people who have strong financial/legal background, but weak technical background. Would like to express, that bankers and lawyers are by default smarter than engineers? By the way, in course of my career, I have as well met lot of people, who considered themselves being a professional IT expert, after having successfully installed an App on a Smartphone. I could easily turn your argument around, if I wanted, however, since I consider this style of personal disparagement as useless and inadequate, I prefer to focus on the real arguments.

- Irwin Stein: „Most economists, including a Nobel Prize winner or two and most people who have worked in finance or banking dismiss crypto-currency as a fad. On more than one occasion, a negative pronouncement by someone with stature in economics or finance has led to the crypto-enthusiasts mocking economics, economists and anyone who has worked in finance. More than one has suggested that I and others are just too old to understand the new Blockchain technology that forms the underlying platform for crypto-currency.“ REPLY: I agree, that this happened. Maybe the reason was, that some of the statements of those economists and Nobel Prize winners were obviously based on a lack of understanding on the technical aspects of cryptocurrencies in combination with an intentionally biased description of the reality – which applies for example to statements provided by Joseph Stiglitz and Kenneth Rogoff. Independently from this assessment, I fully agree, that age discrimination should have no place in a professional discussion.

- Irwin Stein: „Blockchain is essentially a decentralized ledger. It is a method of bookkeeping where each participant to a transaction creates a record of the transaction which is matched and verified with the other participants to the transaction.“ REPLY: This definition is unfortunately incomplete. The basic architecture of the Bitcoin Blockchain comprises a ledger function with an immutable, sequential chain of records, whose authenticity and integrity is secured by means of cryptography (the records contain index, timestamp, transactions, proof and hash of previous block). Privacy is insofar protected, as personalized data are not stored in the Bitcoin Blockchain or cross-linked to the transactional data (records). Blockchain transactions are anonymous as long as the Bitcoin addresses of senders/receivers can not be connected with the personalized data. However, this connection happens outside of the Blockchain e.g. at Bitcoin exchanges/marketplaces, where users have to identify themselves with their personal ID or passport, before they are allowed to buy or sell Bitcoins. In addition to the ledger function the basic architecture of the Bitcoin Blockchain comprises a so called „mining“ function (which are basically decentralized alternating entities competing to become the timestamper and getting rewarded with an asset for the validation of transactions). Besides, there are more advanced Blockchain technologies (e.g. Ethereum), which provide so called „Smart Contract“ functionalities enabling the automatic processing of logistical and financial transactions. In the future, this will allow the development of new business models, which do not require involvement of human labor any more (think of autonomous cars which automatically charge fees to their users and automatically pay bills for energy, cleansing, inspections etc.). Today, this basic Blockchain architecture leads to some disadvantages in the practical application with higher number of users, miners and higher volume of transactions (e.g. scaling, latency, throughput). Crypto developers all over the globe are working on resolutions for these disadvantages (e.g. SegWit, Lightning, DAG, Tangle, …).

- Irwin Stein: „When I wanted to learn about Blockchain I spoke with people who are working in Blockchain at large companies and universities in the US and around the world. What they told me is that we may see Blockchain coming into various industries in the next few years. Initially they expect that it will be used in supply chain and logistics applications.“ REPLY: According to my observation the best Blockchain experts today don’t work for large companies and universities. Could it be possible, that you missed some important facts, arguments and insights by reducing the scope of your discussions to the wrong information sources? If you really want to understand the potential of Blockchain technology you have to follow the newsfeeds on specialized crypto websites, such as https://www.coindesk.com or https://cointelegraph.com and join crypto currency discussion panels such as http://bitcointalk.org, http://www.bitcoinforum.com or https://www.reddit.com/r/CryptoCurrency/ (note: an overview on the most valuable information sources is provided in my aforementioned blog „Crypto Assets – the most important Q&A“). In addition, I would recommend watching a speech held by Andreas M. Antonopoulos at the Swedish Internet Days („Internetdagarna“) conference during November 20/21, 2017 in Stockholm under the headline „Introduction to the internet of money“ (see: https://youtu.be/rc744Z9IjhY). In this speech Andreas M. Antonopoulos pointed out a couple of important factors, which illustrate, why Blockchain technology has truly disruptive potential.

