NOTE: This blog has automatically been translated with Google Translation Service (http://itools.com/tag/translate) from the German original, which was published on September 6, 2017. I have manually double checked and refined the automatic translation of the blog. The blog comprises hyperlinks to a number of subordinated documents mostly in German language (e.g. newspaper articles), which have automatically been translated by Google Translation Service as well. Please note, that I have not adjusted the translation of these subordinated documents.

START OF BLOG

This blog offers a detailed and comprehensible introduction to digital business models and platform economy as well as their socio-economic consequences. Following the definition of the terms, I will address various aspects of digitalization and digital transformation, such as necessary paradigm shifts, market capitalization as a strategic weapon of platforms and „unicorns“, strategies in competition with platforms, the downsides of data-driven business models, including the impact on the protection of privacy and intellectual property, the Internet of Things as an essential framework condition for the data economy, and digital transformation and innovation strategies.

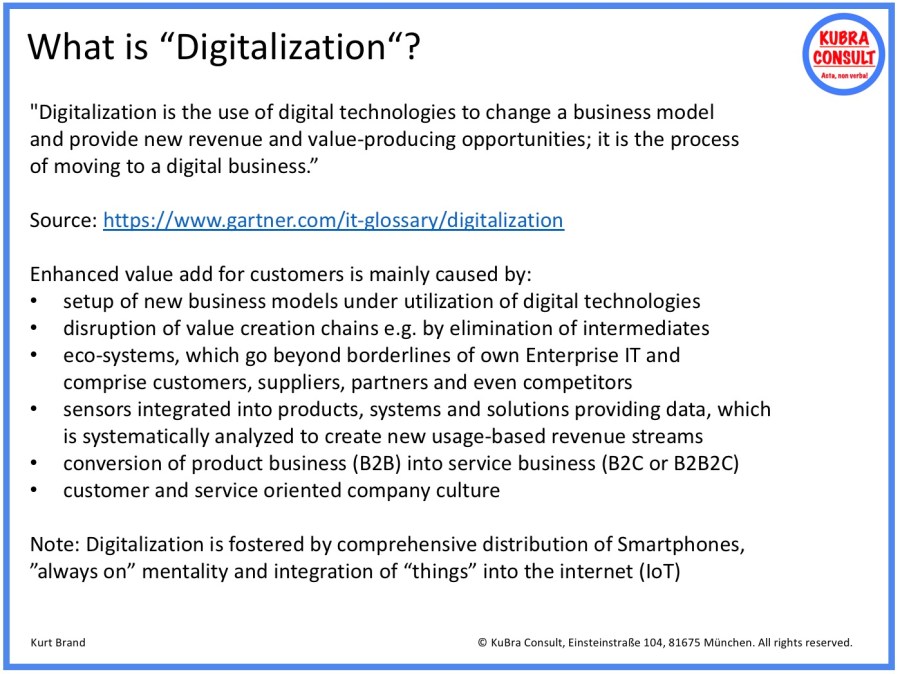

Before you can think about „digital business models“ or „digital platforms“, you first have to agree on what you want to understand by „digitalization“ or „digital transformation“. Gartner provides the following short and comprehensible definition: „Digitalization is the use of digital technologies to change the business model and provide new revenue and value-producing opportunities; it is the process of moving to a digital business“.

Note: Digitalization is not just about the use of information technology to manage data or to support business processes, but about the development of new business models. The widespread adoption of smartphones, the „always on“ mentality and the increasing integration of „things“ into the Internet are the basis for new digital services and their increasing distribution.

These basic ideas can be read, inter alia, in a CIO.de article published by Oliver Janzen (CEO of DST consulting) on April 1, 2016 in German language under the headline „Transformation needs target images: Digitalization – The Big Picture“ (see: https://www. cio.de/a/digitalisierung-das-big-picture.3255348).

The difference between „Digitization“, „Digitalization“ and „Digital Transformation“ is explained in the following chart:

The next chart provides an extract from my blog published on January 20, 2017 under the headline „What can the digital champions of tomorrow learn from Apple, Google, Amazon, Facebook & Co.“ (see: https://kubraconsult.blog/2017/04/28/what-tomorrows-digital-champions-can-learn-from-apple-google-amazon-facebook-co/). It names patterns and principles used by Digital Champions to build up successful digital business models and platforms:

In addition, my blog published on March 24, 2017 provides an outlook on the foreseeable or possible „socio-economic consequences of digitalization“. It intends to give you an impression of the immense scope of the changes resulting from digitalization, automation and robotization (see: https://kubraconsult.blog/2017/03/17/the-socio-economic-consequences-of-digitalization/).

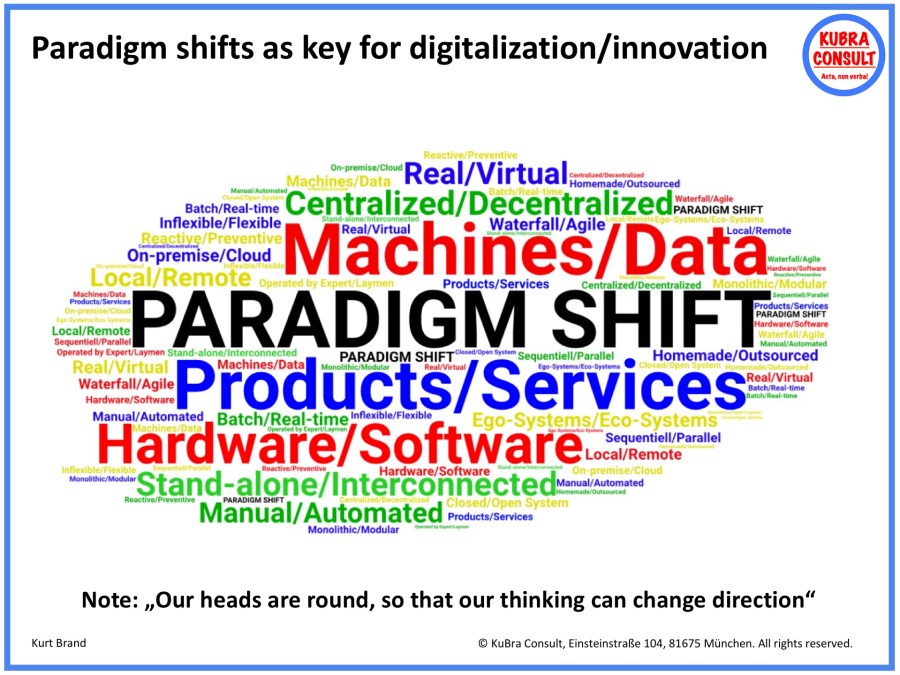

An essential prerequisite for the implementation of such fundamental changes is often the letting go of popular traditional patterns of thought in favor of new, innovative patterns of thought in the course of a paradigm shift. Some important examples are shown in the following graphic:

