THIS IS AN AUTOMATIC TRANSLATION CREATED WITH GOOGLE TRANSLATOR OF A BLOG PUBLISHED ON JULY 8, 2018, IN GERMAN LANGUAGE. THE ORIGINAL BLOG CAN BE READ HERE: https://kubraconsult.blog/2018/07/09/die-lebensluegen-des-euro/.

On August 3, 2011, the correspondent of the German Wirtschaftswoche magazine in Brussels, Silke Wettach, and the Wirtschaftswoche’s chief economist, Malte Fischer, published an interesting, for laymen understandably formulated, article under the heading „The life lies of the Euro„. Although this article is already over 7 years old, the identified seven „life lies“ are still valid and virulent. Furthermore, it is interesting and instructive to recall the recent history of the Euro single currency to see how the past observations and analyzes of the two authors have been developed over the past 7 years. For these reasons, I will provide you with the article below, supplemented by some facts and figures that I consider with hindsight as essential or notable (each labeled as „NOTE AT TRANSCRIPTION„).

So, let’s go back to the summer 2011, just over four years after the outbreak of the global financial crisis in 2007/08, caused by the bursting of the subprime real estate bubble in the US. The German chancellor Helmut Kohl was still alive, Angela Merkel had been in office since 2005 and not yet the „eternal chancellor“, Greece was „rescued“ only once and the European Stability Mechanism (ESM), which would substitute the European Financial Stability Facility (EFSF) as part of a „Euro Rescue Package“ from September 27, 2012, onward, was not yet established. That the European Central Bank would pump up its balance sheet total to over €4.5 trillion (as of April 2018) through a €2.3 trillion bond purchasing program, which started in March 2015, was not foreseeable at that point of time.

<START OF QUOTATION FROM THE WIRTSCHAFTSWOCHE ARTICLE FROM 08/2011>

The recent Euro crisis summit on July 21, 2011 has only briefly ensured peace in the financial markets. The structural problems of monetary union are far from being resolved. It is time for politics to commit to the seven major life lies of the Euro.

The collective breathe a sign of relief lasted just seven days. Highly satisfied, after having finally come to an agreement after weeks of turmoil, the 17 heads of state and government of the Eurozone departed from the crisis summit in Brussels last Thursday, July 21, 2011. Markets initially reacted positively to the decisions on Greece and the Euro – because they barely expected that politics would converge.

Just over a week later, European politicians realized that they had not started the „controlled and manageable process“ promised by Chancellor Angela Merkel. In Cyprus, the cabinet of Dimitris Christofias resigned on Thursday, July 28, 2011, after rumors spread that the country was the next candidate for the European bailout fund EFSF (European Financial Stability Facility). On the previous day, the rating agency Moody’s downgraded the credit rating of the island state by two notes and called a further downgrade as possible.

No stable foundation

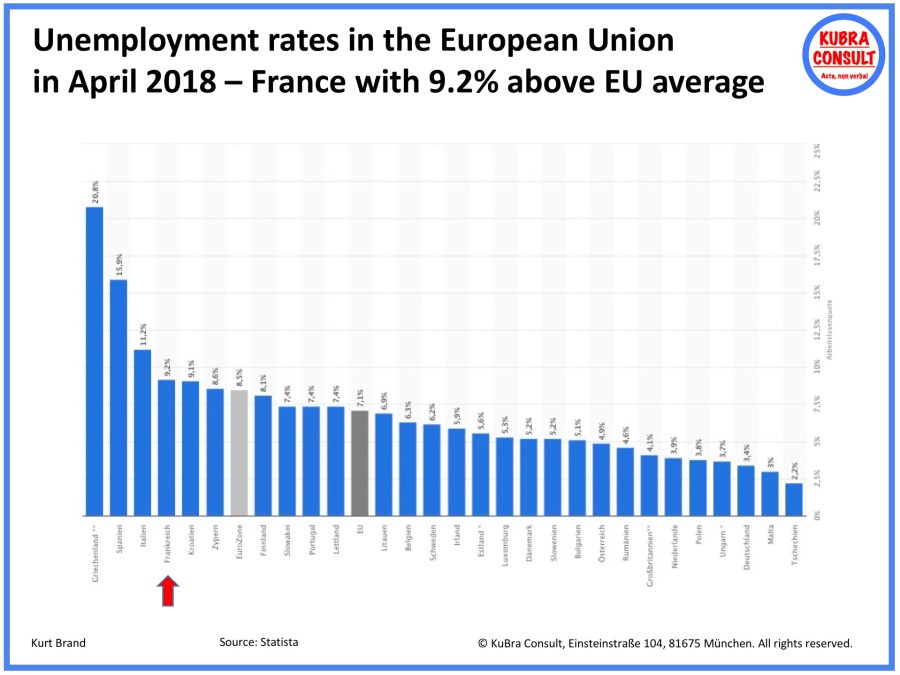

But in addition to the problems of Cyprus came in the past week then also bad news from France. The International Monetary Fund (IMF) called on the government to cut spending and increase revenues, otherwise the budget deficit of 7.1% may not decline to 3.0% by 2013 as planned.

The consequences would be fatal: France threatens to lose the top rating of the rating agencies. Without the French Triple-A, the entire construction of the EFSF rescue package will be shaken. This can only work if the two largest members of the monetary union, Germany and France, have the best credit rating. The latest developments illustrate once again how much politics has illusions – and how much it clings to economic life lies. The Euro does not have a stable foundation because the principles that should make it stable and viable have either been lacking from the start or have been gradually undermined.

Life lie no. 1: Prosperity for all

A common economic area needs a common money. With this postulate politicians in the 1990s promoted a single currency in Europe. Under the umbrella of a common monetary policy, all countries should benefit from stable prices and greater prosperity. But there was another reason: France had demanded as a price for its approval of reunification, Germany had to give up the Deutschmark and hand over monetary policy competence to a common central bank. France wanted to break the hegemony of the Bundesbank.

NOTE AT TRANSCRIPTION:

This narrative was contested by former German Minister of Finance, Theo Waigel, in an interview in the German ZEIT magazine on June 28, 2018. Derived from the question „cui bono?“ („Who benefits from it?“), in my opinion, a major unspoken motivation for the introduction of the Euro was the dream of leading EU politicians that the Euro could challenge the US-Dollar’s position as global reserve currency. Less than ten years after the introduction of the Euro, this dream crushed with the outbreak of the global financial crisis in 2007/08 and the associated weakening of the Euro and banking system in the EU. I think this is the most plausible explanation, since the justification for a „steadily narrowing“ European Union is usually the claim of politicians to assert European interests and values in the world (in addition to the maintenance of peace, which, in my opinion, is primarily a merit of NATO).

<END OF NOTE>

The Deutsche Bundesbank had set the monetary tone in Europe since the collapse of the Bretton Woods fixed-price system. Their stability-oriented monetary policy gave the other central banks only the choice of either following the course or devaluing their own currency. Therefore, the introduction of the Euro from the outset was primarily a political project. The economic facts, however, spoke against it even then. Thus, a single currency makes economic sense only if the members form a so-called „optimal currency area“. Wages and prices must be flexible and the workforce mobile. Goods and capital markets should be strongly networked.

No common economic policy

In addition, the participating countries must have a diversified sector structure and a consistent economic policy. Only then can they cushion economic shocks without resorting to currency depreciation. However, in most Eurozone countries wages are not sufficiently flexible and workers are not very mobile. The economic well-being in countries such as Greece and Ireland depends on a few branches. There is also a lack of common economic policy. While countries in the south see state intervention and inflation as a tried and tested means of solving their problems, northerners are placing more emphasis on competition and stability. Poor conditions for a harmonious life under one roof.

NOTE AT TRANSCRIPTION:

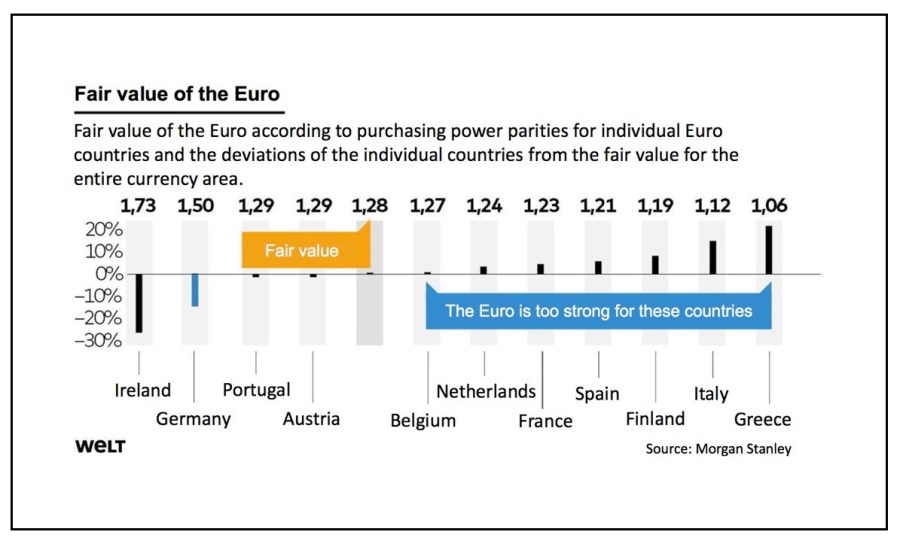

Unfortunately, not only many citizens, but also politicians and experts are blinded by the positive development of the macroeconomic key data in Germany. The external value of the Euro (currently $1.17 per €, instead of a fair value of $1.54 per € for Germany), which is 20 to 30% too low from the German point of view, has led in the past 10 years since the outbreak of the global financial crisis has made it even easier for export-oriented German companies to export even more than at Deutschmark times. As a consequence, the German foreign trade surplus rushed from record to record (which provoked, for example, in the US considerable criticism and even the threat of punitive tariffs). In addition, the zero-interest-rate policy of the European Central Bank enabled the German government to save hundreds of billions of Euros in refinancing its sovereign debt.