- Irwin Stein: „What I do not hear from these same people is a lot of enthusiasm for Blockchain in the financial sector. FINRA assembled a panel of Blockchain experts in 2016 that looked at various functions in the financial markets that might be made more efficient by Blockchain. The overall conclusion was that Blockchain development still had a way to go.“ REPLY: Even though, I would agree to the conclusion that Blockchain development still has a way to go, there are plenty of Blockchain projects which focus on the disruption of the financial industry including its major functions such as authenticating identity and value, moving value, storing value, lending value, exchanging value, funding and investing in assets, companies and startups, insuring value and managing risks, or accounting for value. As literature for further research I would recommend Alex Tapscott’s and Don Tapscott’s book „The Blockchain Revolution – How the technology behind Bitcoin is changing Money, Business, and the World“ published in 2016. And to understand the broader context of Blockchain technology beyond Financial Services I would recommend to take a look at the presentation held by Alex Tapscott at the LendIt USA conference on March 6-7, 2017 in the Jacob Javits Center in New York City under the headline „Blockchain Revolution: Understanding the 2nd Generation of The Internet and the New Economy

„: http://blog.lendit.com/wp-content/uploads/2017/03/BLOCKCHAIN-REVOLUTION-%E2%80%A8Understanding-the-2nd-Generation-of-The-Internet-and-the-New-Economy.compressed.pdf. - Irwin Stein: „There will certainly be decentralized ledgers within various financial companies and for some financial tasks. The entire world of finance is based upon checks and balances, supervision of employees, and repeated audits. Some of that has been automated since the 1970s.“ REPLY: Please don’t underestimate the impact of triple-entry accounting. There are people who argue, that it is the most important invention in course of the last 500 years, such as Daniel Jeffries in his article published on June 22, 2017: https://hackernoon.com/why-everyone-missed-the-most-important-invention-in-the-last-500-years-c90b0151c169.

- Irwin Stein: „The financial markets need to keep the bad actors out. Decentralization does not do that. If anything it is the opposite. Blockchain verifies the transactions but not the people behind them.“ REPLY: Even though, I do not disagree to this statement, we have to acknowledge, that the global financial industry produced in course of the last 40 years a long series of asocial, immoral or even illegal machinations – despite all control and regulation efforts and in many cases at taxpayer’s expenses. Major examples are the burst of the US Subprime bubble in 2007/08 caused by interlaced derivative „securities“ with falsified ratings, the Asian crisis in 1997/98 caused by Hedge Funds speculating agains the Thai currency Bath, provision and management of illegal or at least immoral tax shelter schemes with or without tax havens, deliberate bypassing of laws with cum-ex and cum-cum trades to obtain multiple reimbursements for taxes, which were only paid once. A more comprehensive list is provided in the following blog under the headline „Why the global financial industry must be regulated and enchained“: https://tivot.blog/2018/02/10/why-the-global-financial-industry-must-be-regulated-and-enchained/ and I would recommend to carefully read it since it illustrates, why an increasing number of ordinary people does not trust the financial industry and Central Banks any more.

- Irwin Stein: „A decentralized system prides itself on anonymity and anonymity invites bad actors. If you read what the regulators of the banking and financial markets around the world have published, they continually share two main concerns about crypto-currency; money-laundering and tax avoidance.“ REPLY: Do you seriously believe, that criminals will preferable use Blockchain technology as major vehicle for their illegal transactions, despite every transaction is immutably recorded, transparently made available for the entire network (including prosecution authorities) and can be tracked and traced by anybody who is interested? At latest, if these criminals tried to change the huge amounts of cryptocurrencies back into US-Dollar or Euro, they would put themselves at a high risk to get caught.