The following questions could be a good starting point for owners of linear business models when entering the field of digitalization and digital transformation:

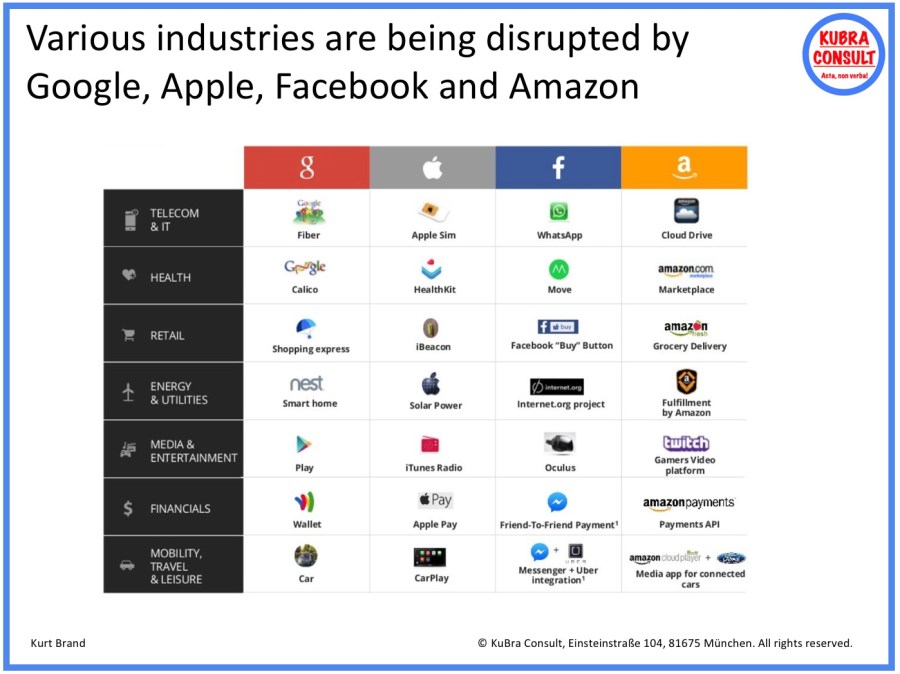

On the basis of this understanding we will devote ourselves in the following to the Digital Platform Economy. Digital Platforms are not just well-known brands that have conquered the world in recent years, such as Apple with the iPhone and iTunes, Google with its search engine and the mobile Android operating system, Amazon with its online retail platform for digital mail order business or Facebook with its social media platform. There are significant differences between conventional („linear“) business models and digital platforms, which the founders of „The Platform Innovation Kit“ described very well in the following summary:

Digital Platform Economy is therefore primarily about the development of companies from the conventional paradigm of „my“ product or „my“ service to becoming an intermediary and coordinator of various partners (customers, suppliers or even competitors). The key mission of a platform company is no longer to develop or optimize new products, but to organize transactions between the partners involved, in a way that benefits all partners embedded into „value creation networks“. Digital platforms are important growth and innovation drivers as they change market access.

The following example may illustrate the huge impact of this change in market access for the balance of power between suppliers, platform owners and customers: One of the main reasons for Amazon’s success is its role as a distribution platform for third-party retailers. If you want to sell larger quantities, the market power of the Americans means that you can hardly avoid a listing on the Amazon platform. The third party retailers can thus achieve significantly more sales, but has to deliver Amazon for better or worse. Since Amazon has all relevant customer data under its control after listing, it can temporarily easily undercut third-party retailers and ultimately take over their business completely if it fits into Amazon’s strategy. In addition the broad variety of third-party transactions provide Amazon with a huge amount of data, which they can utilize as excellent lever for predicting, controlling or even manipulating the behavior of customers and suppliers in Amazon’s interest. As the platform operator, Amazon becomes the spider in the web.

This means indeed, that – as direct interface between manufacturers and customers (or users) – digital platforms question processes proven for years and change entire industries at breathtaking speed. And the platform economy does not stop at country or industry boundaries.

The goal of the digital platforms is the ultimate control of end user access. To do this, they use different access channels (today: browsers, devices, operating systems; in the future: voice assistants such as Alexa, Siri, Cortana or Google Home, televisions, control units of cars, virtual or augmented reality applications).

The business models operated on these channels are partly in competition with traditional business models. Classical, analog models are defeated by digital platforms if they are unable to establish or maintain their own stable customer access. In particular, access to the end customer is, as in the analogue world, the decisive key.

The world is becoming increasingly digital. Decisions are thus made digitally and previously analogue-controlled customer accesses lose relevance. The chart below shows how digital platforms in all areas of life attempt to gain control.

Note: I have taken this graphics from an excellent article published by Alexander Graf (kassenzone. de) on February 15, 2017 under the headline „Amazon, Facebook and Apple: The basics of platform economics“ in German language on t3n.de (automatically translated version see: https://goo.gl/Quy7Rh). The article deals primarily with the effects of digital platforms on trade.

Dr. Holger Schmidt of Technical University (TU) Darmstadt puts it this way: „Platforms are the central business model of the digital economy. The companies put themselves successfully as mediators between providers and buyers and act as a „matchmaker“ like a lubricant for the economy, thereby expanding existing markets or even create entirely new markets: Google as a search engine brings together providers and demanders of information that otherwise only with a much higher search effort or maybe never found each other. Airbnb as a room broker brings together private apartment providers and travelers who previously knew nothing about each other.