The following chart shows the Euro’s „fair value“ for 11 Eurozone countries based on calculations by Morgan Stanley in January 2017, according to an article in the German WELT newspaper published on February 2, 2017, under the heading „Exchange rate: so much is the Euro really worth„:

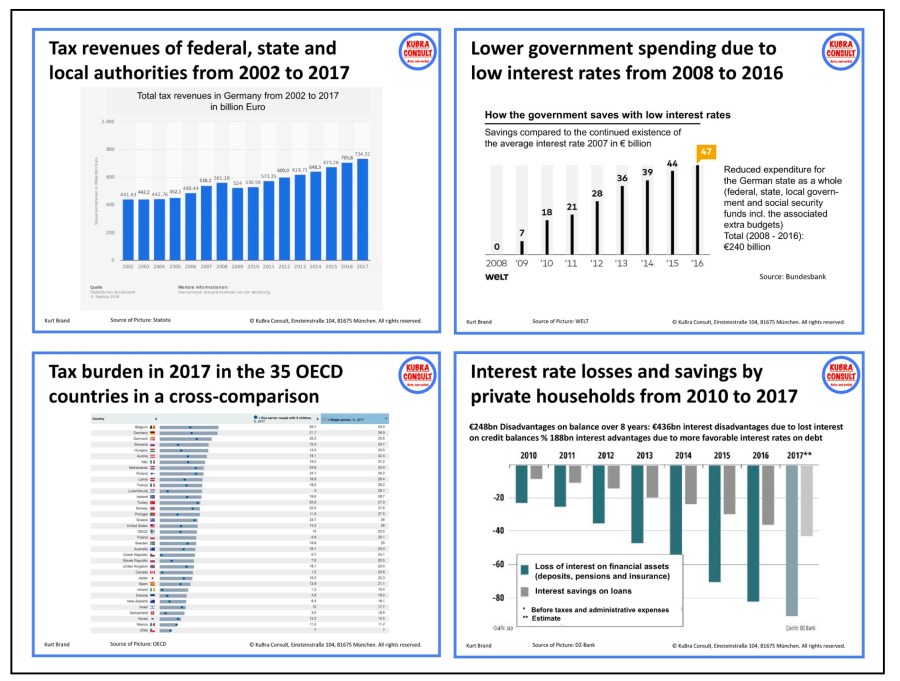

As the next chart illustrates, the annual financial leeway of the German state (federal, state, local and social insurance) was €330 billion higher in 2017 than in 2005, when Angela Merkel became chancellor of the Federal Republic of Germany. The major reasons for this significantly increased financial leeway are higher tax revenues and lower efforts for refinancing government debt. Nevertheless, German workers (singles working full-time) are groaning behind Belgium under the second-highest tax burden among 35 OECD countries.

The reality of life of the great majority of citizens in Germany is not determined by GDP growth, export surpluses, corporate profits or share prices, but by the level and development of wages, social welfare („Hartz IV“) and pensions, the price development of housing rents and consumer goods or the tax burden. Future-proof jobs with adequate salaries, from which a sole earner can feed his family, are the most social form of economic and financial policy. In this regard, too much has been going in the wrong direction in Germany, especially from the perspective of the lower half of the population over the last 25 years, as the chart below illustrates:

The very fact that 19.5 million low-wage earners in Germany (representing 44% of the workforce) will be threatened by old-age poverty on entering retirement age means significant social dynamite for the society and the political system of the Federal Republic of Germany.

Massive investments in education and infrastructure, the establishment of a „sovereign wealth fund“ to supplement the dying statutory pension system with a sustainable component and to involve citizens in productive assets, a radical simplification of the income tax system and the digital transformation of the country would be four concrete measures whose meaningfulness should be obvious. In addition, comprehensive measures to effectively regulate the financial industry should be introduced and implemented in order to curb short-term speculation without benefit to society (high-frequency trading, naked short selling, derivatives trading) and to promote long-term investment for the benefit of society, as referred to in Article 14 (2), of the German constitution („Grundgesetz“), which says „property obligates“.

<END OF NOTE>

Life lie no. 2: More convergence

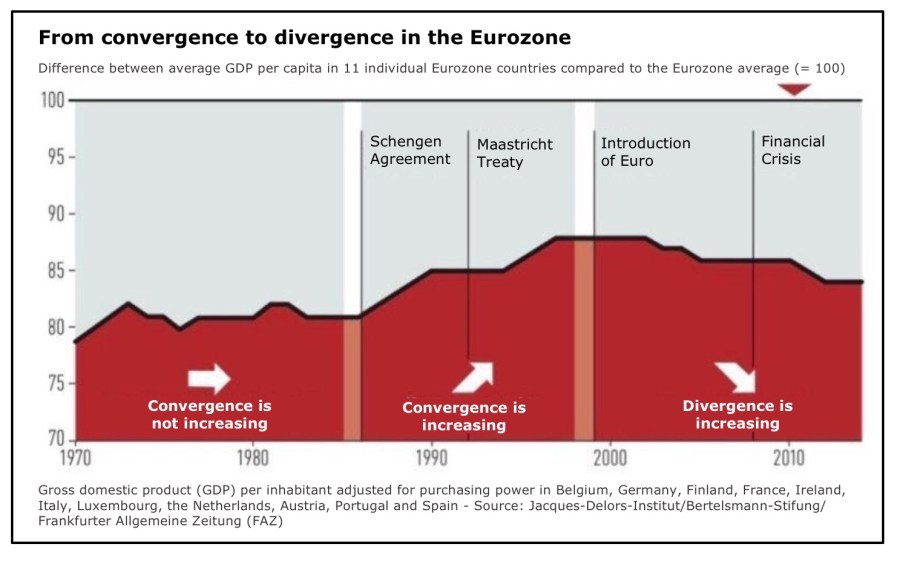

As early as the 1970s, politicians dreamed of the United States of Europe. In order to realize this dream, they pleaded for accelerating economic integration through a common currency. With this so-called foundation stone theory (also locomotive theory), they prevailed against the representatives of coronation theory. The latter warned that a common currency should only be introduced if the participating countries have made a strong economic alignment. In the Euro crisis, the foundation stone theory now turns out to be a historical error. Instead of growing together, the member countries have economically disintegrated. Trade imbalances increase the centrifugal forces.

NOTE AT TRANSCRIPTION:

As the chart below illustrates, convergence between Eurozone member states has worsened gradually since the Euro was introduced in 1999:

<END OF NOTE>

At first everything seemed to go smoothly. In the run-up to the introduction of the Euro, interest rates in the peripheral countries plummeted and approached the low German level. Membership in the Eurozone provided the prospect of price stability and better credit quality. In Spain, short-term interest rates fell from 7.5% in 1996 to 3.0% in 1999. In Ireland, they fell from 5.4% to 3.0% and in Italy from 8.8% to 3.0%. The low cost of funding sparked a credit-financed investment, construction and consumption boom, which drove up the imports of the southerners.

NOTE AT TRANSCRIPTION:

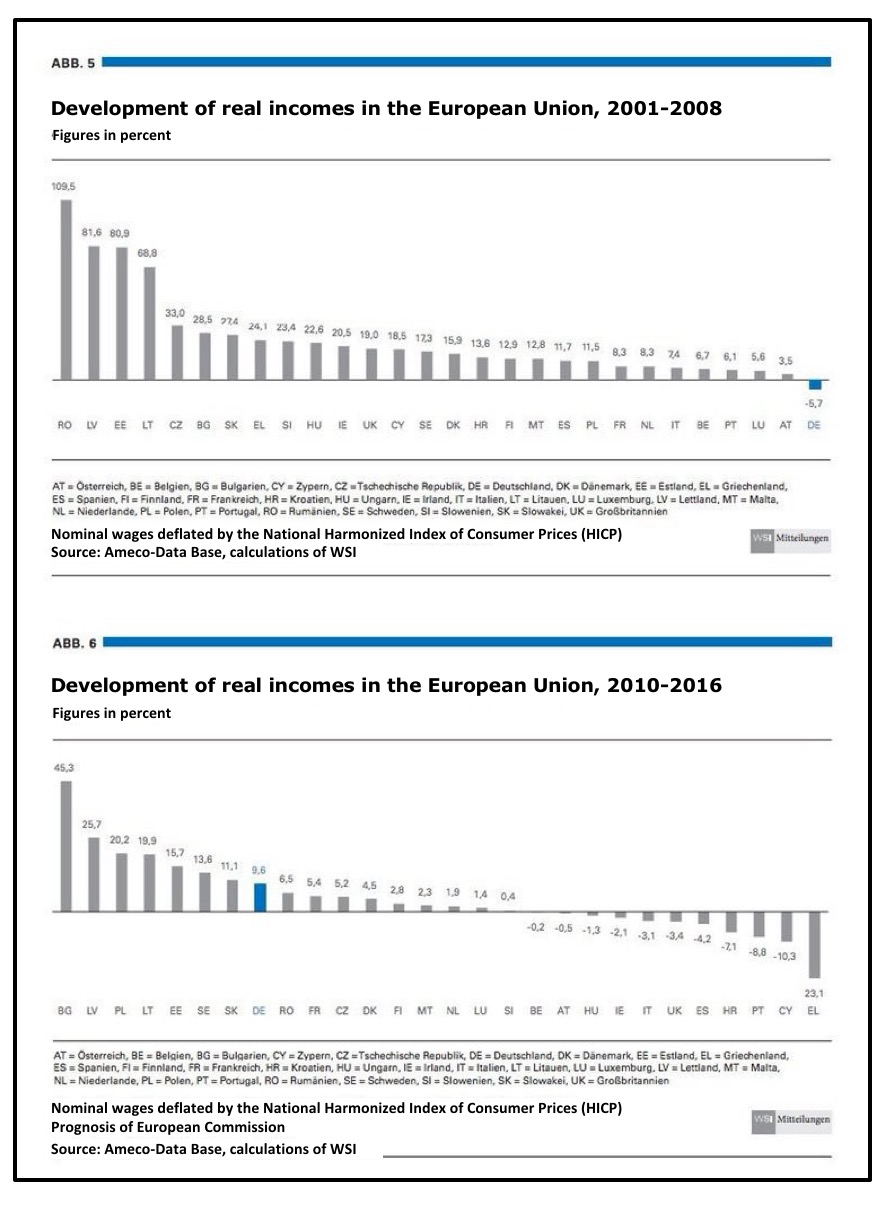

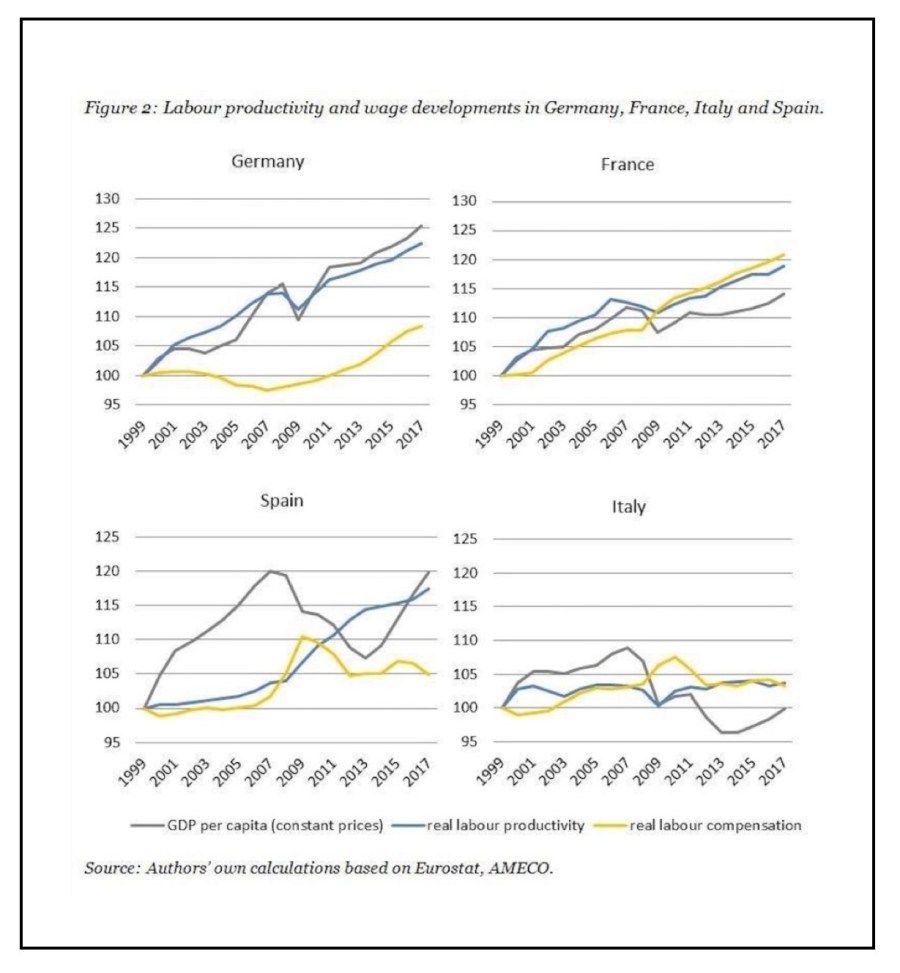

Greece even had double-digit interest and inflation levels before entering the Eurozone. The second major effect (in addition to the significant reduction in interest rates and inflation rates in southern Europe) was the diverse development of real incomes in the 28 EU Member States following the introduction of the Euro between 2001 and 2016. As the chart below illustrates, Germany was the only EU state, where real incomes decreased between 2001 and 2009 (by 5.7%). In all other EU countries, real incomes increased, even reaching double digits in 20 out of 28 EU countries – in Greece, for example, by 24.1%.

The divergence in the development of real incomes has increased the competitiveness of the German economy and reduced the competitiveness of the economies of other EU states relative to Germany – either by a disproportionate increase in real incomes or (as in the case of Italy) by a disproportionate increase in labor productivity (see the following chart provided by the Jacques Delors Institute Berlin):

The penultimate chart with the development of real incomes in the European Union makes clear that in Greece between 2009 and 2016 the above-average increase in real incomes resulting from 2001 to 2009 was reduced. Unfortunately, when discussing the impact of austerity policies in Greece, interested parties tend to forget that real incomes in Greece increased by a respectable 24.1% between 2001 and 2009 (while real incomes in Germany fell by 5.7%).

For a detailed comparison of real income developments in the EU between 2001 and 2016, see: https://tivot.blog/2018/02/10/reallohnentwicklung-in-der-zwischen-2001-und-2016/. Another very interesting comparison between the development of inflation-adjusted corporate profits and real incomes in Germany between 1991 and 2016 is provided here: https://tivot.blog/2018/02/10/unternehmensgewinne-vs-reallohne-in-deutschland-zwischen -1991 and-2016/.

<END OF NOTE>

Debt countries must lower wages

Germany also profited from the credit-financed investment, construction and consumption boom that drove up imports by the southern European countries. The current accounts of the southerners slipped into deficit. In Spain, the negative balance reached around 10% of gross domestic product (GDP) in 2007, and around 15% in Greece in 2008. By contrast, Germany accumulated large surpluses in the current account balance. The crisis is now forcing the southerners to correct. They have to cut wages and prices to become competitive again. But that stifles the economy and makes the consolidation of state budgets even more difficult. By contrast, the German economy is growing strongly. The diverging Eurozone can hardly be controlled by a single key interest rate.

Life lie no. 3: No-Bail-Out

Everyone for himself and God for all of us. That was the principle according to which monetary policy was designed in the monetary union. Article 125 of the Treaty on the Functioning of the European Union (TFEU) therefore states that ‚a Member State is not liable for the liabilities […] of another Member State and does not act for such liabilities‘. But since the financial and debt crisis escalated, the governments are no longer shy about this central requirement. Already with the first rescue package for Greece last year, they violated the no-bail-out clause. Since then, German taxpayers have been liable to Greece for the aid loans provided by the state bank KfW.

Clause finally outmaneuvered

With the recently resolved second rescue package for the Greeks, the clause is finally outmaneuvered. Like the aid to Portugal and Ireland, the money for the Greeks should now be mobilized through the EFSF Euro Rescue Fund. The latter, in turn, acquires the money through its own bonds, for which the countries of the Eurozone are liable in accordance with their share of the capital of the European Central Bank (ECB). Germany is therefore responsible for around 27% of the loans raised by the EFSF. This also applies to bonds that the fund issues in the future in order to refinance purchases of government bonds on the secondary market or preventive credit lines for crisis countries.

Liability and debt community

If the countries in crisis can not repay their loans or credits, taxpayers from other countries have to step in and provide the EFSF with the means to service its bonds. Particularly fatal is that the EFSF should pass on its low refinancing costs to borrowers in the form of low interest rates. This further reduces the incentives for debtor countries to refurbish their national budgets. The hoped-for stability union has thus become a liability and debt community.

NOTE AT TRANSCRIPTION:

The bailouts for member states in the Eurozone add up to more than 600 billion Euros. The programs for Ireland, Portugal, Spain and Cyprus have been completed. More money flowed to Greece than to all other crisis countries combined. The entire scope of the previous „Euro Rescue Packages“ from „Greece I“ in spring 2010 to „Greece III“, which is due to expire in 2018, has been documented by the news broadcast of the first Federal German television channel (ARD Tagesschau) here: https://www.tagesschau.de/wirtschaft/rettungspakete108 .html.

In the already above-mentioned interview in the German ZEIT magazine on June 28, 2018, the Director of the European Stability Mechanism (ESM), Klaus Regling, and the former Chief Economist of the European Central Bank, Jürgen Stark, commented as follows:

Klaus Regling: „We are providing financial help, but in the form of loans to be repaid, which are also bound to strict reform requirements. These are not transfers, and that will remain the case. The fund closes a gap that we may have missed in the past: in a severe crisis, countries may lose investor confidence, with the result that no one buys their government bonds anymore. When we started the monetary union, we had not thought it would be possible that something like that could happen in Europe. Today a country can ask us for a loan in such a situation, if otherwise the stability of the monetary union as a whole would be endangered.“

Jürgen Stark: „But that is a completely different monetary union than the one was designed in the Maastricht Treaty. Its character was changed by the crisis measures. The important principles such as no bailout clause and self-responsibility of the member states or the prohibition of state financing by the European Central Bank have been completely undermined. I am not on the side of those who are constantly going to the Constitutional Court. But that does not change the facts.“

The following picture translated from a German caricature provided by Horst Haitzinger brings this to the point.

In an interview on June 30, 2018, at Tichy’s Insight under the heading „The ‚Lirazation‘ of the Euro“ (see: https://www.tichyseinblick.de/wirtschaft/die-liraisierung-des-euro/) the former chief economist of the Deutsche Bank, Thomas Mayer, draw the following conclusion while discussing with former budget expert of the German Alliance90/The Greens political party, Oswald Metzger:

„Yes, the pillars of the EMU were tacitly dismantled. If I say tacitly, I mean that the responsible politicians have transformed them in a non-transparent way into a community of liability that is in sharp contradiction to the original intention and sacred oaths at the beginning. In our appeal of 154 German economists („The Euro may not lead to the liability union!„) published on May 21, 2018, I see a dividing line. There are some, even from the guild of economists who think our appeal is destructive. They say, it contains no constructive elements, which is why it should be rejected. Anyone who argues like this, opposes the idea that a country that is not functioning in EMU will ever leave it again.

The critics complain that one should not permanently recall the initial „no-bail-out“ clause, which codified the liability for respective own fiscal decisions. No, on the contrary, one have to have an obligation to stabilize the current monetary union. These people accept what has been decided in politics that the EMU is a one-way street. They inevitably have to defend themselves against criticizing the communitarisation of liability, since a return to the still valid treaties does not allow every country to remain in the monetary union.“

In plain words: The wrong decision to introduce the Euro is defended with teeth and claws – whatever taxpayer’s money it takes …

One should also mention that the „rescuing“ of Greece had to be paid by member states of the Eurozone, whose citizens are significantly less wealthy than the Greeks – you may think of e.g. the Baltic States (Estonia, Latvia and Lithuania) or Slovakia. In a speech in the Slovak parliament in 2012, former Slovakian parliamentary president Richard Sulik disgustedly described the conditions under which the decisions on the European Stability Mechanism (ESM) were pushed through the parliaments and the pressure that particularly small states such as Slovakia were exposed to: https://youtu.be/y8KSBykRJl8 (Note: The speech is in Slovak language with German subtitles can be switched on).

<END OF NOTE>

Life lie no. 4: Statistics do not lie

Today everyone is smarter. Greece would never have been in the Euro, say with hindsight former German Chancellor Helmut Kohl as well as current German Chancellor Angela Merkel. Seven times in a row, from 1997 to 2003, the Greeks reported false deficit numbers to Brussels. In 1998 and 1999, which were considered to be the reference value for joining the Euro, the deficit was in fact well above the maximum permitted 3.0% of gross domestic product (GDP). When the Greek fraud finally surfaced in 2004, the excitement was high in Brussels and the states. Sanctions were mentioned, such as the blocking of subsidies. But nothing ever happened, for lack of legal means. The founding fathers of the Euro had not reckoned with such brazen cheating, although others – and even the Germans – sought refuge in creative accounting in order to overcome the hurdle.

