NOTE: THIS IS AN AUTOMATIC TRANSLATION CREATED WITH GOOGLE TRANSLATOR. THE ORIGINAL BLOG IN GERMAN LANGUAGE CAN BE READ HERE: https://kubraconsult.blog/2018/05/08/ungleichland-und-seine-folgen/.

On May 7, 2018, the West German Broadcast (WDR) documentary „Unequal Land – How wealth turns into power“ caused heated discussions in social media and a passing noise in the German newspaper forest. The video can be viewed in the ARD-Mediathek. Since videos in the media libraries of the public broadcasters in Germany are always only temporarily available, you will find an alternative source on YouTube.

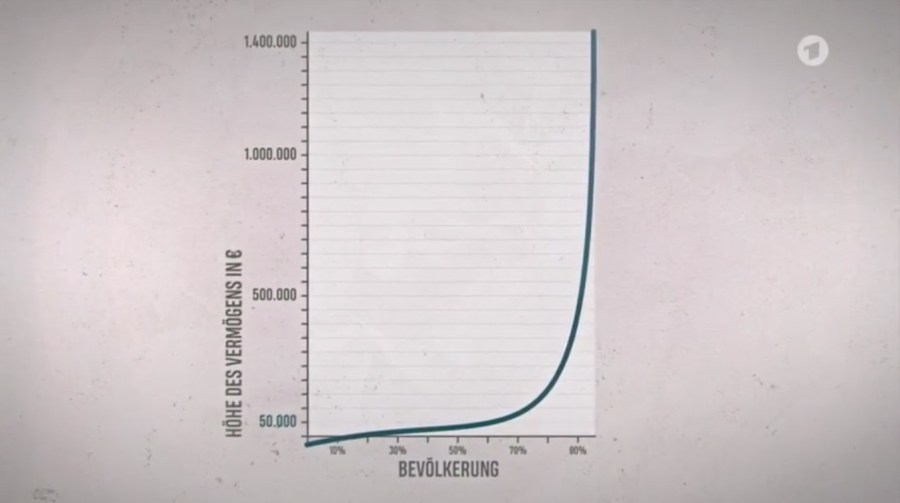

Basically, in my opinion, the authors of the documentation try to paint a somewhat factually neutral and fact-based picture of the distribution of wealth in Germany – including the difficult question of whether it is „fair“ if € 33 billion is owned by the richest German Family (Reimann) or if the 45 richest Germans with 214 billion € together have as much as the poorer half of the population in Germany, after all, consists of over 40 million citizens or if almost 60% of net wealth in Germany according to a OECD analysis owned by the richest 10 percent of Germans.

According to Credit Suisse’s Global Wealth Data Book, in 2016 Germany ranked 117th out of 172 countries in the inequality of wealth distribution with a so-called „Gini coefficient“ of 0.79 (0 = total equal distribution of money, 1 = one household owns everything, the rest nothing). 22 out of 28 EU member states have a less uneven distribution of wealth than Germany, which is at the level of Togo and Morocco. And the inequality in Germany is growing: in 2013, the Gini coefficient in Germany was still around 0.77. Note: At 0.29, the Gini coefficient for income distribution in Germany is much more balanced.

The following graphic from the WDR documentation illustrates this unequal distribution of wealth in Germany for 95% of the German citizens very vividly and impressively on the basis of a DIN A 4 sheet. Important note: The richest 5% of Germans no longer fit on the DIN A 4 sheet at the selected scale; Family Reimann floats for example, with its € 33 billion in 6.6 kilometers height above the x-axis in orbit.

The fact that wealth in Germany is not only disproportionately distributed but also significantly lower on average than in most other Western European EU member states had already been revealed in a study by the European Central Bank in 2013:

For many citizens, such findings are likely to run into incomprehension or create a sense of injustice – often followed by reflexive demands for a „wealth tax“ or greater taxation of inherited assets. Such demands in turn lead to violent resistance by the rich, wich for example point out that the richest 10 percent of households in Germany pay about 60 percent of income tax or that the majority of assets are in companies and that the profits from entrepreneurial activity are largely reinvested there. Of these, it is argued by the rich, indirectly benefit workers and employees and their families, through jobs and corporate taxes, which is basically true.

Note: If you want to conduct such discussions reasonably factual and goal-oriented, you have to differentiate at least between income and assets and with regard to assets between private assets and business assets. Furthermore, one should properly separate real assets and financial assets (I will return to this point shortly) and also the differentiation between self-acquired and inherited assets contributes to the objectification of ideological and emotional discussions.

Discussions about income and assets or their distribution in Germany are heavily mined areas. There is hardly a country in the world in which social envy and resentment towards the privileged and top performers of society are as pronounced as in Germany. For this reason, rich people in Germany avoid displaying their wealth too obviously.