- Irwin Stein: „Crypto-defenders will argue that far more money is laundered through banks. Banks spend a lot of money trying to curtail money laundering. The crypto-industry spends virtually nothing. The fact that there are other ways to launder money is no excuse for the creation of a new system that makes money laundering easier.“ REPLY: Indeed, much more fraud and other crime happens in US-Dollar than in any other virtual/conventional currency and the same applies for tax avoidance. The global amount of money bunkered in tax havens or the capital managed by the shadow banking sector is by three-digit factors higher than the market capitalization of Bitcoin (currently €195 billion at a Bitcoin price of approx. $11,500). Besides, the giant volume of $544 trillion to $1.2 quadrillion of derivatives, i.e. financial bets on underlying assets, is a bigger threat for the stability of our global financial system, than Bitcoin most likely ever will be – see: „Why Bitcoin&Co. are by far not the biggest issue in our global financial system“ (see: https://kubraconsult.blog/2017/11/28/why-bitcoinco-are-by-far-not-the-biggest-issue-in-our-global-financial-system/).

- Irwin Stein: „In the past few months banks, bankers, stockbrokers and serious investors have all given the thumbs down to crypto-currency. Recently the large credit card companies announced that their credit cards can no longer be used to purchase crypto-currencies. The largest stock brokerage firms will not purchase crypto-currency as an investment for their customers. Most professional investment advisors realize that they cannot purchase crypto-currency for their clients and satisfy their obligations as fiduciaries.“ REPLY: I am not sure, which news sources you follow, however with an increasing frequency I read in newspaper reports that Goldman Sachs or even Jamie Dimon’s JP Morgan Chase & Co. start their own experiments with cryptocurrencies and Blockchain technology. As you probably are aware, Bitcoin futures opened for trading on the Cboe Futures Exchange, LLC (CFE) on December 10, 2017. Cboe was joined by CME Group, which launched Bitcoin futures contracts on December 18, 2017. In fact, the financial industry establishment cannot afford again a year such as 2017, where investors and soldiers of fortune were able to earn with Bitcoin much more money than it was possible with any other traditional investment.

- Irwin Stein: „Part of the reason is that the crypto-currency industry itself cannot decide if crypto-currency is a security, commodity, currency or a whole new asset class. There is so much divergent opinion within the crypto-community that anyone who reads a few dozen articles on the subject is likely to be confused rather than enlightened.“ REPLY: The reason for this supposed confusion is very simple: There are various kinds of Blockchains (see bullet point no. 6), which determine the functionality, potential use cases and subsequent classification of the cryptocurrency utilizing the underlying Blockchain technology. Most interesting are from my point of view the use cases where cryptocurrencies have the character of a new asset class, which enables decentralized applications. Adam Ludwin (Founder&CEO of Chain.com) has published an interesting blog on October 16, 2017, under the headline „A letter to Jamie Dimon – and anybody else who is still struggling to understand cryptocurrencies“: https://kubraconsult.blog/2017/11/27/a-letter-to-jamie-dimon-and-anyone-else-still-struggling-to-understand-cryptocurrencies/.

- Irwin Stein: „Much of that divergent opinion is caused by the fact that these are legal definitions being interpreted by non-lawyers. I will not apologize for thinking an opinion written by a non-lawyer with a technical background living in Europe, Asia or Australia about how something should be defined under US law should carry little weight.“ REPLY: See my reply to your Point no. 8. To discredit discussion partners whose arguments cannot be refuted is a discussion style usually applied by Marxists and Leninists as part of their dialectic method.

- Irwin Stein: „That does not stop the crypto-community from hanging on the word of every hack with a keyboard who holds himself out as a crypto-expert. For an industry barely 2 years old, there are enough people holding themselves out as “crypto-experts” to fill Yankee Stadium at least once, perhaps more.“ REPLY: I do not disagree to your point of view, however, this seems to be a common pattern of every new hype including dot.com in 1999/2000, Social Media from 2008 onwards, etc. pp.

- Irwin Stein: „If all was well in crypto-land I would never have heard about Tether. Tether is a crypto-currency that is exchangeable into US currency at a fixed rate. It claims to have a cash reserve of $2 billion to back up each and every Tether coin that has been issued. People have questioned whether the owners of Tether really have secured $2 billion and the owners have repeatedly refused to respond with simple proof that the $2 billion is there. In any legitimate industry this question would never have to be asked more than once.“ REPLY: According to my understanding, the Tether case is still pending and the respective investigations are ongoing?! From a lawyer, as you are one, I would expect to consider a defendant as innocent until he is convicted.