Greek bargains

Meanwhile, it is also clear that the Greek hanky-panky in the EU capitals had been known for much longer. The officials of the European Commission noticed regularly that the numbers did not match. At the meetings of the European Ministers of Finance the topic came up again and again. „Nobody wanted to deal with it properly,“ recalls one who was there. „The theme was dismissed after the motto, the Greeks are just rascals.“ Secretly, everyone hoped that such a small country has no impact on the entire currency zone. A misjudgment, as has been shown. Added to this was political pressure from the top.

The monetary union, so the political requirement, should include as many states. Helmut Kohl made it clear that he did not think much of a debate on the Euro-fitness of states such as Belgium and Italy, whose government deficits already exceeded the 100% mark, even though only 60% were (and are) admissible. „It is the German interest that as many countries as possible meet the criteria,“ Kohl emphasized in the autumn of 1995. That the Euro banknotes were designed from the beginning with the Greek name Evro, although Greece was not even a member of the Eurozone, speaks for itself.

NOTE AT TRANSCRIPTION:

The member of the German Parliament and christian-democratic politician, Klaus-Peter Willsch, has set out on June 30, 2018, in Tichy’s Insight under the heading „Green Fake News: The Greece loans are gone forever“ how the voters and taxpayers with regard to the „rescue“ of the Euro over years were lied to and cheated, for example, interest rates and repayment deadlines have been repeatedly extended to protect Greece from bankruptcy (resulting in losses for the taxpayers of the creditor states) or by the participation of the International Monetary Fund (IMF), which in 2015 was required for the approval of the German Parliament for the third „rescue package“ for Greece, but was not implemented in the end.

<END OF NOTE>

Life lie no. 5: Stability Union

For the German Minister of Finance, Theo Waigel, the point was clear: „The Euro will only be a successful and respected currency, if it is a stable currency“, he said, when the budding members of the Eurozone in 1996 decided under German pressure on the stability pact. A ceiling of 3% of the gross domestic product (GDP) for the budget deficit and a 60% government debt cap for the government debt should discipline potential debt transgressors. But the sanctions provided by the Stability Pact have not been applied once. Even more: the policy softened them later.

Excessive deficit procedures came to nothing

When Germany and France violated the deficit rule for several years, Federal German Chancellor Gerhard Schröder (SPD) and French President Jacques Chirac abruptly weakened the Stability Pact, which gave Euro countries room to maneuver. Excessive deficit procedures against the two states came to nothing.

Current attempts to tighten the Stability Pact are lacking credibility after this precedence case. Even worse, the sanctions of the market will no longer apply if the EFSF rescue fund buys bonds from crisis countries in the future. „Every state in Europe can borrow at will, without being punished by higher interest rates,“ warns Ifo CEO Hans-Werner Sinn.

NOTE AT TRANSCRIPTION:

The starting point for the introduction of the Euro was the post-war monetary system (with the abolition of the US-Dollar in 1971, the dissolution of the Bretton Woods monetary system in 1973 and the European Monetary System (EMS) between 1979 and 1998). I do not want to go into detail here, otherwise the article would be too long.

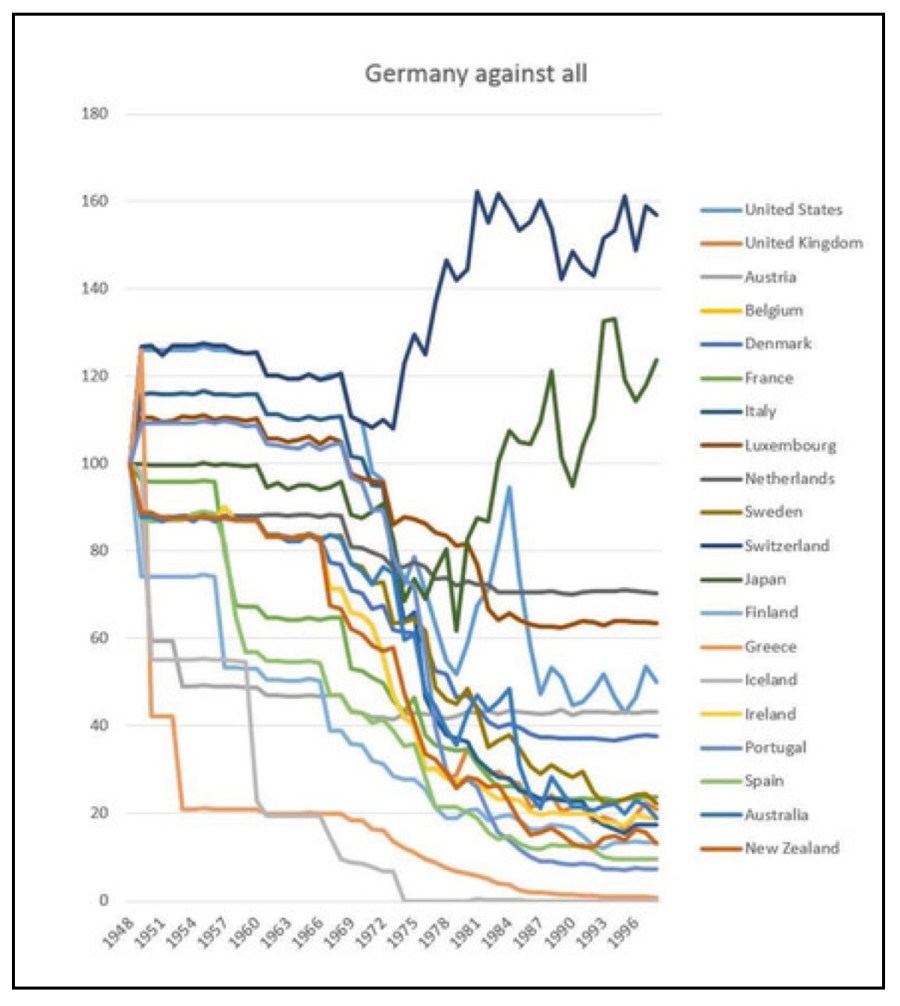

As the chart below illustrates, in the 50 years between 1948 and 1998 – with two exceptions (Swiss francs and Japanese yen) – the Deutschmark has significantly revalued against all well-known currencies, in some cases by several hundred percent (for example, between 1970 and 1998 the value of the Italian Lira decreased by 600% against the Deutschmark). Even against the world currency US-Dollar, the Deutschmark revalued by 60% between 1960 and 1998. The Deutschmark stood for solidity, stability, reliability and prosperity and, unlike the Euro, it did not have to be „rescued“ only once in its 50 years of existence.

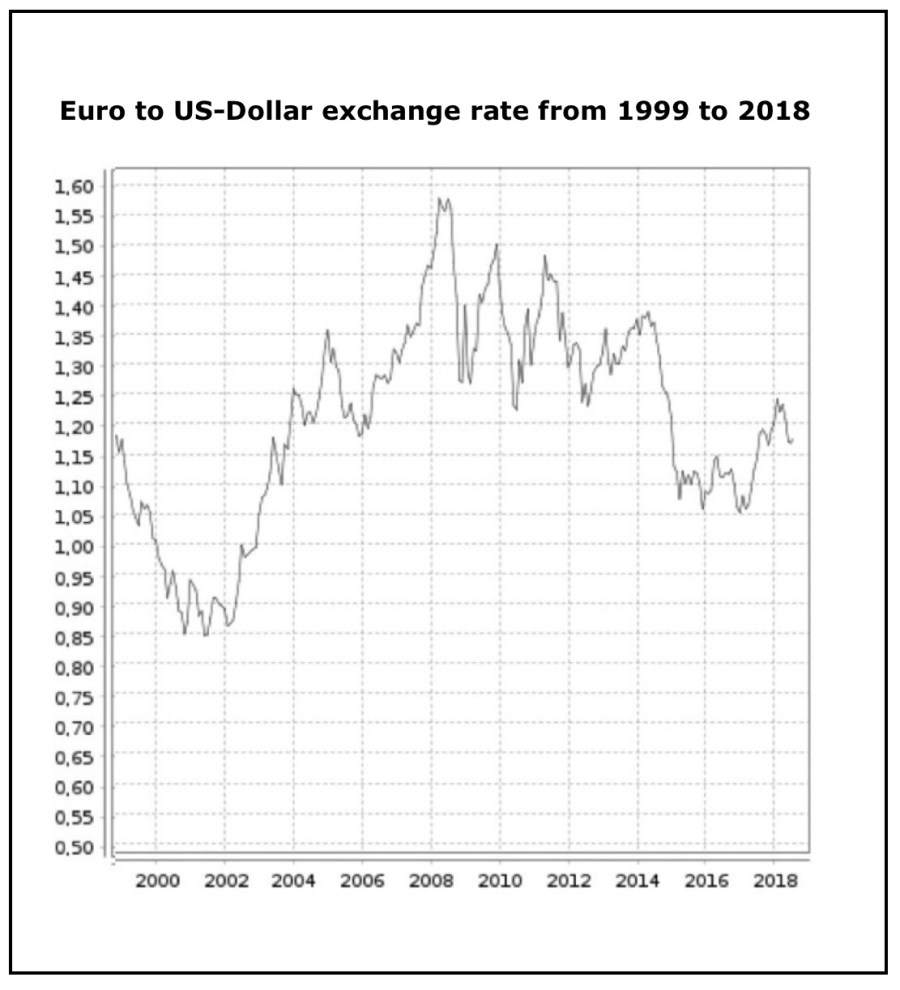

By contrast, the exchange rate of the Euro against the US-Dollar between 1998 and 2018 shows significant volatility (range between $0.85 per Euro and $1.60 per Euro) and no sustained revaluation over the 18 years of its existence.