An exception is Christoph Gröner, one of the largest German real estate developers with an estimated fortune of approximately € 80 million, who accompanied and filmed for half a year for the aforementioned WDR documentation. Christoph Gröner has worked his way up from petty-bourgeois backgrounds, has a correspondingly high level of self-confidence, and in the course of the WDR documentary he makes some provocative and informative remarks, for example, when he says, „If you have a big fortune, you can not destroy it through consumption. You throw the money out the window and it comes back in the door again. Or „We entrepreneurs are more powerful than politics because we are more independent“. Or „We live in the hottest society in the world. Anyone can do what they want here.“

At a speech in the context of a charity gala in favor of children in Berlin, Christoph Gröner expresses himself as follows (original quote): „We, the people who step on the gas, who have the time and the money, we have to get involved, we are the Country. We have one of the most beautiful countries in the world, we have the best options. Let us help to create equal opportunities for children, fair opportunities for children“. While the last two sentences testify to a thoroughly honorable attitude to society (in the sense of the German Constitution („Grundgesetz“) Article 14, paragraph 2, „property obligates“), the ordinary citizen must swallow involuntarily when listening to the first sentence „We, the people who step on the gas, who have the time and the money, we have to get involved, we are the state.“

It is precisely this sentence and its underlying self-perception that, in my view, leads us to the core problem of the very unequal distribution of income and wealth, namely the concentration of too much power and influence in the hands of a few and the consequent effects on state and democracy. Conversely, this concentration of power leads, inter alia, to a far-reaching powerlessness of democratically elected representatives of the people – especially when rich use the opportunities for their individual advantage, which open up to them in the course of a globalized economy across countries, state and city boundaries.

If countries, states or cities are played off against each other in order to negotiate the most favorable conditions and tax rates for investments, profits or assets, then from a legal point of view this may still be in order; from a moral or social point of view, one may consider it borderline. This is especially true of excesses, such as the „double Irish with a Dutch sandwich„, which helps large US companies push their taxes on profits in the European Union into a low single-digit percentage range or for tax avoidance and tax evasion in recent years as revealed by the International Consortium of investigative journalists under the terms „Panama Papers“ or „Paradise Papers„. Even with self proclaimed „philanthropists“ like George Soros, who build up substantial parts of his fortune through speculative financial bets on currencies (i.e., at the expense of countries and their citizens), there remains a stale aftertaste in my mouth when I read that such locusts open their heart and purse to bring benefits from her private casket to the people – best yet utilizing tax-saving foundations.

Despite this criticism, I still regard capitalism as the best economic and social order – especially if it succeeds in channeling this capitalism into the path of a „social market economy“ that takes into account the principle of „property obligates“ from the German Constitution („Grundgesetz“). People have different personalities, talents, strengths and weaknesses, and I see no other economic and social order that would be able, based on entrepreneurial initiative and a healthy profit motive, to provide work and prosperity, not just the entrepreneur himself, but also to the breadth of the citizens.

However, the WDR documentation describes a very questionable development that thwarted this goal. The following chart based on data from the book „Who owns the world“, published by the journalist Hans-Juergen Jakobs in 2016, illustrates that the relation between real assets and financial assets has shifted significantly between 1970 and 2017 – at the expense of real assets:

While in 1970 world real assets and financial assets were still roughly the same size, in 2017 real assets of $ 80 trillion had financial assets of a whopping $ 300 trillion – a ratio of 1 to 3.75.

This development is problematic insofar as real capital and financial capital usually pursue different, sometimes even conflicting, economic interests. Investing capital in goods markets focuses on investment, innovation, production and trade, while investing capital in financial markets is often short-term speculation. Real capital is interested in stable general conditions and must pay much more attention to balancing the interests of politics and society in order to be able to use well-trained workers and a modern and efficient infrastructure. Financial capital focuses on the highest possible returns, which can be achieved above all in unstable markets with high volatility or by betting against currencies or commodities to the detriment of the company.

The following four graphics from a presentation by Stephan Schulmeister from the Austrian Institute for Economic Research on May 4, 2017, summarize these differences and opposites quite well:

Let me give yet another example to illustrate the dimensions of the global financial system. The US website „The Money Project“ has set itself the goal of visualizing data and facts about money in a catchy and memorable way. On this site, there is an October 2017 article titled „All of the World’s Money and Markets in One Visualization,“ with a graphics that illustrates in which „aggregate states“ global capital is available (see: http://money.visualcapitalist.com/all-of-the-worlds-money-and-markets-in-one-visualization/). The graphics themselves is very good and impressive, but at the same time so big that I decided not to embed it in this blog.However, I would like to emphasize the following key facts:

- Total value of all coins and banknotes in the world = $ 7.6 trillion.

- Total value of 5.99 billion ounces of gold (already mined) or 187,200 tonnes = $ 7.7 trillion of gold (based on a spot price of $ 1,275 per ounce).

- Total value of (easily accessible) “ narrow money“ M1 in the world, including coins, banknotes and current accounts = $ 36.8 trillion.

- Market capitalization of all stock markets worldwide = $ 73 trillion, of which 38% are US, 11% Euro area, 5% United Kingdom, 10% China, 7% Japan and 29% the rest of the world (Note: China’s share has risen from 2% in 2015 to 10% in 2017, while the US share has fallen from 52% in 2015 to 38% in 2017).