That sounds simple, but it is highly disruptive: platforms replace the „invisible hand“ (Adam Smith) as the organizational principle of a market. With the drastic reduction in transaction costs and the resulting enormous popularity among consumers, the welfare gains in the platform economy shift from producers to consumers and the platform operator. The four largest platforms alone (Alphabet, Amazon, Facebook, and Alibaba) are now worth more than all German DAX30 companies that still largely work on the losing pipeline model“ (see: https://goo.gl/R6Pd2j).

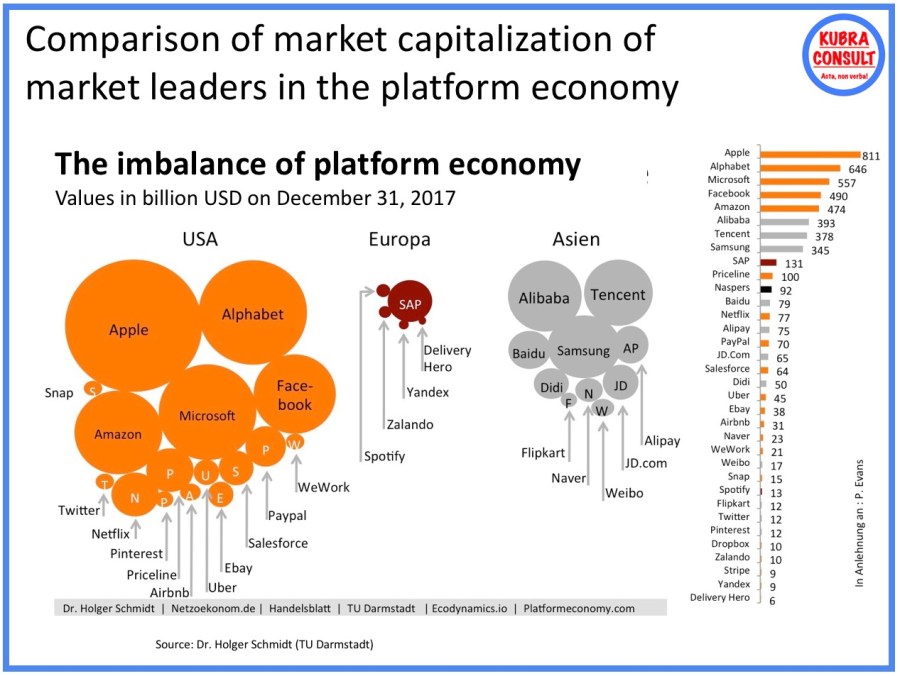

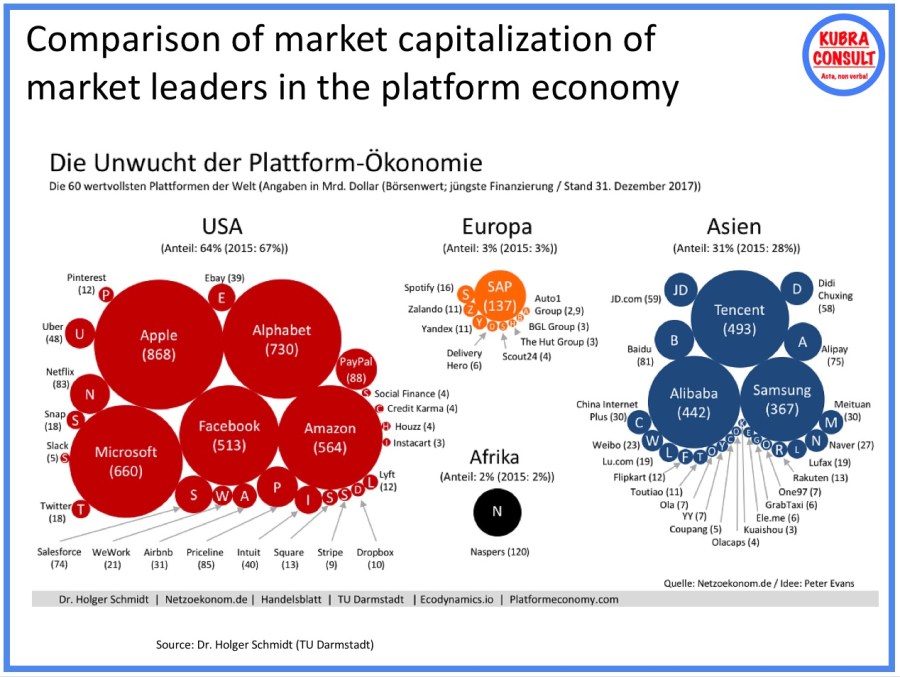

With kind permission of Dr. Holger Schmidt, I use the following chart in which he compares U.S., European and Asian companies that are market leaders in platform economy, and have the highest market capitalizations and company valuations:

One sees at first glance that the market capitalizations of U.S. companies are significantly higher than those of Asian companies. With SAP as the only company with a noteworthy digital platform, the Europeans are far behind in third place. Note: The raw data on which the chart was generated and a wealth of additional in-depth information can be found in Peter C. Evans’s study „The Rise of the Platform Enterprise“ published in January 2016 (see: https://goo.gl/y3ze1H). An updated version of the chart above illustrating the 60 most valuable global platforms as of December 31, 2017, is provided here:

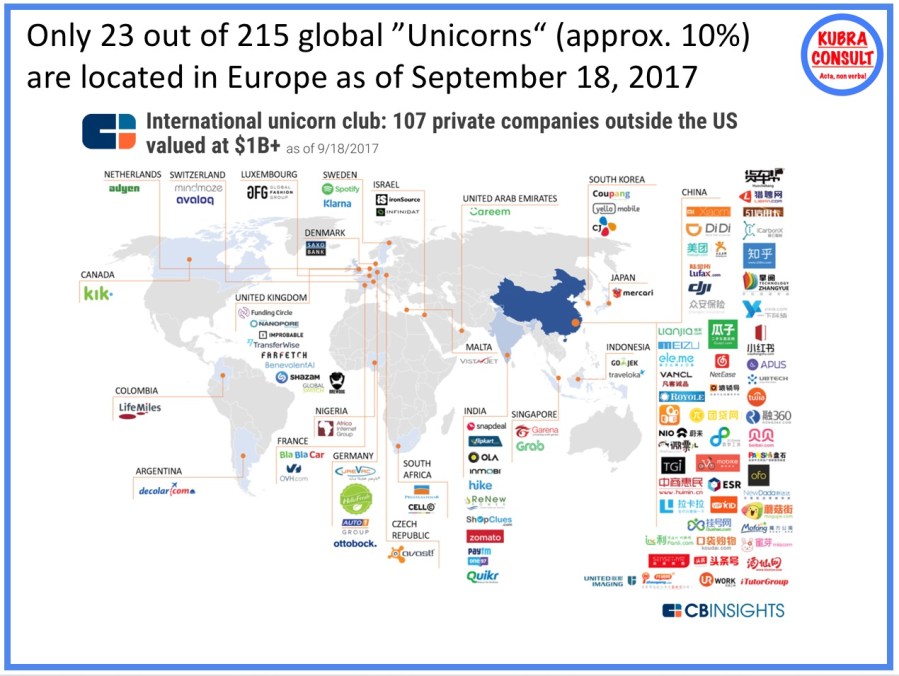

The same picture as for the market leaders of the platform economy arises, if one looks at the current distribution of the so-called „Unicorns“ – these are companies (usually startups), which have yet to show any special success, but already have reached market capitalization of 1 billion USD or more. According to a recent survey by CB Insights (as of September 18, 2017) of 215 global „Unicorns“ only about 10% or 23 companies are located in Europe (of which just 4 are located in Germany, so the fourth largest economy in the world).

The market capitalization or the company valuation of start-ups is a success factor that should not be underestimated when developing platforms. One may shake the head over the sometimes irrationally high company valuations of U.S. „digital champions“: The electric mobility provider Tesla had for example with $ 55 billion in July 2017 a larger market capitalization than the Ford Motor Company; U.S. carpool mediator Uber was valued at $ 68 billion in a 2016 round of financing, although the company will accumulate a cumulative loss of approximately $ 3.0 billion seven years after its creation in the four quarters of fiscal 2016/17.

BUT: You should still be careful not to underestimate the importance of these extreme company ratings for the success of the young companies, because they are part of the concept of success – the madness has, so to speak, method: Uber can burn with its carpool mediation $ 3.0 billion per Year over 20 years and accumulate a cumulative loss of $ 60 billion. If Uber is able to collect $ 68 billion from other investors in course of an IPO, its venture capitalists still make a lot of money. And if a venture capitalist ever invests $ 10 million in 1,000 startups, one single „Uber“ is sufficient to recoup his $ 10 billion in venture capital. That according to experts, 90% of startups fail (see: https://goo.gl/ANj1Nm), therefore plays no crucial role.

Partly because of this logic, startups in Silicon Valley in California / USA have 10 times more risk capital (venture capital) available than in Germany: In 2015, the startups in Silicon Valley have received $ 34 billion from venture capital companies in the region for approximately 2,000 Deals, while start-ups in the DACH region (comprising Germany, Austria and Switzerland) received just $ 3.9 billion for approximately 374 deals (see: https://goo.gl/BEbKJX). In 2016, the venture capital financing volume in the DACH region even fell by almost a third (see: https://goo.gl/cQimgz).

Another important success factor of digital business models or platform companies is their „scalability“. In the digital economy this describes the increase in sales without an increase of fixed costs, e.g. by continuous investment in production or infrastructure (see: https://goo.gl/Wbpt3A). There are several digital business models that have a positive impact on scalability, such as: Software as a service (SaaS), streaming services, publishing subscriptions or online memberships – the bandwidth is diverse. Recurring payments and memberships, that generate Monthly Recurring Revenue (MRR) for the provider, have now reached consumers. These digital business models lower the barriers to entry for the customer by avoiding large initial investments (e.g., to buy a software or a car) and paying only what they need and what they use. In addition, short notice periods and flexible pricing models increase the attractiveness of these digital business models.

From the vendors‘ point of view, digital business models with continuous monthly payments offer a high degree of predictability for business development: Monthly Recurring Revenue and the associated stable cash flow help to plan resources expediently and in the long term. The termination rate can provide information about the „Customer Lifetime Value“ and thus form the basis for future investments in customer acquisition. Only those who know how much a customer is worth can plan expenditures per customer meaningfully and thus generate sustainable growth. The biggest challenge is the measurability of all data as well as the correct evaluation.

So, is the success of Platform enterprises such as Amazon, Facebook or Google inevitable? Or are there counter strategies, which enterprises with linear business models selling goods and services or governments with less advanced economies can apply to survive in the era of globalization and digitalization? Are Platform enterprises invincible or are there threats, which can affect even the business of „digital champions“ in a negative way?

The following chart is a first draft comprising potential threats and counter strategies in the competition between enterprises with linear business models and platform enterprises. Feedback to further develop and improve this collection of material is – as always – more than welcome.