- Irwin Stein: „Theft and fraud are rampant in the crypto-currency world. Electronic wallets are routinely hacked. Estimates run as high as 10% of the money sent to ICOs may have been hacked from the ICO’s wallet and hundreds of millions of dollars have been stolen from the various secondary market exchanges where the crypto-currency is traded.“ REPLY: At first, we have to differentiate between the Bitcoin Blockchain one the one hand and Bitcoin exchanges/marketplaces on the other hand. In course of the last 9 years since its release nobody was able to hack the Bitcoin Blockchain mainly due to its smart decentralized architecture and the cryptograhic protection mechanisms. Full stop. Some Bitcoin exchanges/marketplaces, which have IT systems based on conventional database and web technology, were hacked, which is undoubtedly bad. However, you can easily protect your Bitcoins by utilizing offline Wallets such as Ledger Nano S or paper Wallets. In addition, I am not aware of any comprehensive and substantial representative study, which proves or disproves the „estimates“ in your statement above. We are so far lacking sufficient data for a meaningful discussion about this issue.

- Irwin Stein: „Fund raising using crypto-currency (ICOs) has reached a fever pitch and has attracted a significant amount of scoundrels. Very few ICOs fund projects that are worthwhile ventures and most cannot be considered worthwhile investments by any stretch of the imagination. Telling the whole truth about the venture being financed is becoming the exception rather than the rule. Following existing laws regarding investment offerings is an anathema to the crypto-industry.“ REPLY: The first ICO was held by Mastercoin on July 31, 2013. Approximately 500 people invested about 4,700 Bitcoins in the project, which by December 2013 was worth about $5 million when Bitcoins price-surged from about $100 to $1000. Interestingly the majority of ICOs between 2013 and April 2017 took place outside the U.S., as the following animation provided by Elementus.io illustrates quite nicely: https://elementus.io/blog/token-sales-visualization/. U.S. based ICOs caught up from May 2017 onwards. Even though I understand and support the rationale behind the SEC regulations D and A+ for sale of securities, I recognize that these regulations cause administrative burdens and lengthy processes, which some founders of startups and small companies simply cannot afford. An ICO requires in its minimum setup an ordinary webpage and a Blockchain address, whereas sale of securities under SEC regulation D and A+ causes cost of $50,000, if I recap our most recent discussion correctly. Beyond the cost and effort, ICOs based on Blockchain technology enable crowdfunding based on micropayments (e.g. 5 million stakeholders, who „invest“ or donate 10 Cents each for a project, a startup or for needy persons). Finally, the traditional startup funding scene is dominated by Venture Capital or Private Equity firms with banks in back. There are entrepreneurs, who don’t want to be dependent on this setup and prefer a direct collection of funds from investors or donators without middlemen. What is wrong with this approach, as long as these entrepreneurs are serious and reliable and comply to the commitments given to their investors?

- Irwin Stein: „On more than one occasion an ICO has listed someone as an advisor who has never heard of the company or never agreed to be an advisor. I know this to be true because a few months back someone alerted me that my picture had been included in an ICO offering even though I had not given permission for the company to include it. This actually happens way too often. There was actually one ICO that was so brazen that the people behind it raised a few million dollars and then took down their website leaving only the picture of a phallic symbol. The people who invested in this ICO got the shaft in more ways than one.“ REPLY: The behaviour of the ICO providers in both cases is bad and condemnable without any restriction. However, this kind of bad or illegal behavior is neither characteristic for ICOs, nor limited to ICOs. In course of the last two years I had to cope with fraud several times: An Energy Supply company received my annual electricity fee and went bankrupt some days later, I bought and paid a gold coin via EBay from a scammer, who did not possess the coin, and I was victim of credit card fraud several times. Do I condemn all Energy Supply companies, EBay and AMEX due to these bad experiences? No, I don’t.