- The total annual economic output of the national economies of all countries = approx. $85 trillion – the value added contribution of the four largest economies (USA, China, Japan, Germany) is over 50% (definition: gross domestic product (GDP) measures the production of goods and services within a country after deduction of all intermediate inputs; it is primarily a production measure).

- Total value of „broad money“ M3 in the world, including coins, banknotes, current account balances and long-term deposits on savings or deposit accounts = $ 90.4 trillion (Note: 8% of this global money stock exist physically and 92% only virtual as bits & bytes in computers).

- Global debt total = $ 215 trillion, representing 325% of global gross domestic product (GDP) (Note: $ 70 trillion of global debt, or 33%, has been built in the last decade alone), including $ 69 trillion -Dollar sovereign debt (current government debt figures by country breakdown see: https://www.nationaldebtclocks.org).

- The estimated total value of all developed real estate in the world (including residential real estate, offices, retail space, hotels, industrial sites, agricultural land and other commercial uses) = $ 217 trillion (Note: 21% of the world’s total real estate assets are in North America – despite the fact that only 5% of the population live there, while Europe holds 24% of the real estate assets, although only 11% of the population live there).

- Total value of all global derivatives, i.e. contracts between two or more parties deriving their value from the performance of an asset, index or other object (examples of derivatives are: futures, forwards, options, warrants, swaps) = 544 Trillions of dollars to $ 1.2 quadrillion.

For those of you who do not have to handle billions, trillions, or even quadrillions of dollars every day, here’s a comparison that illustrates the dimension of the numbers: One trillion is a „one“ with twelve zeros and a quadrillion a „one“ with fifteen zeros. Stacking four billion US $ 500 bills (equivalent to US $ 2 trillion), the stack reaches the height of the ISS, orbiting the earth about 400 kilometers above the surface. What do you estimate, what would be a stack of $ 544 trillion to $ 1.2 quadrillion? Small hint: We land somewhere halfway from the earth to the moon.

„Collateralized Debt Obligations (CDOs)“ and „Credit Default Swaps (CDS)“ are two types of derivatives that became dubious celebrities as the main cause of the recent global financial crisis from 2007-2008. Warren Buffet described them in 2003 as „financial weapons of mass destruction“ for a good reason.

Most of the derivatives are traded outside exchanges as „over-the-counter trades“ (OTC) between private investors. As a result, the overall system of derivatives trading, with its inherent risks, is largely intransparent to governments, central banks and regulators. Regulators are unable to monitor, let alone control, value flows and risks from derivatives trading.

Many financial professionals see derivatives trading as a „zero-sum game,“ as there is one winner and one loser for each bet (and nothing else is derivatives). Nevertheless, the sheer size of the system as a whole leaves incalculable risks to the global financial system and, consequently, to taxpayers.

Based on the average between the lowest and highest estimates for the total value of global derivatives in 2017 – i.e. $ 872 trillion – the total value of global derivatives is ten times the global annual economic output (GDP), nearly ten times the value of the „broad money“ M3 of the world (including coins, banknotes, current account balances, and long-term deposits on savings or term money accounts) or even nearly twelve times the market capitalization of all stock markets around the world.

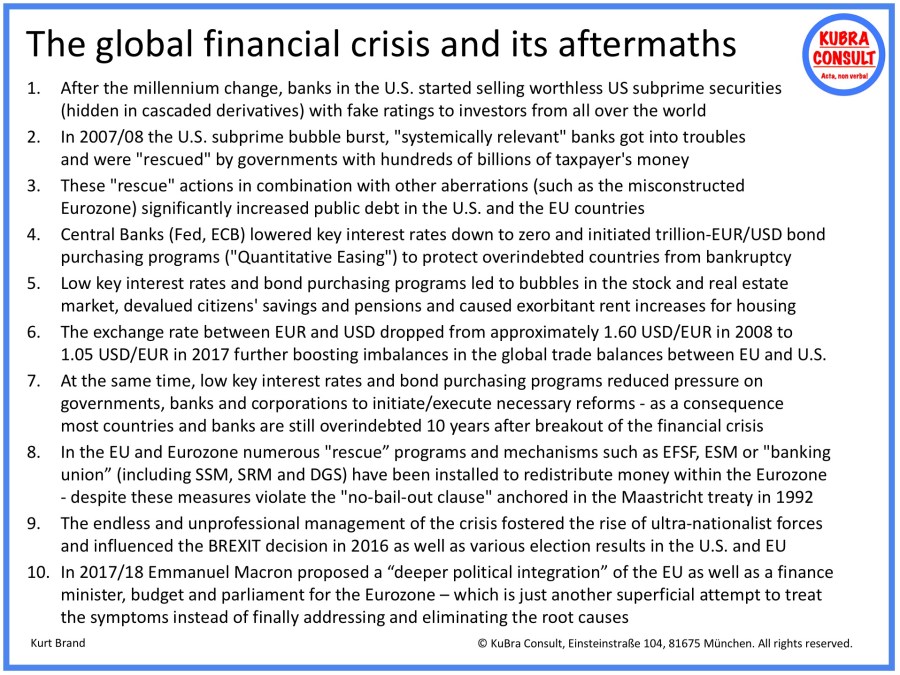

The sheer size and complexity of the global financial system is obviously a problem. In 2007/2008, this problem led to governments in the US and EU being forced to bankrupt „systemic“ banks and mortgage lenders with hundreds of billions of dollars in dollars or euros of risky mis-speculation these were classified as „too big to fail“ (incidentally, it turned out that almost all those responsible for this gigantic fraud were also „too big to jail“). The following graphic illustrates the still noticeable consequences of the last global financial crisis in Europe, the starting point of which was the bursting of the „subprime“ bubble in the USA from 2007/2008:

In the introduction to his above-mentioned book „Who owns the world“, the journalist Hans-Juergen Jakobs makes the following remarkable quote: „Behind the backs of large sections of the population and the public, such a phalanx of financial firms has established a dominant position in the globalized economy. It meets the concentrated capital of states such as China, Arab principalities and Russian oligarchs, who also want to expand in the economy, as well as the billions of pension funds and large family entrepreneurial dynasties, who are concerned with new products and new markets, but who also leave their money to specialists such as Larry Fink (CEO of Blackrock) for investment purposes. This neo-capitalism, controlled by financial markets, reflects a geostrategic competition in which money has the character of a weapon.“

And the British journalist and writer John Lanchester („The Capital“) said in 2012: „The financial system in its present state poses an existential threat to Western democracies that goes far beyond any terrorist threat. No democracy has ever been destabilized by terrorism, but if the ATMs stopped spending money, it would be an event of a magnitude that would put the currently constituted democratic states in danger of collapsing“.

SHORT EXCURSION:

Unfortunately, over the past 45 years, the world has had far too many inappropriate, immoral or even criminal incidents caused by the financial industry that have had a severe negative impact on the real economy. And in many cases, taxpayers had to pay the bill.

In this context, it is important to note that almost all the major instruments for short-term speculation or other financial manipulation with negative effects on our societies, have been invented, introduced or at least abused and perverted during the last 45 years as a result of fateful deregulation put into force by US Presidents Carter, Reagan, George Bush, Clinton and George W. Bush and various European heads of state (e.g. Margret Thatcher, John Major, Tony Blair, Helmut Kohl, Gerhard Schroeder).

The financial industry has used the leeway gained by deregulation to introduce, upgrade or expand instruments for short-term speculation and other financial manipulation, such as, e.g. computer-based high-frequency trading, short selling, hedging, speculation with commodities or against currencies based on long or short equity models, credit default swaps (CDS), asset backed securities (ABS) including collateralized debt obligations (CDO), tax-avoiding transactions using offshore centers and so on …

All these listed instruments are neither God-given, nor will the global financial system collapse if these instruments are strictly regulated or even banned. On the contrary, a substantial simplification of the global financial system and its instruments, combined with a harmonization and simplification of our tax systems would have a healthy and positive impact on the world economy. Under no circumstances should our world economy be a playground for unscrupulous players and weather. People who want to play and bet should satisfy their instincts in the casino with their own money at their own risk – and not with the global economy at the expense of taxpayers.

EXCURSION END

In addition to the sheer size and complexity of the global financial system, another problem – as mentioned earlier – is the concentration of power and influence in the hands of a few wealth managers.

In this context, I would first like to draw your attention to the development of the volume of assets managed by hedge funds. A hedge fund is an investment fund that is subject to few or no investment restrictions. Investors‘ money can be invested not only in equities or bonds, but also in derivative financial instruments (forward transactions). Short selling is also possible. This means that the fund management may sell securities on a forward basis that it does not even own at the time the contract is concluded. In addition, hedge funds try to generate a higher return on equity via debt financing (leverage effect). Overall, they are regarded as a type of fund that works with highly speculative investment techniques.

As the following STATISTA chart illustrates, that the assets managed by hedge funds worldwide increased by a factor of 28.6 between 1997 and the third quarter of 2017 – from 118 billion US dollars in 1997 to 3,374 billion US dollars in the third quarter of 2017. This gigantic volume is almost equivalent to Germany’s economic performance in 2017 as fourth largest economy in the world with a gross domestic product of 3.652 trillion US dollars.