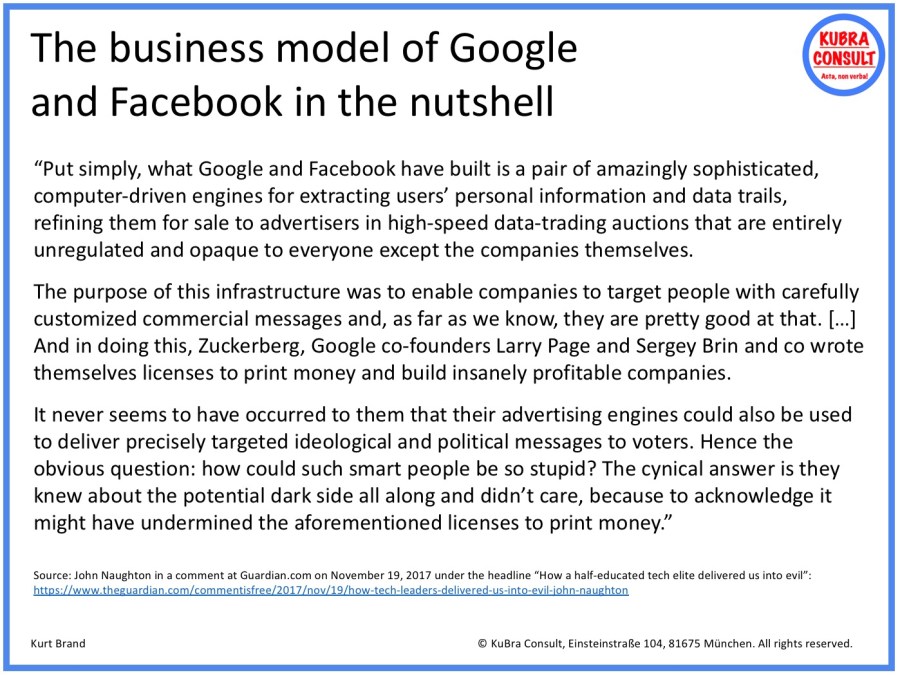

Now follows a very important insight: Every user should understand, that the superficial purpose of a platform company is not necessary identical with its effective purpose. It is certainly not Google’s mission to organize a user’s access to the world’s information, just as little as it it Facebook’s (or LinkedIn’s) mission to organize the user’s networking with other people. The following citation form John Naughton’s excellent comment published on November 19, 2017 in the British Guardian under the headline „How a half-educated tech elite delivered us into chaos“ brings this to the point (source: https://www.theguardian.com/commentisfree/2017/nov/19/how-tech-leaders-delivered-us-into-evil-john-naughton):

Of course, the vast majority of companies on planet earth wants/needs to make profit, however in case of data leeches, such as Google and Facebook, you have to look a little closer to understand their business model.

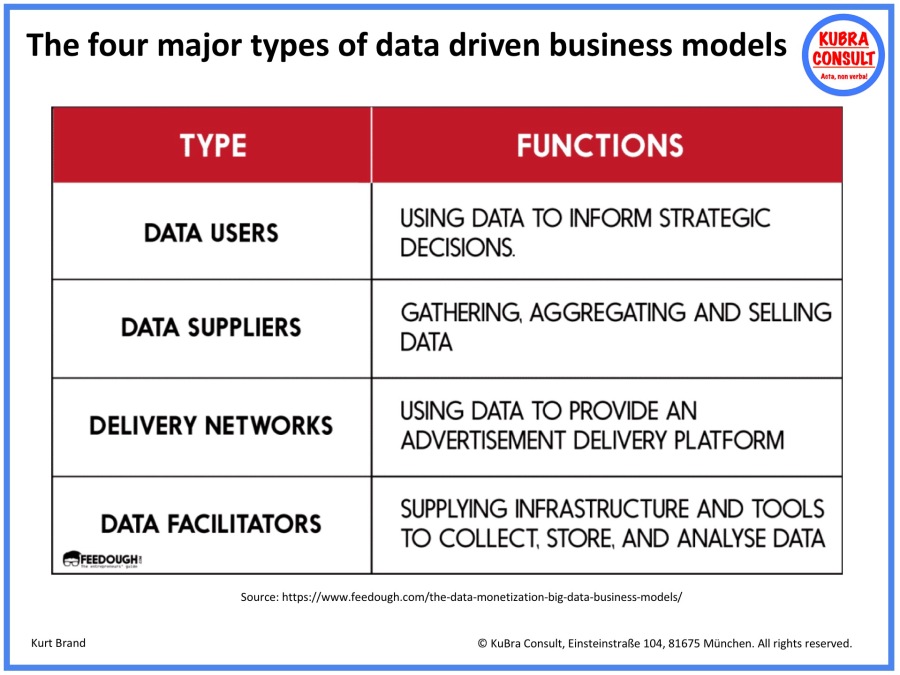

The following chart is taken from a Feedough.com article published by Aashish Pahwa on April 2nd, 2018, under the headline „The data monetization – Big data business models„. In this article he states: „“According to a research, investment in big data will be around $76 billion and 1.7 MB of data will be created every second for every person on earth in 2020. Thanks to the internet of things, we already have smart shoes, clothes, refrigerators, washing machines, and not to forget – smartphones. All these devices are connected to the internet and they continuously send your usage data to the company servers or the cloud. The companies also track your online activities like the websites you visit, the people you talk to, the applications you use, what you buy online, what you want to buy, etc. They monetize this data by providing you personalized services, by selling it, by providing tools to store or sell it, or by using it to become an advertisement delivery network.“

Aashish Pahwa distinguishes 4 types of data driven business models:

This insight is a wonderful transition to my next point …

The impact of platform economics

On April 6, 2017, Brett Scott published at HowWeGetToNext.com a very informative article under the headline: „Reversing the Lies of the Sharing Economy“ (see: https://howwegettonext.com/reversing-the-lies-of-the-sharing-economy-a85501d14be8) including the following citations:

„A platform corporation really only owns two things. It owns algorithms hosted on servers, and it owns network effects – or people’s dependence. While the old corporation had to get financing, invest in physical assets, hire workers to run those assets, and take on risk in the process, a corporation like Uber outsources its risk to independent workers who must self-finance the purchase of their cars, while also absorbing losses from their cars’ depreciation or the failure of their operations. This not only separates corporate managers from ground-level workers, it places the major burden of financing and risk on the workers.

This is a venture capitalist’s wet dream. Give a startup minimal capital to hire developers and run media campaigns, and then watch as the network effects ripple over the infrastructure of the internet. If it works, you’re suddenly in control of a corporation built with digital tools, but extracting value from real-world, physical assets like cars and buildings. The entity holds itself together not via employment contracts, but rather by self-employed workers’ dependence on it to access the market they rely on for their survival.

