This article provides some facts, background information, context and considerations on the risk of derivative trading in general for the stability of the global financial system and consequently for the stability of the global economy as well as Deutsche Bank’s share in this market in particular. The text comprises mainly citations from publication in the Financial Times and other professional newspapers. The sources are mentioned at the end of each citation or paragraph.

Basic Definitions

A derivative is a financial security with a value that is reliant upon or derived from, an underlying asset or group of assets. The derivative itself is a contract between two or more parties, and the derivative derives its price from fluctuations in the underlying asset.

Key take aways:

- Derivatives are securities that derive their value from an underlying asset or benchmark.

- Common derivatives include futures contracts, forwards, options, and swaps.

- Most derivatives are not traded on exchanges and are used by institutions to hedge risk or speculate on price changes in the underlying asset.

- Exchange-traded derivatives like futures or stock options are standardized and eliminate or reduce many of the risks of over-the-counter derivatives

- Derivatives are usually leveraged instruments, which increases their potential risks and rewards.

Derivatives can be a useful tool for businesses and investors alike. They provide a way to lock in prices, hedge against unfavorable movements in rates, and mitigate risks—often for a limited cost. In addition, derivatives can often be purchased on margin—that is, with borrowed funds—which makes them even less expensive.

On the downside, derivatives are difficult to value because they are based on the price of another asset. The risks for OTC (over the counter) derivatives include counter-party risks that are difficult to predict or value as well. Most derivatives are also sensitive to changes in the amount of time to expiration, the cost of holding the underlying asset, and interest rates. These variables make it difficult to perfectly match the value of a derivative with the underlying asset.

Source: https://t1p.de/rptv

Difference between notional value and market value of derivatives

In market parlance, „notional value“ is the total underlying amount of a derivatives trade. The notional value of derivative contracts is much higher than the „market value“ or cost of a derivative due to a concept called „leverage“.

Leverage allows one to use a small amount of money to theoretically control a much larger amount. So, notional value helps distinguish the total value of a trade from the cost (or market value) of taking the trade, There is a clear distinction: the notional value accounts for the total value of the position, while the market value is the price at which that position can be bought or sold in the market place.

Source: https://t1p.de/algw

ABS, CDS and CDOs as „weapons of mass destruction“

In 2002, five to six years even before the outbreak of the global financial crisis in 2007/08, star investor Warren Buffett called derivatives “financial weapons of mass destruction.”

“In our view, however, derivatives are financial weapons of mass destruction, carrying dangers that, while now latent, are potentially lethal,” wrote Buffett in Berkshire Hathaway’s 2002 annual letter.

Source: https://t1p.de/hfee

The credit derivatives – ABS (asset backed securities), CDS (credit default swaps), and CDOs (collateralized debt obligations) – played a significant role in the development of the global financial crisis (which started as a default crisis in the US subprime housing market as of 2007/08) affecting both the financial and real economy. […] ABS are beneficial providing previously unavailable investment opportunities to market participants which facilitates the access to debt capital spurring real economic growth.

Source: https://t1p.de/hn71

A credit default swap (CDS) is a type of credit derivative that provides the buyer with protection against default and other risks – which means nothing else than that the buyer is able to take risks in a magnitude he could not afford under normal circumstances.

Credit default swaps came into existence in 1994 when they were invented by Blythe Masters from JP Morgan. They became popular in the early 2000s, and by 2007, the outstanding credit default swaps value stood at $62.2 trillion.

Source: https://t1p.de/2v6z

The first collateralized debt obligations (CDOs) to be issued by a private bank were seen in 1987 by the bankers at the now-defunct Drexel Burnham Lambert Inc. for the also now-defunct Imperial Savings Association. During the 1990s the collateral of CDOs was generally corporate and emerging market bonds and bank loans.

In the early 2000s, the debt underpinning CDOs was generally diversified, but by 2006–2007—when the CDO market grew to hundreds of billions of dollars—this had changed. CDO collateral became dominated by high risk (BBB or A) tranches recycled from other asset-backed securities, whose assets were usually subprime mortgages. These CDOs have been called „the engine that powered the mortgage supply chain“ for subprime mortgages, and are credited with giving lenders greater incentive to make subprime loans, leading to the 2007-2009 subprime mortgage crisis.