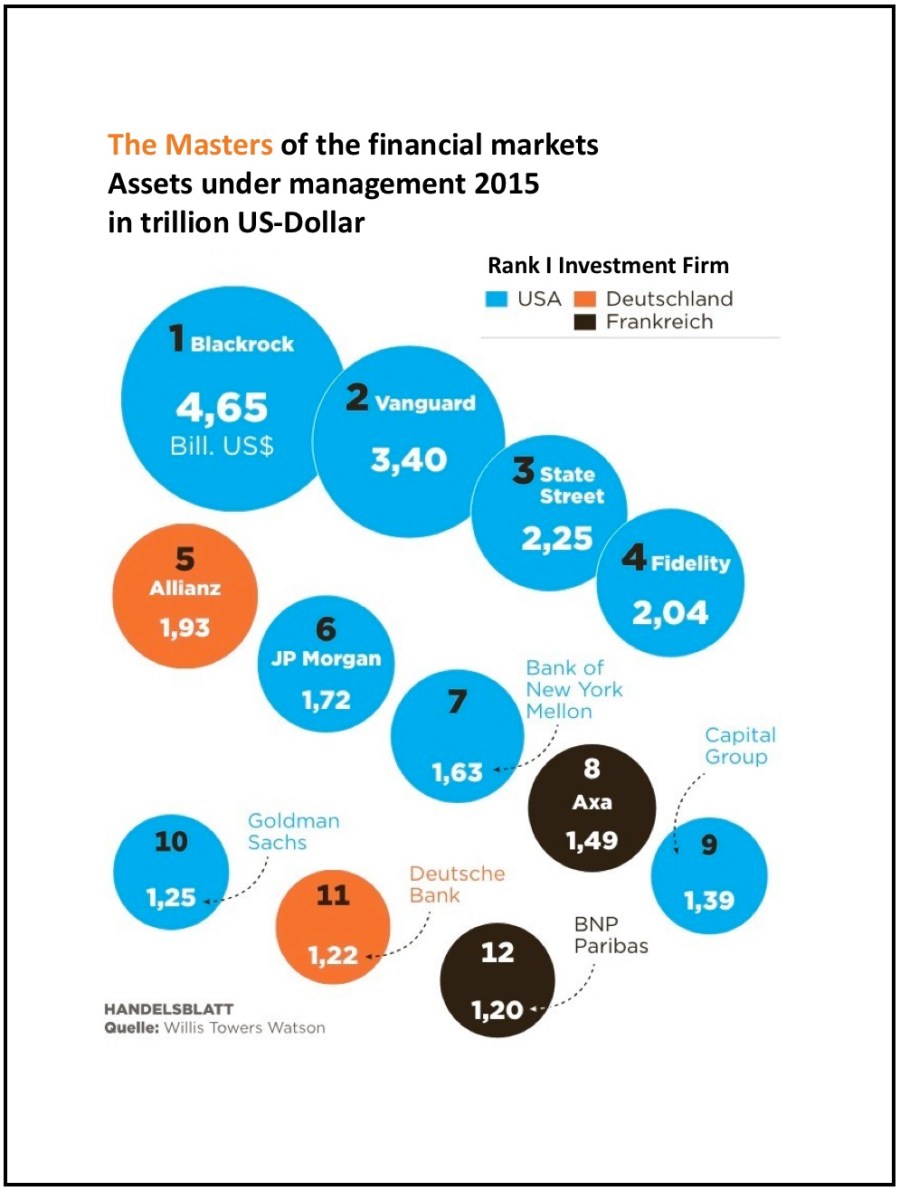

The following chart, which is also based on data from the book by the journalist Hans-Jürgen Jakobs, illustrates that the world’s 12 largest asset managers managed a massive fortune of $ 24 trillion in 2015 – that was about half of the 47 Trillions of dollars administered in the same year by the world’s 200 most powerful asset managers, fund managers, sheikhs, oligarchs and families.

Incidentally, in 2017/18, the assets managed by US market leader Blackrock have grown to $ 6.3 trillion. By comparison, the gross domestic product of the Federal Republic of Germany (i.e. the total value of all goods and services produced each year within the country’s borders and serving final consumption) was $ 3.652 trillion in 2017, making Germany the fourth largest economy in the world.

A very substantial and readable article under the (for my taste a bit too lurid) title „Blackrock: A money company on the way to global hegemony“ was published on May 8, 2018, by the German Tagesspiegel. In addition, I can only recommend to any interested reader Matt Taibbi’s article „The Great American Bubble Machine“ and „Secrets and Lies of the Bailout“ which describes in detail the influence of Goldman Sachs and the emergence of the global financial crisis in 2007/2008.

To get an insight into investment banking and its risks and consequences, I recommend thirdly an (unfortunately chargeable) interview with the Deutsche Bank economist David Folkerts-Landau in the German Handelsblatt published on May 21, 2018, a ZEIT article published on February 14, 2013, under the headline „Investment Banker: The Heritage after the Crash“ about Deutsche Bank board member Edson Mitchell and a SPIEGEL article from October 28, 2016 in English under the headline „The Deutsche Bank downfall: How a pillar of German banking lost its way“.

But how does this concentration of power and influence affect Germany? First, a few facts and figures.