[…]

So, what is to be done? For one, let’s first understand the problem. Innovation and change are pointless unless they’re coming from a real analysis of what’s gone wrong—especially when we’re being made to believe we’ve actually gained an asset. Only then can we rebalance the power. If we are going to turn ourselves into a sprawling network of micro-entrepreneurs, micro-contracting via a feudalistic platform, let’s at least cooperatively own the platform. In doing this, we might even retain one definition of sharing — the common usage of a shared resource pool, like the farmers who collectively manage a reservoir.“

The German WELT newspaper published on June 2, 2017 a comment by Günter Gressler (Head of 3M Europe) under the headline „Platform Economy – Do German companies just oversleep a trend?“ (See: https://goo.gl/gVdL31). Gressler writes:

„Do German companies oversleep an important trend? Are we just spectators while the U.S. and Asia are marching into the future with their digital platforms? In any case, it would not be surprising looking at a survey performed by the industry association Bitkom. In this representative survey, 6 out of 10 managing directors and executives from Germany stated that they had never even heard of the terms platform economy, platform markets or digital platforms. To put it diplomatically, this finding is questionable.“

„If that stays that way, the digital dominance of the U.S., in particular, will be a locational disadvantage for Europe. Because digitalization is not only revolutionizing people’s everyday lives, but also many classic industrial sectors. So what to do? It certainly can not be about copying success models from the USA and simply transferring them to your own industry. Especially since the founders of the above-mentioned platforms did not set up any platforms because they wanted to set up platforms. First of all, they had an innovative idea. Only then came the platform.“

In a discussion in the German ZEIT newspaper with the boss of the German trade union ver.di, Frank Bsirske, about „Digitalization of the working world“ on August 30, 2017, under the headline „What does Frau Krause do when the algorithm takes over?“ (see: https://goo.gl/AQtp6f) digital consultant Christoph Bornschein pointed out to important side effects of the platform economy:

„Ultimately, trade unions and companies are faced with major design tasks in an environment of failed industrial policy. What does that mean? For a relatively long time, we have not built up our own digital economy in this country, but have become dependent on another economic area with a different set of values – that of the USA. We have a digital trade deficit and massive outflow of funds through platforms like Facebook and Google out of the EU into the U.S.. But besides the funds, the control also drains off. Trade unions and companies are now required to sort out these problems and to accompany and moderate profound changes in the interests of their partners and members – economically effective and socially inclusive.“

Dr. Holger Schmidt (Technical University Darmstadt) explains the economic consequences of the platform economy as follows: „Platforms shift value added not only within a market, but also between states: If we ordered a taxi in Germany in the past, bought a book or booked a hotel room, 100% of the proceeds went into the pockets of the participating (German) companies. Today every time you book your room on Airbnb, every time you buy on the Amazon marketplace and every time you click on a Google ad, you spend money from Germany to the U.S., the land of the platform operator (unless it’s sorted out somewhere in-between to save taxes).

As all global platforms come from the U.S. or Asia, prosperity is shifting increasingly and rapidly from the digital loser countries (Europe, Africa, South America, Australia) to the U.S. and Asia. Because the platforms are spreading in all directions. Amazon is particularly aggressive: The online retailer expands horizontally (for example, attacking the wholesale trade, because it offers in the new section „Amazon Business“ from the stand 100 million products for companies from paperclips to drills), regionally (to Australia and Southeast Asia) and vertically (setting up their own logistics system including their own aircraft, ships, drones and a „Uber for trucks“). When these plans come to fruition, the platforms are gaining ever greater share of value creation, becoming relevant in more and more markets“ (see: https://goo.gl/mFdNX8).

However, it is not just about the economic consequences of digital platforms, but also about social, society related and legal consequences. Think of the latter, for example, about the protection of personal data and the intellectual property of companies (see: https://www.linkedin.com/pulse/how-us-government-discredits-us-american-industry-kurt-brand/). The effective protection of customers‘ personal data and intellectual property (as well as of their end users) would be tangible arguments that European platform providers could, if not necessarily should, score in global competition with U.S. (and Chinese) platform providers.

An eye-opener on the question of why the U.S. is so much more successful than Europe in developing platforms is also the presentation held by the former Chief Technology Officer of IBM Germany, Prof. Dr. Gunter Dueck, under the title „The New – laughed at long, briefly fought, then it is quite normal“ on May 31, 2017 in Zurich at the 4th E-Commerce Connect Conference (see: https://youtu.be/bnPfy0YQgkI). Dueck points out the following important aspects in his presentation:

- As long as the market capitalization of startups continues to grow, revenue and profit are not the key KPIs – which is the reason, why Tesla and Uber, despite low sales and high losses, pose an existential threat to the German auto industry. The high market capitalization also enables market leaders in platform economy to buy potential attackers before they become dangerous, or to penetrate completely new markets by buying established companies. Strictly speaking, Apple, Google or Amazon could pay the stock majority of every German automobile company from the petty cash.

- Digital disruption can consist of mercilessly optimizing basic functions / processes of a value chain (e.g. logistics at Amazon or Amazon Web Services) and then using these optimized functions / processes with their unrivaled low unit costs to adopt / change the rules of the game in other industries (e.g. drastic reduction of logistics costs in the food trade – in the short term by the optimized Amazon logistics and in the medium to long term by trucks with autonomous control, which can transport the food without driver and without congestion extremely cost-effective from A to B).

- If you want to offer something „as a service“, you have to adequately design this „something“, so that it can be easily assembled, put into operation, operated, maintained and suppressed – an IKEA shelf can not be sold as it is “as a service“. And if manufacturers of motor vehicles, machinery, chemical products or electronic / optical products – these four categories of goods accounted for about half of German exports of about € 1.194 trillion in 2015 (see: https://translate.google.com/translate?hl=en&sl=de&tl=en&u=https%3A%2F%2Ftivot.blog%2F2018%2F02%2F10%2Fdaten-und-fakten-zum-deutschen-ausenhandel%2F) – want to succeed as a platform provider in the Internet of Things (IoT), they must redesign their products, e.g. with sensors and software for collecting, storing and analyzing the data.