- Irwin Stein: „What I find most ridiculous about crypto-currency advocates is their overwhelming dislike for banks and their absolute but incorrect belief that crypto-currency and Blockchain will replace banks and send them to the rubbish heap of history. Some of these people are European based Socialists who have always hated banks, which is their prerogative. But they have unsuccessfully been trying to supplant banks since the French Revolution. Blockchain is not going to help them.“ REPLY: As mentioned in my reply to your Point no. 10 the global financial industry has provided numerous reasons for criticism in course of the last 40 years – see: „Why the global financial industry must be regulated and enchained“: https://tivot.blog/2018/02/10/why-the-global-financial-industry-must-be-regulated-and-enchained/. What do you expect from John Doe? Shall he shut his mouth and quietly accept the neverending asocial, immoral or illegal behaviors of the global financial industry including at least one major financial crisis per decade and the subsequent negative impact on public debt and tax burdens? How can it be that the financial industry’s profits exclusively flow into shareholders‘ pockets and losses are socialized to John Doe on a regular basis?Almost all of the major instruments for short-term speculations or other financial manipulations with negative impact on our societies have been invented, introduced or at least misused and perverted in course of the last 45 years as consequence of fateful deregulations approved by the US-Presidents Carter, Reagan, George Bush, Clinton and George W. Bush and various political leaders in Europe (e.g. Margret Thatcher, John Major, Tony Blair, Helmut Kohl, Gerhard Schröder). The financial industry utilized the massively expanded leeway provided by this deregulations by introducing, upgrading or broadening various instruments for short-term speculations or other financial manipulations such as high-frequency trading, short-selling, hedging, speculations with commodities or against currencies based on long and short equity models, Credit Default Swaps (CDS), Asset Backed Securities (ABS) including Collateralized Debt Obligations (CDO), tax-avoiding transactions with Offshore Centers and so on. All the listed instruments are neither God-given, nor will the global financial system collapse if these instruments become strictly regulated or even prohibited. In contradiction: A significant simplification of the global financial system and its instruments in combination with a harmonization and simplification of our tax systems will have a healthy and positive effect on our global economy. Our global economy should by no means be a playground for unscrupulous gamblers and bettors. People, who want to gamble and bet, should satisfy their lucid drive in a gambling house with their own money and at their own risk and not at the account of taxpayers.

- Irwin Stein: „Other people hate banks because they assert, incorrectly, that banks were the cause of the stock market crash in 2008. I do not know of a single instance of a bank putting a gun to someone’s head and making them take out a loan that they could not afford to repay. The real estate bubble that preceded the crash might better be laid at the feet of the thousands of real estate brokers who encouraged people to buy homes with the foolish notion that real estate always goes up in value.“ REPLY: So the victims are responsible for the crimes? Interesting statement from the pen of a lawyer. Just for your information: German investors lost $600 billion in course of the market crash in 2008 mainly because they bought junk derivatives with a falsified A rating from US banks..

- Irwin Stein: „The most vocal group of bank haters seems to be millennials who have very little experience dealing with banks, but who constantly tell me that they do not trust them. They tell me that banks charge too much and that the world needs better platforms to make payments.“ REPLY: First of all, millennials do not understand that emails can be sent around the globe within seconds free of charges, whereas money transfers via banks usually last some days and/or cost a significant amount of fees – although in both cases just bits and bytes in computers are being transferred. And even though I am a baby boomer, I fully understand and support this point of view. In addition the millennials in Europe have been grown up in a decade where one crisis was followed by another: public debt crisis, banking crisis, Euro crisis or at the moment the refugee crisis. Unemployment rates of young people in the Mediterranean countries are above 20%. Isn’t this reason enough to develop a critical attitude towards the established system, in which banks and currencies play a deciding role?

- Irwin Stein: „A payment platform like PayPal works quite well and is a big step up from the way banking worked 20 years ago. All it actually does is move money from my bank to a vendor’s bank quickly. Blockchain may make these payments systems better and faster.“ REPLY: As already mentioned, PayPal, Western Union, AMEX or VISA may provide reliable systems, however the fees they charge to either customers or suppliers are far too high. In addition, if you want to transfer money from your PayPal account to your bank account, you usually have to wait one day until the money is booked on the receiving account.