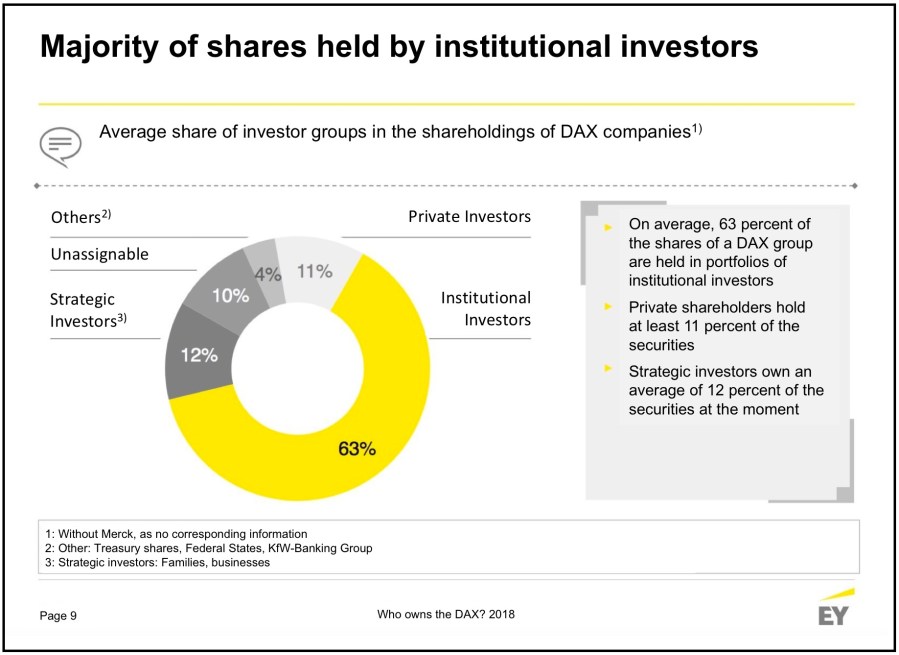

In April 2018, the auditing firm Ernst & Young has published a study titled „Who owns the DAX?„, from which the following chart is taken:

Key findings of this Ernst & Young study were:

- More than every second share of the DAX companies (54 percent) is foreign-owned. Compared to the previous year, the share of foreign investors has risen (by 1.3 percentage points), compared to 2005, foreign investors‘ exposure has actually risen sharply (by 12 percentage points).

- More than one in four shares (28 percent) is attributable to investors from other European countries, with one in five (21 percent) owned by investors from North America.

- Institutional investors are particularly involved in the DAX groups. They hold an average of 63 percent of the shares. Strategic investors such as families or companies have an average of 12 percent in their possession. The proportion of private investors is currently calculated at 11 percent, but is systematically under-reported, as private investors in surveys on shareholder structure are much harder to identify than institutional investors. It can therefore be assumed that a larger part of the non-allocable shares is owned by private shareholders.

- At the end of 2017, more than eight out of ten stocks (82 percent) of a DAX group were in free float, with only around 18 percent in the firm’s possession.

Domestic and, above all, foreign asset managers thus have a considerable influence on 30 largest public limited companies in Germany, many of whose jobs are affected by their development. Since the main interest of these asset managers is to maximize returns for their clients, it is difficult to imagine that asset managers will not use their influence to achieve the most favorable political conditions for the development of the assets they manage.

Der Tagesspiegel writes in the abovementioned article on May 8, 2018, „Despite all the warnings dares so far no EU government to tackle the impending cartel of money managers. „It undermines the principles of our market economy, but most politicians fear the influence of the giant and do not even dare to ask critical questions“, observed the longtime Liberal Democratic Party member of European parliament and today’s member of German parliament, Michael Theurer. Anyone looking for explanations meets an amazing phenomenon: Blackrock is itself a political power. The arms of the „money kraken“ reach into the governments. This already signals the symbolism in dealing with Larry Fink. When Fink travels Europe, he will be received like a state guest. Whether in Rome, Paris, The Hague or Athens, the Lord of the trillions always has a rendezvous with the head of state personally. „In the last few weeks, I had meetings with four heads of state,“ Fink boasted in April 2017 at the business channel Bloomberg TV.

Of course, concrete influence in practice should hardly be comprehensible. However, you can certainly ask for example, why income tax legislation in Germany is not radically simplified in order to make tax avoidance and evasion more difficult – corresponding proposals have been on the table since 2004/2005 (tiered tariffs of Kirchhof, Merz and Otto Graf Solms). Or why the tax liability in Germany is not coupled to citizenship, as other states including the US do. Or why there is still no financial transaction tax in the EU, despite years of discussions? Or why US platform companies, such as Google, Apple, Facebook, or Amazon, are allowed to pay only two percent of their worldwide tax burden in the EU by taking advantage of tax loopholes, although sales and profits from business in the EU are obviously much higher. Or why the German Federal Government has needed over 20 (!) Years to prevent the asocial multiple reimbursement of capital gains tax in the context of so-called cum-ex and cum-cum deals?