According to research, by 2020 more than 50 billion „things“ will be connected in the „internet of things“. The customer data sent by these devices to the company servers or the cloud, are analyzed, e.g. to offer personalized services or to sell the customer data to third parties for advertising purposes. The growth of the Internet of Things therefore has significant impact on the future development of the platform economy.

In order to develop a basic understanding of the development, meaning and possibilities of the „Internet of Things“ (in combination with „Big Data Analytics“ and „Artificial Intelligence“), I recommend the following, very readable interview with the „tech guru“ Kevin Ashton the German Frankfurter Allgemeine Zeitung (FAZ) newspaper on October 8, 2017 under the headline „Tech Pioneer Ashton: 2050 we will not be allowed to drive our own car“ (see: https://goo.gl/SZ7n5d).

Quote from it: „The „Internet of Things“ is the evolution of the Internet, in which everyday objects are enabled to send and receive data. This works with the help of sensors, i.e. with microphones, cameras, GPS, with chips like on credit cards or with body tags. The sensors are connected to the internet. Because the data they collect need to be analyzed to know what is happening around us and to make predictions about what’s going to happen. People of my generation still do not really understand what the „Internet of Things“ is about. We grew up with the computers of the 20th century. These computers had keyboards which we used to feed them with all sorts of information manually. The computers helped us to create Excel spreadsheets, which we used to analyze information. Today, the computer processes the data itself. This means, it gets the information, processes it and learns from it. Therein lies the paradigm shift. Such computers are much more powerful than those that depend on people and keyboards. The contribution of sensors and computers is, that we can produce, transport and distribute things much more efficiently.“

The essential abilities of networked „things“ are well illustrated by the following graphics provided by Michael E. Porter:

On the homepage of the German Federal Ministry for Economic Affairs and Energy (BMWi) I came across the following article, which was published by the working group „Digital Business Models / Platform Economy“ under the direction of Dr. Sebastian von Engelhardt and Jasmin Mehrgan (Institute for Innovation and Technology (iit) in VDI / VDE Innovation + Technik GmbH) (see: https://goo.gl/nWfPNq ). Since I find the comments very successful, I will provide you with the following as a quote for the sake of simplicity:

„Today’s customers or service users have ever-higher expectations of receiving products or services as soon as possible. These should also be tailored to their personal wishes. In the meantime, this is a matter of course, especially for younger customers. Companies should therefore think consistently from the perspective of the customer and their needs. For them, that means making the shift from product centric to user centric business models. Car-sharing providers have shown it: Especially young city dwellers are increasingly less interested in owning a car. However, they want flexible access to mobility. In this case, they are preferably vehicles equipped with the latest technology. The modern car-sharing offers fulfill exactly this desire for flexible mobility.

When discussing digital business models, the term „disruption“ is used again and again. This is understood to mean a pioneering, market- or industry-changing development. Disruptive developments – driven by innovative digital technologies and business models based on them – have fundamentally turned entire traditional industries upside down: Amazon revolutionized book and mail order business, the travel industry was undergoing massive changes through portals such as Airbnb, the insurance industry through intermediaries such as Check24 or the taxi industry by Uber. Once established companies were radically displaced from the market (such as Nokia by Apple) or have gone bankrupt (eg Neckermann in mail order for Amazon, Britannica or Bertelsmann encyclopedia by Wikipedia).

Initially small, often underrated players have taken over the field of established companies. Many of the new companies do not even offer their own products, but act on their platform mostly as an intermediary between different providers and the target groups (so-called „Uberization“). In the future, more and more companies will be developing digital business models and data-based business models, replacing traditional products or services, and massively competing with established companies that fail to initiate or miss the transformation process in time.

This also makes it clear that business models in the digitally networked world also have a strong need to „think in terms of systems“. The added value of products and their associated, often data-based, services must be redefined. Often, so-called „hybrid products“ are created here: service packages that consist of a product and services rather than just one product or just one product-specific service.

A basic principle of this so-called digital „platform economy“ is to bring a variety of (different) providers together with their offerings and to offer them to different customers on a common platform. The appeal of the platform for one group (eg app developers) increases as more players in the other group use the platform (eg app users) and vice versa (so-called network effect). The corresponding business models are all the more successful the better it is to create suitable and attractive overall systems („digital ecosystems“) that offer real added value for the customers. An example of this is the group Apple, which operates its own platform and this opens for content providers. Apple was so successful with the launch of the iPhone and iPad because these devices, coupled with their own app store, provide access to a „universe of possibilities.“

The systemic networking of hardware and software products, monetizable data and services – mostly from different competing vendors – and the joint action in a value added network or on a service platform are therefore becoming more and more success-critical for more and more companies. For example, many companies will not be able to open their „platform“ specifically for third-party providers or, if necessary, to cooperate with competitors. A platform and its partners compete with other platforms instead of individual companies.

Knowledge of and mastery of the system logic and „rules of the game“ of digital markets are crucial for successful business in the „Smart Service World“. Smart products, data and Internet-based processes form the basis and offer opportunities for innovative, „smart“ business models. Nevertheless, there is no universally applicable process for introducing digital business models in companies. Companies have to find their own way, adapted to their structures, products and target groups. It is important to answer well-known questions such as „Who generates with whom or by whom, with what and how with which products resp. Services sales? „To find new innovative answers. Customer-centered service platforms play a key role here.“ QUOTE END