The following chart illustrates the exchange rate between Euro and US-Dollar from 1999 to 2018:

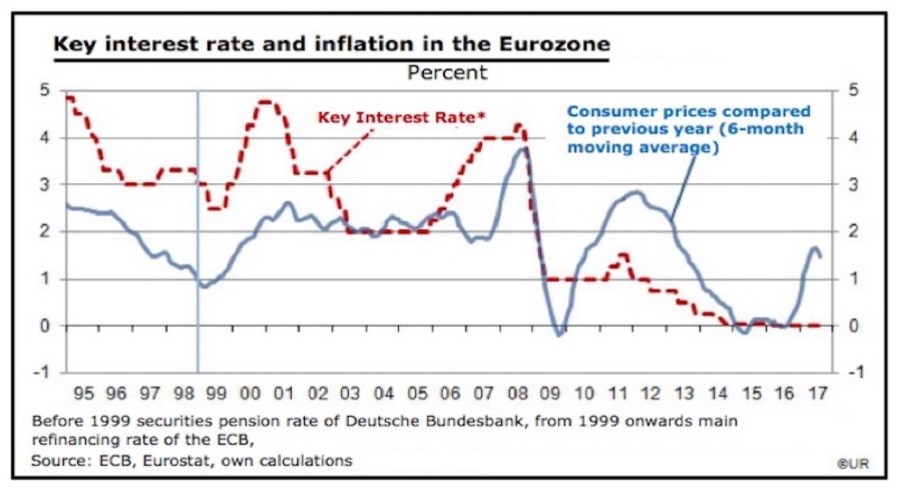

The key interest rate and inflation rate are also subject to significant fluctuations in the Eurozone. As the chart below illustrates, the ECB initially lowered its key interest rate (red line) from around 4% to 1% after the outbreak of the global financial crisis in 2008, and then reduced it through several small steps to 0% (from March 16, 2016, onwards).

Low Euro exchange rates and low interest rates are good for export-oriented companies and debtors (most notably over-indebted countries, which have saved hundreds of billions of Euros in refinancing their sovereign debt over the past 10 years), but bad for consumers, savers, tenants and taxpayers:

- Consumers have to pay 20 to 30% for overpriced imported products from non-Euro states (including fuels, clothing, smartphones, consumer electronics, „white goods“, etc.) as well as for holiday travel to non-Euro states.

- Savings deposits and investments for pensions are covertly devalued by low/zero interest rates – which affects in particular the German savers, as they invest their money mainly in supposedly safe investment forms (savings account, fixed income securities, life insurance) and compared to other EU countries only to a limited extent in shares or real estate.

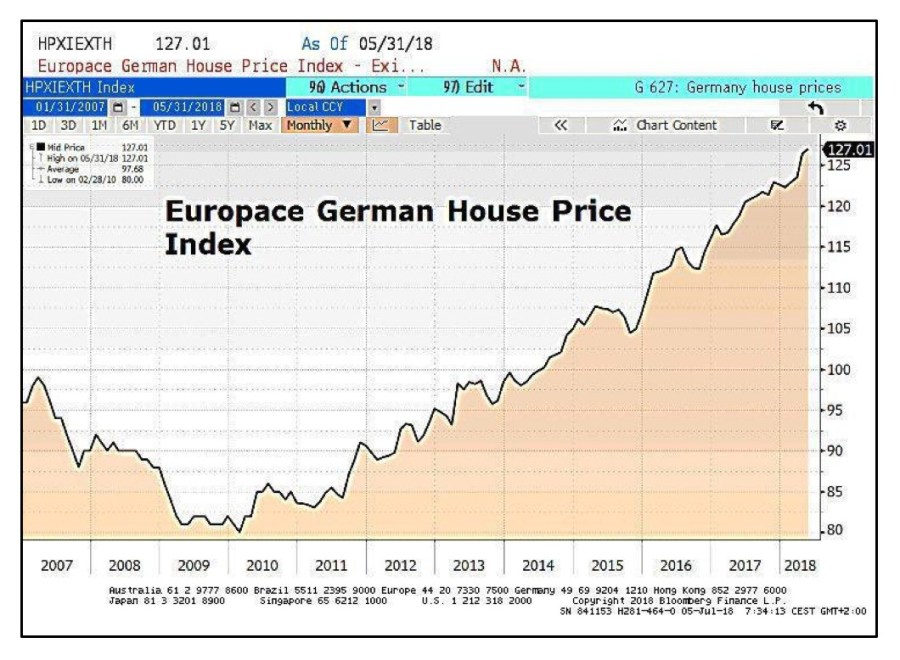

- The cheap money of the central bank generates bubbles on the stock and real estate prices. In all major German cities, real estate prices have risen by well over 50% since 2008.

- The misconstrued Eurosystem has resulted in German taxpayers being burdened with default risk of approximately €2 trillion over the past 10 years.

The following chart illustrates the increase of the German House Price Index between 2009 and 2018:

The default risk of €2 trillion for German taxpayers is structured as follows:

- €1.152 billion from the 25.6% share of the Deutsche Bundesbank in the total assets of the European Central Bank amounting to €4.5 trillion per April 30, 2018

- €976 billion TARGET2 claims of the Deutsche Bundesbank to the ECB as of June 30, 2018 (of which only one quarter is visible in the ECB’s balance sheet, since TARGET2 claims and liabilities of the Eurozone countries are netted at ECB level)

- €190 billion maximum liability share of the Deutsche Bundesbank in the loans issued by the European Stability Mechanism (ESM)

<EXCURSION TO THE „TARGET2“ TOPIC>

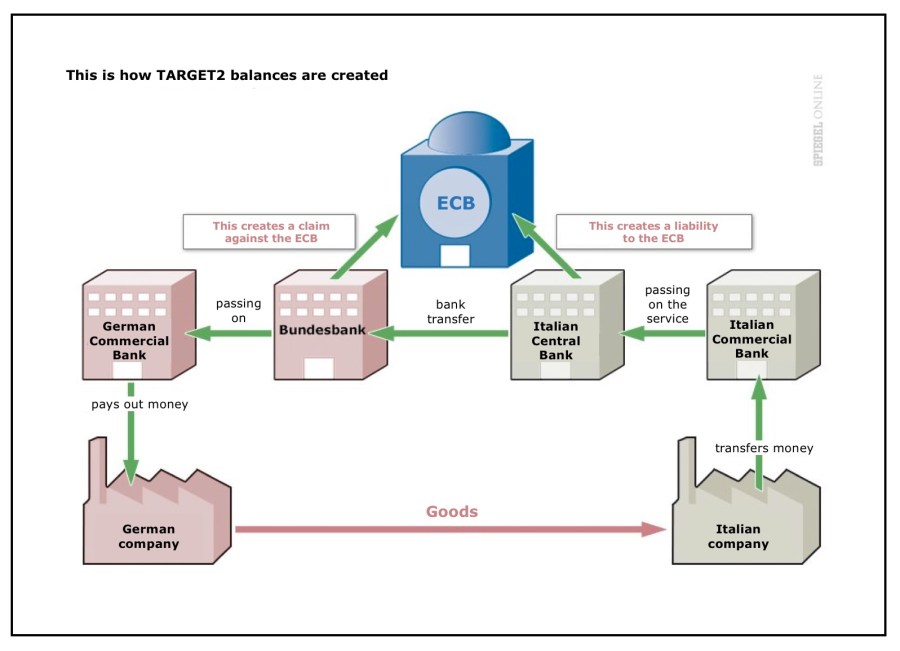

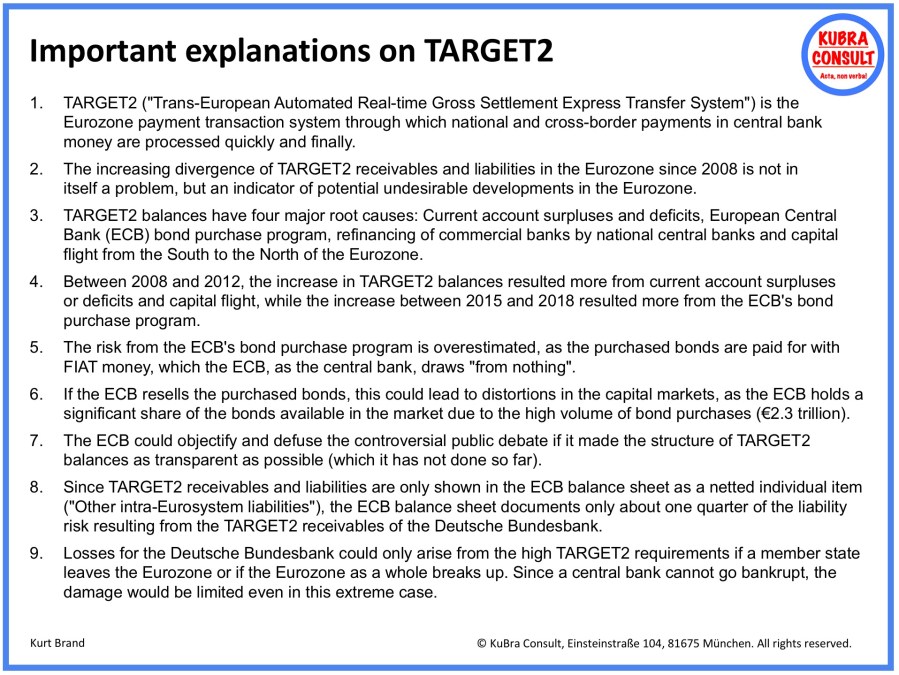

TARGET2 is the payment system of the Eurozone, which transacts national and cross-border payments in central bank money quickly and definitively. According to the German Bundesbank, TARGET2 generates an average of around 340,000 payments worth around €1.7 trillion per day. For a full year, TARGET2 will process nearly 90 million payments for a total value of approximately €450 billion.