In the public discussion in Germany, the increasingly apparent division of society into „rage citizens“ („Wutbürger“) and „do-gooders“ („Gutmenschen“) in recent years is predominantly attributed to the decisions of the Federal Government under the leadership of Angela Merkel to deal with the refugee crisis in 2015. However, if you take a closer look, this split also has tangible economic causes – among other things, because the wealth gains generated in Germany over long periods of time were not distributed in a balanced manner. Key examples are listed in the graphic below:

The following three quotes are taken from a short Docupy video from May 2018:

Branco Milanovic (former Chief Economist of the World Bank): „If we look at globalization in the past 25 to 30 years, then we see: There are two groups of globalization winners. The first group is the already rich 1% of the world. They’re getting richer and richer. Especially interesting: the middle class in Asia, for example in India and China. Here, the income of 2 billion people has grown strongly. They are the winners of globalization. In contrast to the lower middle class of the industrialized nations in the USA and Europe. Their income is also stagnating in Germany. The group could be described as a „loser“ – although it hasn’t really lost anything. But it has not gained much from globalization either. These are the lower middle classes in Germany, the USA, Japan or France. „Your income has not grown in the last 20 years.“

Yascha Mounk (political scientist Harvard University): „We have managed to pull two billion poor people in India and China out of poverty. This is an incredibly positive development. But at the same time, of course, it’s true that the lower middle class, whether it’s in Mannheim or Michigan, hasn’t gotten very much in the last 20 years.“

Thomas Piketty (economist, Paris School of Economics): „In concrete terms, this means that if Europe fails to link globalization with the principles of social justice, there is a long-term risk of a break between globalization and the lower population groups.“

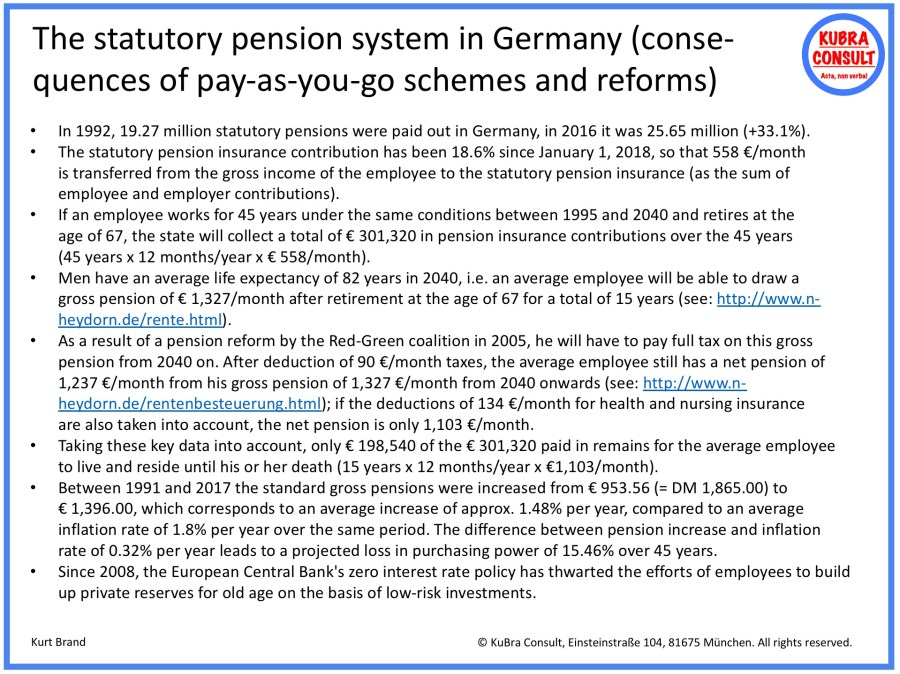

The economic causes mentioned above subsequently increase the risk for millions of workers in Germany to plunge into poverty among the elderly, as illustrated by the graph below (so far unfortunately available only in German language). 19.5 million workers in Germany, whose gross salary is less than € 2,330/month, can only count on a statutory pension at the basic level of € 795 (which is equivalent to approx. 44% of the current 44.16 million gainfully employed persons in Germany).

The contexts are admittedly complex and complex and are not exclusively under the influence of the financial system.

So, for example, the misconstructed Eurosystem led to structural divergences between the „Northern“ hard currency countries with their export-oriented economies and their „savings culture“ on the one hand, and the „Southern“ soft currency countries with their dependency on domestic demand and their „spending culture“ on the other hand. In this misconstrued compulsory corset, the unilateral monetary policy of the European Central Bank (ECB) to „rescue“ over-indebted countries in the South of the Eurozone with zero interest rates since 2008 and with purchases of government bonds and corporate bonds in the amount of several trillion euros since 2015, at the expense of savers, consumers and taxpayers in Germany.

The federal government’s inability to relieve its citizens through noticeable tax cuts is another problem – especially against the backdrop of an increase in federal tax revenues from € 190 billion in 2005 to € 312 billion in 2017 – an increase of € 122 billion or 64% per annum – the state’s financial leeway is not only increased by growing tax revenues, but also by lower interest rates, as the following list shows:

- As a result of the zero interest rate policy of the European Central Bank (ECB) German savers missed between 2010 and 2017 on balance (after deducting the interest benefits from lower interest rates) according to calculations of the DZ Bank around € 248 billion in interest (€ 436 billion interest disadvantage by escaping credit interest minus 188 billion interest savings through cheaper interest rates).

- The German state (federal, state and local governments) had tax revenues of € 452.1 billion in 2005. Over the next 12 years, these have risen to € 734.5 billion in 2017. The total tax revenues of the German state were therefore € 282.4 billion or 62% higher in 2017 than in 2005. By 2022, tax assessors expect an increase to around € 890.0 billion.