- Irwin Stein: „I think these advocates will be disappointed to find that banks will ultimately take the best Blockchain has to offer and utilize it in such a way as to fire significant numbers of employees and make more money. Blockchain may actually strengthen the banking industry rather than displace it.“ REPLY: This may indeed happen, however, experience shows that large dinosaurs have a limited ability to innovate with adequate speed and agility. How did U.S. Mail and other companies with business models based on traditional paper mail react, when email and messaging services came up? Platform enterprises, such as Google, Apple, Facebook or Amazon have impressively proven, that „nobodies“ are able to disrupt whole industries starting from zero within timeframes of 5 to 15 years. In case you are interested in digital business models and platform economy, please have a look at my blog of the same name published on November 4, 2017: https://kubraconsult.blog/2017/11/04/digital-business-models-and-platform-economy/. The better is the enemy of the good and time will show, who finally wins the competition.

- Irwin Stein: „The problem with the idea that crypto-currencies will replace banks is that banks do a lot more than just facilitate payments. The primary function of banks is to aggregate and intermediate capital. Banks take deposits from a lot of people and use the funds to make loans to small businesses and to make mortgage loans to homeowners. The consumer side of these transactions can be done with a peer-to-peer approach and an app. You can apply for a small loan or a mortgage from your smart phone, but you are still borrowing from a pool of money held at a bank.“ REPLY: See my reply to your Point no. 8. I would really recommend you reading Alex Tapscott’s and Don Tapscott’s book „The Blockchain Revolution – How the technology behind Bitcoin is changing Money, Business, and the World“, which clearly shows, that your understanding is at least questionable.

- Irwin Stein: „Banks also make large loans. On any given day General Motors or Dow Chemical may float a bond issue to borrow a few hundred million dollars. On the same day the State of New York may float a bond issue to fund a highway or bridge project or new university dormitory. There may be a hundred or more of these large loans and bond financings taking place around the world every day. It is not likely that these large complicated financings will ever be done with an app on a smart phone. These bonds are sold to syndicates of commercial banks. This requires that capital be pooled and that large entities have control over those pools of capital. Bank depositors do not decide how the bank invests the money they deposit. This is the antithesis of the decentralized world envisioned by crypto-enthusiasts. In their world, the crypto-currency is held in electronic wallets over which only the owner has control. No banks or centralized entity has access to those crypto-funds. There are no banks or similar entities to pool those funds and make the large loans upon which the global economy depends. Crypto-enthusiasts have no answer to how these large loans might be made in a decentralized financial world. They do not care that banks evolved to where they are because of the need for large loans to fund large companies and large projects.“ REPLY: Bitcoin was introduced on January 3, 2009 (< 10 years ago), and the first ICO took place on July 31, 2013 (< 5 years ago). Which good things with remarkable benefit for the society were financed by The Bank of New York Mellon, the State Street Corporation or the Manhattan Company in the first 5 to 10 years after their foundation in the 18th century? Let’s be fair and compare apples with apples. Crypto Assets are still in their childhood, where teething problems shouldn’t be a surprise at all and where you are usually not able to predict, if the grown-up child will become a lawyer, a banker or an engineer. In fact, the core of the discussion is not decentralization versus centralization. The core of the discussion is the question: Who controls our financial and money system? Why don’t you mention in context of your „large loan“ argument the money creation privilege of banks, i.e. the fact that banks do not at all only lend money, which they have collected from other savers or investors? On the contrary, in course of lending transactions banks do generate capital which didn’t exist before.