A quite comprehensible explanation of the TARGET2 system can be found in an article published by the German SPIEGEL magazine on July 10, 2018, under the heading „Bundesbank claims: is Germany really sitting on a trillion-dollar-bomb?„. From this SPIEGEL article, I have taken the following chart, which illustrates how TARGET2 balances arise from trade in goods (which is just one of several possible causes for the creation of TARGET2 balances, I will come back to this in a minute):

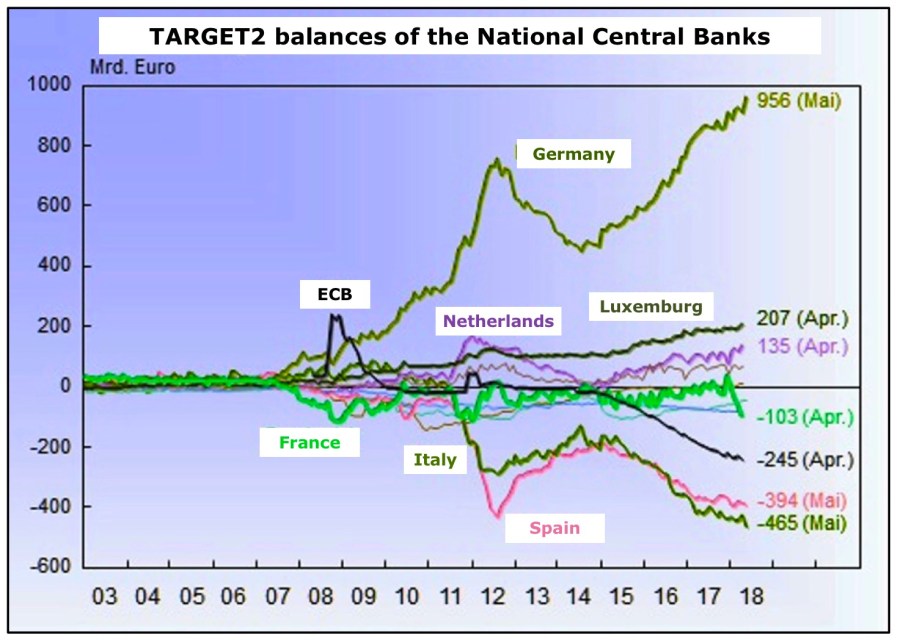

Before the global financial crisis started in 2007/08, the TARGET2 balances of the national central banks were largely balanced. As the German Wirtschaftswoche magazine reported in an article published on March 5, 2012, under the heading „Euro crisis: TARGET balances pushing Germany to the abyss„, the former president of the German Bundesbank, Helmut Schlesinger, discovered at the end of 2010, that the Deutsche Bundesbank in its Balance sheet had accumulated 300 billion Euros under the title „Claims within the Euro system (net)“ – which was almost 20 times of what was recorded before the financial and Euro crisis started.

When Schlesinger asked his former counterparts at the Bundesbank what the reason for this extraordinary development was, he did not get a satisfactory answer, he told the Wirtschaftswoche on the sidelines of an interview. He then turned to Hans-Werner Sinn, the CEO of the Munich Ifo Institute, who at first could not make any real sense of the receivables balance in the Bundesbank balance sheet. Sinn conducted research – at the Bundesbank, the European Central Bank (ECB) and in the literature – and sparked a heated debate in economists circles, which reached the general public in 2012 and still continues today.

In parallel to the controversial debates in professional circles, the TARGET2 balances reached new record highs (see chart):

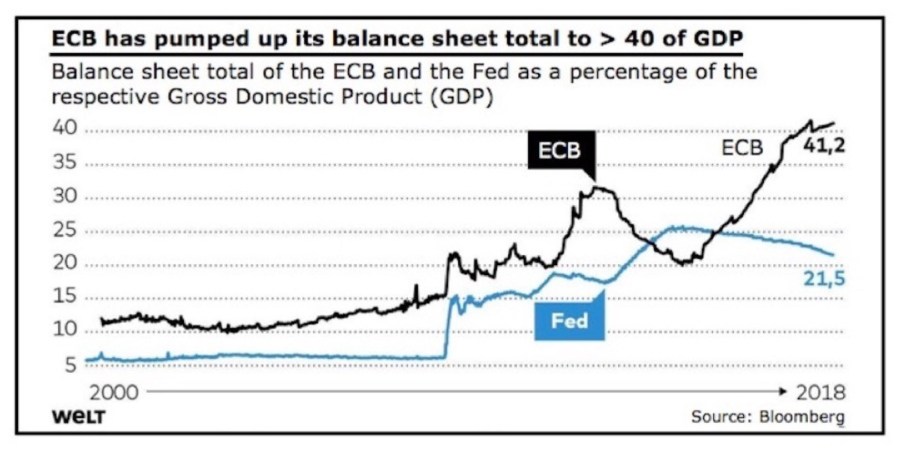

As a consequence the European Central Bank pumped up its balance sheet volume to over 40% of the Eurozone’s Gross Domestic Product (GDP):

The Federal Association of German Banks names in a publication from the series „Economic Policy Update“ published on February 15, 2018 four major root causes for the divergence of TARGET2 balances since 2008:

- Current account surpluses or deficits of EU member states

- Refinancing problems of banks (e.g. in Italy), which can only refinance themselves through their national central banks

- Capital flight from the south to the north of the Eurozone

- The European Central Bank’s bond-purchasing program („Quantitative Easing“)

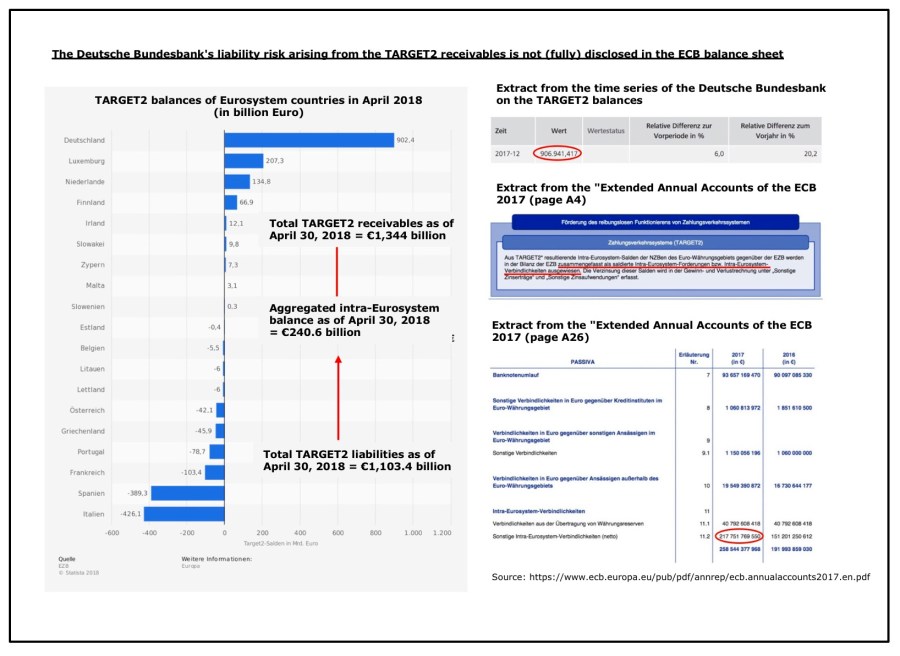

The European Central Bank and the Deutsche Bundesbank are not entirely innocent of the heated discussion which spilled over from the expert circles into the public during 2012, because, firstly, there is a lack of transparency as to which of the aforementioned root causes contribute to what extent to the spreading of the TARGET2 balances. Secondly, there is still some controversy over whether the ECB has not exceeded its mandate with the bond-purchasing program and is in the process of prohibited public funding (the respective lawsuits are still pending at the European Court of Justice). Thirdly, the European Central Bank also uses an intransparent accounting logic.

This intransparent accounting logic, in which the TARGET2 claims and TARGET2 liabilities of the EU member states‘ central banks are netted and reported as a single liability on the liability side of the ECB’s balance sheet, is illustrated in the chart below (Note: On the left side of the chart you’ll find the TARGET2 balances as of April 30, 2018, the data on the right side of the chart is as of December 31, 2017, on which the ECB’s balance sheet was prepared). Gerald Braunberger, who is responsible for the financial market at the German Frankfurter Allgemeine Zeitung (FAZ) newspaper, assumes that the reported balance results from liabilities caused by the ECB’s own operations, since the ECB is not only the clearinghouse for the national central banks‘ TARGET balances, but owns as well positions from own transactions. This sounds logical, but it is not explicitly explained in the ECB’s Annual Accounting Directive.

Between economists and financial experts is controversial, how concrete and extensive the threat from the aforementioned liability risks in the amount of €2 trillion is and whether and under what conditions the aforementioned amounts would materialize as losses for the German Bundesbank and thus for the taxpayer. Consensus seems to be that the TARGET2 demands will only lead to losses if states leave the Eurozone or if the Eurozone as a whole breaks down.

Even if one sees the growing spread of TARGET2 balances not as a problem on its own, these spreads are at least an indicator of potential problems such as trade imbalances, capital flight or refinancing problems for banks that no longer have access to the capital market. Incomprehensibly, the ECB does not publish statistics on the structure of TARGET2 balances. It would at least make the discussion more objective and reassuring, if the public knew what shares of the TARGET2 balances resulted from bond purchases, from the refinancing of commercial banks by national central banks, or from current account surpluses or deficits.

In an Wirtschaftswoche article published on July 20, 2017, the Norwegian economist Kjell Nyborg, explains under the heading „The ECB risks monster inflation„, that the ECB, as part of its bond-purchasing program („Quantitative Easing“), accepts junk bonds or bonds for which no market (and so that no market prices exist) as collateral for its bond purchases. According to some experts, the sale of ECB-purchased bonds following the end of the Quantitative Easing program could cause economic disruptions in the markets.

The renowned economist Martin Hellwig argues that money creation through open-market purchases by central banks initially creates an undeclared profit and the losses can not exceed this profit: „Every counterfeiter knows that he can enrich himself when by printing paper slips and putting it as Money into circulation, for example, by buying a second-hand vehicle. If the vehicle breaks down afterwards, the counterfeiter suffers a damage, but after that he is not poorer than before the purchase of the vehicle. The employees of the Bundesbank, who have stolen and recirculated old bank notes thirty years ago, knew that too. The same connection applies to the central bank, except that it does not have to fear the public prosecutor, because it has a state monopoly on the sale of such bank notes. When the central bank uses this monopoly to buy securities, it becomes richer. If it later suffers a loss on these securities, the central bank becomes poorer again, but not poorer than before the purchase. “

<EXCURSION END>

Apart from these specialist discussions, the events in Greece in 2015 and in Italy in 2018 show that the Euro is a fragile entity and by no means irreversible. Greek Minister of Finance Yannis Varoufakis had already worked out in 2015 plans to return to a national currency for Greece. The Euro-critical government of Italy, elected in March 2018, is considering the introduction of so called „mini-bonds“, which would de facto be a parallel currency to the Euro. Cryptocurrencies such as Bitcoin may also become a vanishing point for investors who have lost confidence in the Euro and the European Central Bank at the latest in the next financial crisis (see „Crypto Assets – the most important Q&A„).