- In addition, the federal, state, local and social insurance funds have saved a total of € 240 billion over the nine years of 2008 and 2016 through the zero interest rate policy of the European Central Bank – an average of € 26.7 billion per year. In 2017, the savings amounted to € 47 billion.

- Taking into account the above-mentioned key data, the German state had a tremendous € 329.4 billion more leeway in 2017 than in 2005. Where did all the money go? And why do workers in Germany still have to bear the second highest tax burden under 35 OECD countries behind Belgium?

Overall, the following is the – from the citizen’s point of view – extremely sobering picture: German workers have to shoulder the second highest taxes and tax burden among 35 OECD countries behind the workers from Belgium – despite skyrocketing tax revenues in Germany, with € 734.5 billion in 2017 were € 282.4 billion higher than when Angela Merkel took office in 2005, where it was „only“ € 452.1 billion (+ 62.5%). As a result of the ECB’s zero interest rate policy, the government has saved € 240 billion in government debt interest rates (from 2008 to 2016), while citizens have missed € 248 billion in interest on balance (from 2010 to 2017: a disadvantage of € 436 billion resulting from credit interest % an advantage of 188 € billion from loan interest).

And the insincerity of the Federal Government in dealing with the unequal distribution and poverty risk of growing parts of the population (see following chart) has contributed to the division of society as well.

If decisions to rescue „systemically important“ banks or over-indebted Eurozone countries, which cause default and liability risks in the billions for the German taxpayer, be lashed under time pressure without adequate discussion by the German Bundestag, while an increase of the Hartz IV standard rates by € 7.00 per month causing much lower costs in the hundreds of millions is discussed in a way as it would lead to the downfall of the West, this, viewed from the point of view of the voters (and especially those affected), creates a fatal picture.

Conclusion:

The discussions that triggered the WDR documentary „Unequal Land – How wealth becomes power“ are important.

The discussions that triggered the WDR documentary „Unequal Land – How wealth becomes power“ are important. Thomas Fricke writes in a very readable SPIEGEL column on May 11, 2018:

„What causes bitterness? One explanation is that the citizens have been constantly preached that they should please take responsibility for themselves. What is crazy is when suddenly entire industries are swept away by cheap Chinese competition. Collective bitterness could also increase because 40 percent of the population has had little or no income growth in recent years, while others have their money increased on paradisiacal islands or still get a few billion dollars on top of it, even though they have tricked with diesel. Collective bitterness arises when, as ten years ago, money is suddenly there to save big banks after people have been told for years that unfortunately nothing is left over for pensions, schools and medicines. Or when suddenly laws apply according to which – mantra of personal responsibility – even people who have not had a new job for a year are threatened with falling to Hartz IV, who have worked hard for many years and cannot find a new job so quickly due to the banking crisis or general recession.“

This analysis hits the nail on the head and also shows that the consequences of inequality pose a threat to our democracy.

However, my optimism is limited that state and economy have a serious interest in correcting the misguided developments outlined. Why? Both benefit from it. And as long as broad sections of the population remain lethargic and indifferent and either do not participate in elections or repeatedly elect the same parties who are responsible for the occurrence of the undesirable developments described, there is little hope for a sustainable change of course.

The essential content of such a change of course would be obvious: massive investment in education and infrastructure, the establishment of a „sovereign wealth fund“ to supplement the breaking-away statutory pension system with a sustainable component, a radical simplification of the income tax system and the digital transformation of the country four concrete measures about whose meaningfulness there should be no discussions.

Moreover, from my point of view, a fundamental Eurosystem reform and effective measures to curb the power of the financial industry are indispensable to reduce short-term speculation without benefit to society and to promote long-term investment for the benefit of society. Both measures can not be implemented at national level by a German federal government – certainly not alone. I would like to emphasize, however, that these demands have nothing to do with utopia, socialism or class struggle, but serve to return the German Constitution („Grundgesetz“) Article 14, paragraph 2, „property obligates“ back its original meaning, that got lost due to the neoliberal „reforms“ in course of the past 45 years.

Because secure jobs that enable qualified workers to live well and properly with their families (even in the age of digitalization, automation and roboterization) are better and more social than any form of redistribution.

I would like to conclude this long blog with a quote from Gruenert & Whitaker that says: „The culture of any organization is shaped by the worst behavior the leader is willing to tolerate“.

Feedback and comments on this blog are, as always, very welcome.

P.S.: My attempt to describe the most important „socio-economic consequences of digitalization“ can be found in my blog of the same name published in March 2017: https://kubraconsult.blog/2017/03/17/the-socio-economic-consequences-of-digitalization/.

P.P.S.: A high-level concept, which illustrates how the digital transformation of our country can be organized effectively and which essential content should be considered in a digitalization strategy for Germany, can be found here: https://kubraconsult.blog/2018/02/21/digitalization-strategy-for-countries-using-germany-as-an-example/.

Loved reading thiis thanks