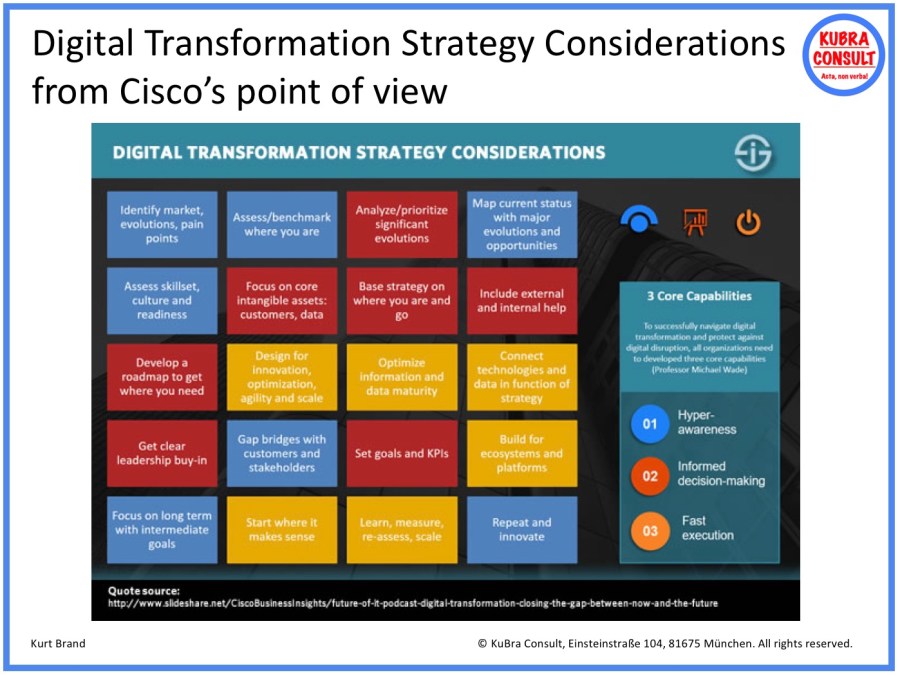

The question of how digital business models can be successfully implemented or how an „analog“ company can best undergo a digital transformation is extremely difficult to answer. There is no such thing as a patent solution. The success depends – as usually in life – above all on the people.

„What does the ideal IT organization look like in a digitalized world?“ This question was asked by the consulting firm A.T. Kearney and the Fraunhofer FIT (Institute for applied Information Technology) in the study „Designing IT Setups in the Digital Age“. Interdisciplinary 140 top managers (mostly C-levels) from all over the world were surveyed, whereby the emphasis was on the German-speaking area (see: https://goo.gl/tzxj8v).

The main conclusion of the study: Today, most companies have a digital agenda, but implementing them is cumbersome. Neither two-speed IT, nor innovation labs, digital hubs, accelerators, or incubators effectively help to reach the destination. Instead, 3 in 4 respondents consider bringing business and IT responsibility together as a key to success. Moreover, the legacy IT, which is usually complex and has grown over decades, turns out to be a heavy block on the leg. A.T. Kearney and Fraunhofer FIT conclude in their market research that 40% of the companies are „digital beginners“ and 27% even „digital objectors“. The vast majority of 87% did not even care to professionally watch aggressive newcomers who wanted to roll up entire markets and did not abide by the rules of the game.

Spin-offs, incubators or so-called „bimodal“ approaches have so far not led to any visible successes. Disposing of the responsibility for the digital transformation to a „Chief Digital Officer“ also not (see: https://goo.gl/txThrC).

Marc Frey has in his really excellent essay „The dilemma of Goliath: Why it is so difficult for Corporates to be as innovative as a Start-up“ (see: https://www.linkedin.com/pulse/das-dilemma-des-goliath-warum-es-corporates-so-schwer-marc-frey/) pinpointed one important issue: „What makes companies so vulnerable and often incapable of innovation, are the same things that made companies once big and profitable: By focusing on ROI and the notorious shareholder value, they have deprived themselves of the opportunity for disruptive innovation.“

Note: The impact of company culture on a company’s ability to innovate and transform its business model should never be underestimated. In my blog published on June 10, 2017, I explain this more in detail and provide some ideas on how you can successfully change a corporate culture (see: https://kubraconsult.blog/2017/06/10/how-to-successfully-change-a-corporate-culture/).

Prof. Dr. Gunter Dueck illustrates with his following quote that innovation (and digital transformation is one of them) is a seedling that can not thrive in a too formal environment:

An important technology, that will play a key role in the development of future platforms is the so-called „Blockchain“, which is used as the technical basis for cryptocurrencies such as the „Bitcoin“. All important facts and milestones about Bitcoin and Blockchains can be found in my blog from August 27, 2017 (see: https://kubraconsult.blog/2017/08/27/the-most-important-facts-and-milestones-of-bitcoin-and-blockchains/).

Finally, I have a suggestion on what the German government could do, to give the topic of digital business models and platform economy in Germany a boost in innovation:

For those who do not know what a blockchain is, here’s a short definition: „A blockchain („Chain of Blocks“) consists of data structures with defined content and a uniform size that are logically concatenated, not on a centralized server but distributed in a network of remote computers, so that they can not be controlled or manipulated by a single person / entity. The anonymity, authenticity and integrity of the data in the Blockchain is ensured by cryptographic methods and procedures (e.g. digital signatures and encryptions). The event log for a transaction (e.g., the payment for a car or the record of information about a person) in the Blockchain is shared with many parties, and information entered once can not be subsequently changed.“

Imagine now that the Federal Republic of Germany would transfer all essential state administrative services into a central Blockchain („Cyber Germany“), so that e.g. Resident’s Registration Office, vehicle registration, child benefit, cadastre or elections („eVoting“) of interested citizens using the (already existing) electronic German ID card can be processed digitally.

In cases where the electronic German ID card is not sufficient, one could alternatively use the (also already existing) PostIdent procedure with video legitimacy (see: https://goo.gl/BSa6vZ ), instead of citing the citizens to the offices and to wait there for hours.

If „Cyber Germany“ proves itself, one could transfer step by step the data from the existing IT systems of federation, countries, cities and municipalities into the Blockchain until the old IT systems can completely be switched off.

Even a separate virtual currency („German Bitcoin“) could be introduced based on the Blockchain in parallel to the Euro (as a lifeline for Day X, when the Euro breaks apart) and could be utilized e.g. to handle tax payments.

Germany would be an innovative pioneer in the digitalization of public administrations.

Last but not least, another important note for companies from the analog world: Digital transformation is like a pregnancy – either completely or not at all! You can not be a little bit pregnant!

15 Kommentare zu „Digital Business Models and Platform Economy“