The speech bubble in the following caricature on the left says „Allow me, I’m the statistical likelihood“ and on the right „Pleased to meet you. I’m the residual risk.“

The failure of the Euro is therefore not impossible and due to its €2 trillion default risk, Germany is politically extensively in danger to be blackmailed. On the other hand, especially in the south of the Eurozone, the EU countries are at the mercy of the ECB and its monetary policy because of their comparably high debt burden. This dependency, by the way, is far too rarely taken into account in discussions about the Euro.

Analysts of the Flossbach von Storch Research Institute have calculated what would happen if interest rates in 2025 were back to 2008 levels. So at a level of about 5%, as before the financial crisis. In Italy, the average interest rate for outstanding government debt is 3%, which varies widely depending on the maturity of the bond. From then on Italy would have to finance itself at an average interest rate of 5%, so that by 2025 the interest burden could amount to more than €100 billion. That would be an increase of about 50% compared to today’s debt burden. A horror scenario, the debt crisis in the Eurozone would be back. But even for a comparably low-debted country like Germany, significantly higher interest payments could quickly become a problem. An increase in interest rates on federal debt to 4% would mean overspending up to about €20 billion a year for the German budget. This is about the amount of money earmarked for the combined annual budgets of the German Foreign Ministry, the German Ministry of Agriculture and the German Ministry of Agriculture.

There is therefore potential for blackmailing by the ECB, which the ECB could used in cooperation with the EU Commission to discipline overly critical governments with anti-Euro views. Sometimes a wink with the fence post is enough. And in this context as well, the question is worthwhile: „cui bono?“ – „who benefits from it?“. Everything in the Eurosystem is connected with everything. In fact, there are 19 national helmsmen who can influence the well-being and woe of the Eurosystem through their national financial and economic policies, plus the EU Commission and the ECB. All of these stakeholders do not necessarily have the same interests, and in doubt, one’s own wallet is closer than the neighbor’s.

<END OF NOTE>

Life lie no. 6: Promote and Demand

Ever since the Euro member states decided on the „rescue package“ for Greece, Angela Merkel has been constantly reiterating that European solidarity has its price. „The awarding of loans is subject to strict conditions,“ promised the German Chancellor to the German citizens, as in May 2010, the transitional rescue fund EFSF was created. Original sound, Merkel: „We help under the condition that the affected state commits itself to comprehensive own efforts.“ Also in her policy statement on the future permanent rescue fund ESM she stressed in December 2010, the „strict conditions“.

And in March this year, Merkel announced that she would vote unanimously on the ESM decisions to be taken in the future: „Germany can veto if the conditions for aid are not met – and I will make use of that.“ The reality is different. Greece has not met the requirements of the first rescue package, as the European Commission, the ECB and the IMF have stated. Government spending rose 8.8 percent in the first half of 2011 rather than falling. Nevertheless, the country now even gets a second „rescue package“, because the protection of Greece is „a self-defense mechanism for the Eurozone,“ as the Greek Minister of Finance Evangelos Venizelos finds.

Also Ireland and Portugal miss the conditions

Following the motto: The Eurozone has no choice anyway. It does not look much better in Portugal and Ireland. Both countries receive aid from the EFSF – and both missed the agreed requirement in the first half of the year. As a reward, they received lower interest rates on their loans at the recent EU summit. And what about the allegedly stringent requirements for the European Rescue Fund, when it buys government bonds of troubled countries from private investors? The German Minister of Finance Wolfgang Schäuble emphasizes that this is not a carte blanche. No, here too European politics has once again built in conditions. However, they should be worth little only in an emergency case.

NOTE AT TRANSCRIPTION:

In fact, the policy of „promoting and demanding“ – better known today as the „austerity policy“ – has thrown back understanding amongst nations and cohesion in the European Union by 40 years. In the course of the re-boiling Greek crisis in 2015, the emotions escalated between Germans and Greeks and long-overcome alleged hatred and mutual prejudice broke their course – including posters with Angela Merkel and Wolfgang Schäuble with Hitler mustache and in SS uniforms.

The Euro crisis has left a lot of scorched earth in the EU. I do not consider it unlikely that the endless Euro crisis in combination with the refugee crisis from 2015 also had a decisive impact on the British BREXIT decision in June 2016. The collateral damage caused by the Euro, directly and indirectly, is therefore considerable.

<END OF NOTE>

Life lie no. 7: Germany as main beneficiary

It sounds logical: the Euro eliminates exchange rate risks between trading partner countries in Europe, thus stimulating exports and stimulating the economy. In fact, since the introduction of the Euro in 1999, German exports to the Eurozone have risen on average by 5.2% per year. However, exports to countries outside the Eurozone grew at a much faster rate of just under 7% thanks to the boom in emerging markets – although they are subject to exchange rate risks. As a result, the share of the Eurozone in German exports fell from 46.4 to 41.3%. The growth of the German economy has also not increased as a result of the Euro. Data and facts about German foreign trade can be found in my eponymous blog from September 9, 2017 .

From 2000 to 2010, real gross domestic product in Germany increased by an annual average of 1.1%. At Deutschmark times, from 1990 to 1999, the rate of growth was more than twice as high at 2.3% ( NOTE AT TRANSCRIPTION: The high growth rates in post-war Germany of the 1950s and 1960s would have to be fairly excluded in this comparison <END OF NOTE> ). One reason for the comparably low gdp growth was, that from 2002 to 2005, Germany submitted to a drastic treatment in order to regain its price competitiveness, which it had lost in the slipstream of reunification.

Dampened domestic demand

The pronounced wage restraint and hard cost reduction rounds in the German companies dampened domestic demand in Germany. On top of that, however, after the introduction of the Euro, two-thirds of domestic savings flowed out into the booming southern Eurozone countries. In the view of many economists, this slowed down investment in Germany.

NOTE AT TRANSCRIPTION:

The economist Daniel Stelter has published a very readable article in the German Manager Magazine on March 4, 2015, under the heading „Germany and the Euro crisis: ten reasons why we are the losers of the Euro„. In this article, Stelter mentions the following essential reasons, why Germany is the loser of the Euro:

- The too low Euro rate is taking the pressure from the German economy to continuously improve its innovative ability, quality and customer service.

- German consumers benefited from the devaluations of other countries until the introduction of the Euro. Imported goods and holidays became cheaper. Since the year 2000, this has changed, because the imports were more expensive and the same applies to the holiday.

- After the introduction of the Euro in 1999, the ECB had to adopt a middle course in its money monetary policy that, as it turned out, was the wrong one for all countries. The recession in Germany in the first half of the 2000s was therefore deeper and longer than it would have been without the Euro. The German government was forced to cut spending and implement labor market reforms that led to lower wages in Germany.

- In order to get the economy back on track after the recession in the first half of the 2000s, Germany relied on regaining international competitiveness over cost cutting rather than productivity improvement. Stagnating wages led to lower tax revenues while exports increased. Thus, the Euro has not „allowed“ Germany to make trade surpluses – the Euro has enforced them.

- German companies have profited from wage moderation and the debt-financed boom in the other European countries – in contrast to German employees and consumers.

- Due to weak economic performance following the introduction of the Euro, subdued tax revenues and persistently high costs of social benefits and reconstruction in the East, politics has begun to reduce spending on investment. This led to a further reduction in domestic demand in Germany.

- A trade surplus always goes hand in hand with a savings surplus. This led in Germany to a huge export of capital abroad. Partly as direct investment, but mostly as a loan to finance the debt boom in other countries. Little wonder that German banks have lost a lot of money in the US real estate market (the German Institute for Economic Research (DIW) estimates that in the course of the global financial crisis between 2006 and 2012 about €600 billion German foreign assets were lost).

- When the global financial crisis in Europe became apparent, German banks withdrew their money from the crisis countries. They were either replaced by public donors, as in Greece, where the Greek government debt was disposed in course of two debt cuts in 2012 from private creditors via ESM/ECB to the taxpayers of the Eurozone. These capital flows led to an increase in the TARGET2 claims of the Deutsche Bundesbank. In sum, the loans given by private banks – our savings – have been replaced by direct and indirect loans from the German government.

- With at least three trillion bad debt in Europe, it is certain that Germany, as the main creditor, will bear a large share of the losses. It is still unclear how this loss will be realized: through bankruptcy, orderly debt restructuring or monetization by the ECB. In any case, the main burden will hit the German citizen.

- All efforts to let the Euro survive through even lower interest rates, obviously lead to an expropriation of savers. Although a weak Euro may help the export industry again, for the man on the street it means higher costs due to rising import prices and reduces the effect of falling oil prices.

Daniel Stelter’s article concludes: „For the average German, the situation is as follows: The introduction of the Euro led to a long phase of low growth, high unemployment and wage stagnation. The days of cheap holidays in Italy and Greece were over. The state has cut spending on social services and infrastructure and investment. For its part, the economy had to focus on exports because domestic demand was depressed and savings were used to provide supplier credits. Now that these loans can not be paid, the German savers and taxpayers have to pay for the damage. Even worse, Germany is also criticized by the other countries. Against this background, the statement that we Germans are the main beneficiaries of the Euro is difficult to maintain. Without the Euro, the debt party in the southern Eurozone would not have existed, nor would the big export surpluses. Instead, we had a higher standard of living and better infrastructure in Germany.“

<END OF NOTE>

<END OF QUOTATION FROM THE WIRTSCHAFTSWOCHE ARTICLE FROM 08/2011>

FINAL REMARKS FROM MY END:

As stated earlier, the Euro primarily benefits export-oriented companies, speculators and over-indebted countries, while consumers, savers, tenants and taxpayers have to pay for the bill.

Despite these undesirable developments, attempts are repeatedly made to convert the Eurozone – despite deviating agreements in the EU treaties – into a transfer union, which would in particular require German taxpayers to bear even higher risks and burdens. These attempts also include French President Emmanuel Macron’s proposals in the autumn of 2017 for the „reform“ of the Eurozone, including an additional budget for the Eurozone, the introduction of EU-wide unemployment insurance or the introduction of an EU-wide deposit guarantee for bank savings accounts, as well as a call of 14 German and French economists in the German Frankfurter Allgemeine Zeitung (FAZ) published on July 10, 2018, under the heading „Future of the monetary union: further taboos must fall„, which contradicts the already mentioned call of the 154 German economists published on May 21, 2018, in the FAZ as well under the heading „The Euro may not lead to a liability union!„.