- Irwin Stein: „The US capital market is not a stodgy outdated system screaming for reform. It is a large, dynamic system that handles trillions of dollars of transactions every day. Virtually every transaction settles with every party happy. It is way past time for the Blockchain industry to leave crypto-currency and the bank-haters behind and to focus on the applications for Blockchain in existing financial institutions and other industries.“ REPLY: Do you understand under consideration of all information provided above, that people like I may have a totally different perception of the global financial industry including the US capital market? The biggest value add of Bitcoin&Co. is from my point of view, that they motivate people to start asking the right questions about the shortcomings of the established financial system as well as about fiat currencies, such as US-Dollar and Euro. Most of the allegations against cryptocurrencies apply as well for the established financial system and the existing fiat currencies and it can only be healthy if this insight finally diffuses into the awareness of the public. The core of our dispute is the question, who will have the power and control over our financial and monetary system in the future. This is obviously the major reason why the allegations are so strident and the pushback of the establishment is so hard (Jamie Dimon and Augustinus Carstens send their regards).

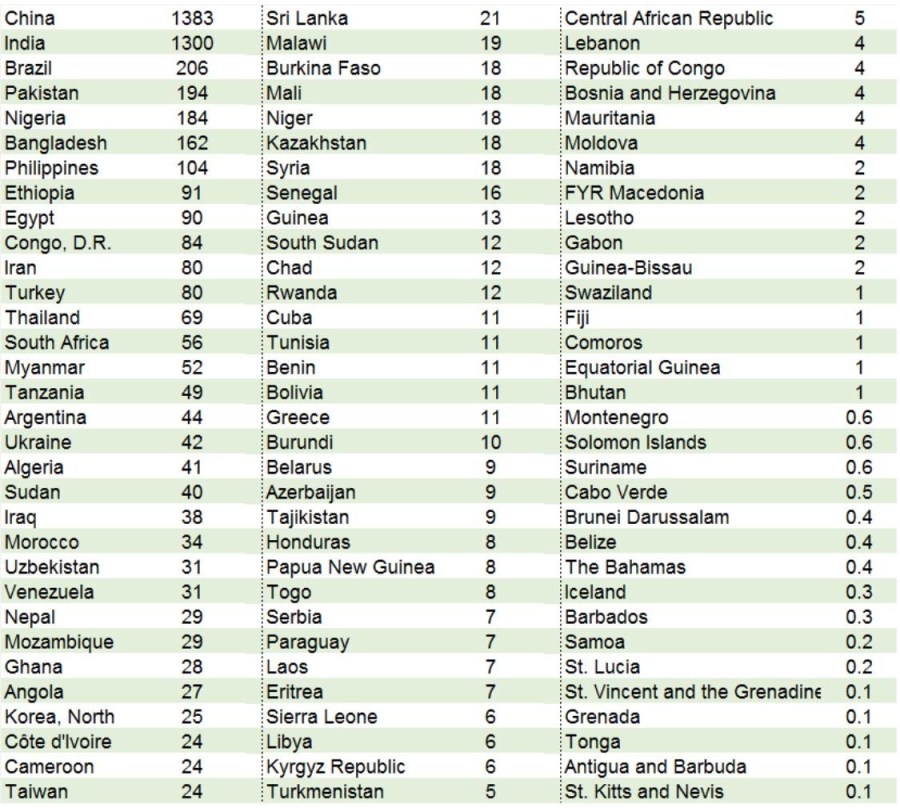

Finally I would like to mention one aspect, which is totally missing in Irwin’s article. In the following chart you find a list of countries with capital controls in order of size of their populations based on data of the International Monetary Fund (IMF) and the United Nations.

The chart shows that as of October 2016, some 5.1 billion people in 96 countries – almost 70% of the world’s population – had very limited access to money/capital, which is often due to exploitative political systems (many have no ability to even get a bank account). Even in countries without major capital controls, such as in the US, Germany, Japan etc, citizens do have restrictions. Particularly cash payments are very restricted by thresholds in an effort to limit money laundering, terror financing and tax avoidance and penalized with high fees. While use of cash for such nefarious purposes may be a very small part of the over all economy, these type of restrictions also unfairly affect regular honest individuals. Blockchain-based solutions have the potential to include the aforementioned 5.1 billion people into the financial system and protect them against government surveillance and oppression.

P.S.: If anybody – besides Irwin Stein – should read this text, please feel free to leave your point of view on this discussion as a comment.