The fact that Emmanuel Macron’s proposals are not based on altruism but result from pure French self-interest is illustrated by the following four charts.

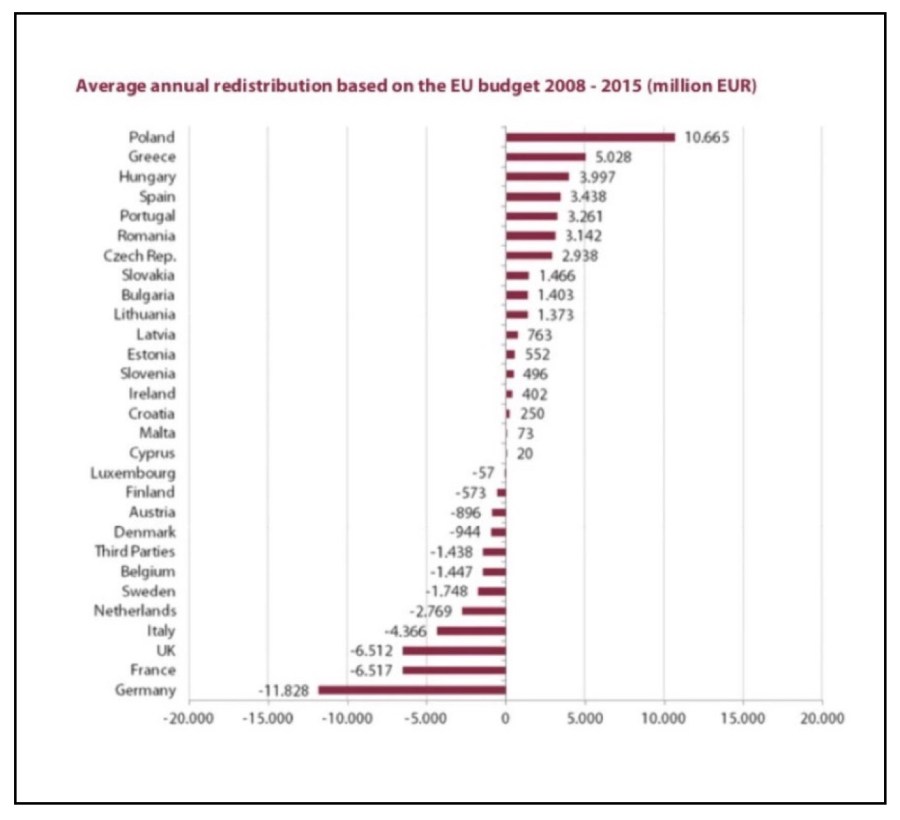

A study published by the Freiburg CEP institute in September 2016 under the heading „Redistribution between the EU member states“ revealed that hundreds of billions of Euro are being redistributed within the Eurozone via the European Investment Bank (EIB), the European Stability Mechanism (ESM) and the European Central Bank (ECB), in addition to the amounts redistributed under the European Treaties as part of the EU budget to foster convergence between the EU Member States.

The following chart from this CEP study illustrates that Germany, as a net contributor, payed €94.62 billion (net) to the EU budget over the 8-year period from 2008 to 2015, while Poland, as a net recipient, received €85.32 billion over the same period.

The EU budget for 2017 foresees a total of €157.86 billion in commitments and €134.49 billion in payments. According to „Facts and figures about the European Union„, these funds were used as follows:

- €74.89 billion (47.45%) commitments and €56.522 billion (42.03%) payments for „smart and inclusive growth“

- €58.584 billion (37.11%) commitments and €54.914 billion (40.83%) payments for „sustainable natural resources growth“

- €9.395 billion (5.95%) commitments and €9.395 billion (6.99%) Payments for „administration“

- €10.162 billion (6.44%) commitments and €9.483 billion (7.05%) Payments for „Europe in the world“

- €4.284 billion (2.71%) commitments and €3.787 billion (2.82%) payments for „Security and Union guarantee“

- €0.534 billion (0.3%) commitments and €0.390 billion (0.3%) Payments for „special instruments“

By comparison: Raising the minimum wage in Germany from €8.85 per hour by €0.35 per hour to €9.19 per hour from 2019 onwards will incur annual costs of approximately €2.0 billion.

Thomas Mayer and Oswald Metzger discuss in the already mentioned interview in Tichy’s Insight of June 30, 2018, under the heading „The ‚Lirazation‘ of the Euro“ the possibility of a dissolution of the Eurozone as follows.

Oswald Metzger: „In a debate about the explosive power of the Euro, Oskar Lafontaine’s former short-term Treasury secretary, Heiner Flassbeck, who sees Italian economic welfare in new debt, not in consolidation, told me: „If Germany does not like the Italian way, then should it please leave the Euro themselves, reinstate the Deutschmark, accept a 30 percent revaluation and reap more than three million unemployed.“ Is he even right in the end?“

Thomas Mayer: „Ultimately, it would be the solution if Germany steps out of the Euro through a parallel currency and leaves the Euro to the weak currency countries, which have already occupied it more or less anyway anyway. Then Germany would have the chance to disconnect from it. For the German industry this would mean that it would have to increase its effort again, because the German economy would have to achieve sales revenues through the quality of its products and services again and not with the help of a light currency, which ostensibly spurs export business, but slows down innovation and makes it sluggish. That’s why it would make sense for Germany to leave the currency area and simply leave the Euro in such a position.“

Thomas Mayer: „If that happens, then we would have a maybe 30% revaluation of the German parallel currency. As a reflection of the Italian proposals, the German state could then demand that taxes are being paid in this new currency. Companies would also have to earn money in this new currency, and of course citizens would, if they no longer want to take over the currency risk of the soft currency Euro. Thus, in addition to the Euro, a second cycle could emerge over time that would allow Germany to get away without total loss. The Bundesbank’s TARGET2 claims on the Eurosystem would then have been calculated in a new Deutschmark equivalent to approx. 70% of the existing amount. That would be quite a loss, almost €300 billion.“

Oswald Metzger: „At the moment, the Bundesbank’s target claims amount to just over €900 billion.“

Thomas Mayer: „If Germany lost €300 billion, that would be bitter. But still better than a total loss! But even if you ask well-meaning people in Berlin, then the answer comes in unison: „Never in life Germany will do that! We are the very last ones to leave the Euro.““

Political scientist Fritz W. Scharpf outlined in the IPG-Journal on December 26, 2017, under the headline „The southern Euro“ a suggestion how the Eurozone can be resolved in an orderly manner using the already existing European Exchange Rate Mechanism II (ERM II).

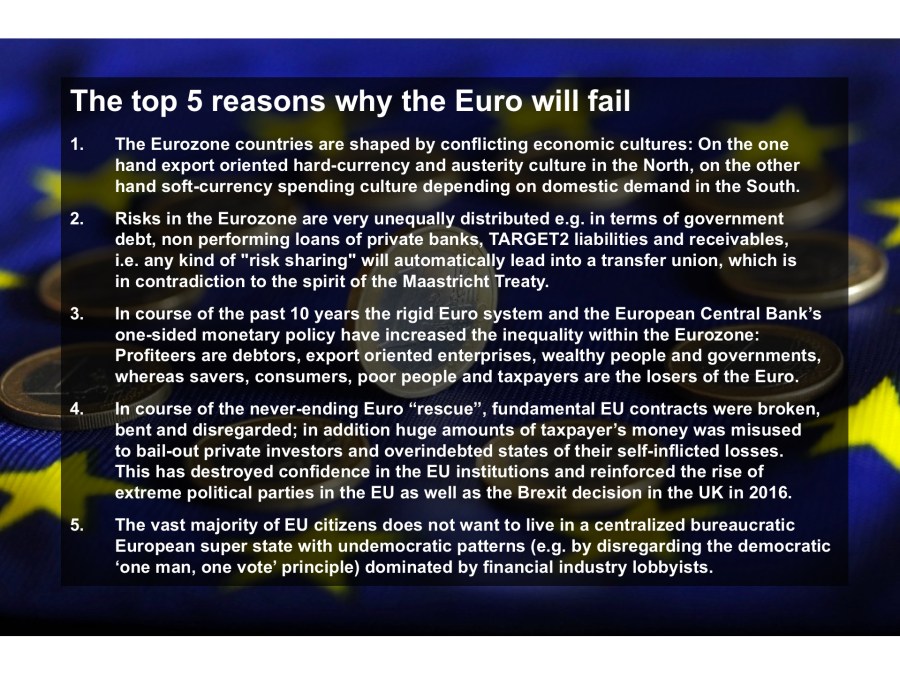

Personally, for the following reasons, I do not believe that the Euro will survive in the long term.

PS: Finally, I would like to recommend you five additional articles or blogs:

- Why German taxpayers, consumers and savers are the big losers of the Euro, you can read in my eponymous blog published on November 16, 2017: https://tivot.blog/2018/03/16/warum-deutsche-steuerzahler-konsumenten-und-sparer-die-grossen-verlierer-des-euro-sind/.

- The Viennese economic researcher and university lecturer Stephan Schulmeister published on his homepage in July 2018 a substantial and detailed analysis of the tension between neoliberal markets and politics under the heading „The right thing in the wrong: Defend the Euro!“, The conclusion of which I do not share, but which I still share warmly would like to recommend: http://stephan.schulmeister.wifo.ac.at/fileadmin/homepage_schulmeister/files/Euro_Blaetter_07_2018.pdf.

- One of the main root causes of inequality in developed countries seems to be the asymmetric growth of the financial and real economies. In 1970, both were still the same size, in 2015, the financial industry was almost four times larger than the real economy – see „Unequal land and its consequences“ published on May 11, 2018: https://kubraconsult.blog/2018/05/11/unequal-land-and-its-consequences/.

- This asymmetric growth has been caused and encouraged over the last 45 years by deregulation in connection with technological and financial innovations (including high frequency trading and massive expansion of derivatives trading) – see „Why Bitcoin & Co. are by far not the biggest problem in our global financial system“ published on November 29, 2017: https://kubraconsult.blog/2017/11/28/why-bitcoinco-are-by-far-not-the-biggest-issue-in-our-global-financial-system/.

- That these deregulations are not God-given can (or even have to) be reversed is stated in my blog from 2017 under the headline „Why the global financial industry must be regulated and enchained“: https://tivot.blog/2018/02/10/why-the-global-financial-industry-must-be-regulated-and-enchained/.

6 Kommentare zu „The life lies of the Euro“