Source: https://t1p.de/sjbn

In the late 1970s, the college dropout and Salomon trader Lew Ranieri coined the term securitization to name a tidy bit of financial alchemy in which home loans were packaged together by Wall Street firms and sold to institutional investors. In 1984 Ranieri boasted that his mortgage-trading desk „made more money than all the rest of Wall Street combined.“

The good times rolled: as homeownership exploded in the early ’00s, the mortgage-bond business inflated Wall Street’s bottom line. So the firms placed even bigger bets on these securities. But when subprime borrowers started missing payments, the mortgage market stalled and bond prices collapsed. Investment banks, overexposed to the toxic assets, closed their doors. Investors lost fortunes.

Source: https://t1p.de/2rmj

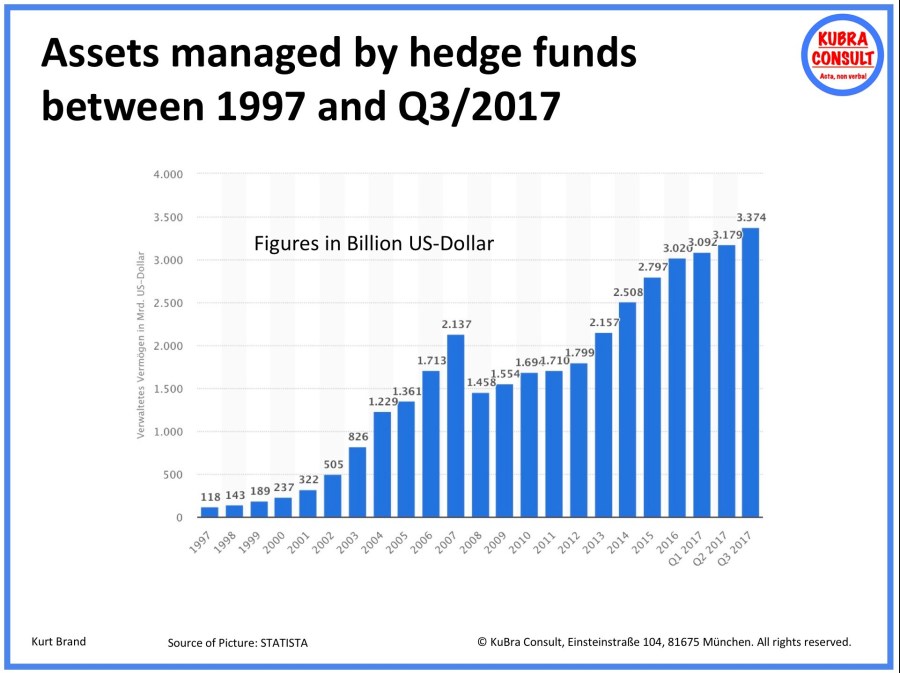

Since the turn of the millennium the trading volume of the derivatives markets exploded and reached unhealthy magnitudes which pose a threat to the stability of the global financial markets – not only due to the complexity of the instruments and the size of the market, but also to its lack of transparence and missing or ineffective regulations.

Facts and Figures: https://t1p.de/s0a4

In parallel, the volume of assets managed by hedge funds with high return targets compared to the market average multiplied between 1997 and 2017:

The world’s 12 largest asset managers managed a massive fortune of $ 24 trillion in 2015 – that was about half of the 47 Trillions of dollars administered in the same year by the world’s 200 most powerful asset managers, fund managers, sheikhs, oligarchs and families.

Incidentally, in 2017/18, the assets managed by US market leader Blackrock have grown to $ 6.3 trillion. By comparison, the gross domestic product of the Federal Republic of Germany (i.e. the total value of all goods and services produced each year within the country’s borders and serving final consumption) was $ 3.652 trillion in 2017, making Germany the fourth largest economy in the world.

Source: https://t1p.de/uzlm

Once a commodity is hooked on derivatives, producers lose a right to set prices — and there’s no way back. Derivative markets are not the efficient markets from economics textbooks. Centralization and focus on trading expectations and interpretations rather than real things make them prone to behavioral biases and manipulation. Worse, they make commodities an integral part of financial markets.

Source: https://t1p.de/0g2z

The role of Deutsche Bank as major player in the derivatives market

At the beginning of July 2019, Deutsche Bank announced a new „strategic transformation“ after a decade of woeful underperformance. The headline-grabbing figure was 18,000 — the number of jobs it expects to cut as part of the restructuring.

[…]

But of course, it’s a large bank. So that means it poses systemic risks. Which means bad news for everyone, or something. So cue a pack of market bears over the weekend speculating over the bank’s long-term health, and what it might mean for the broader market.

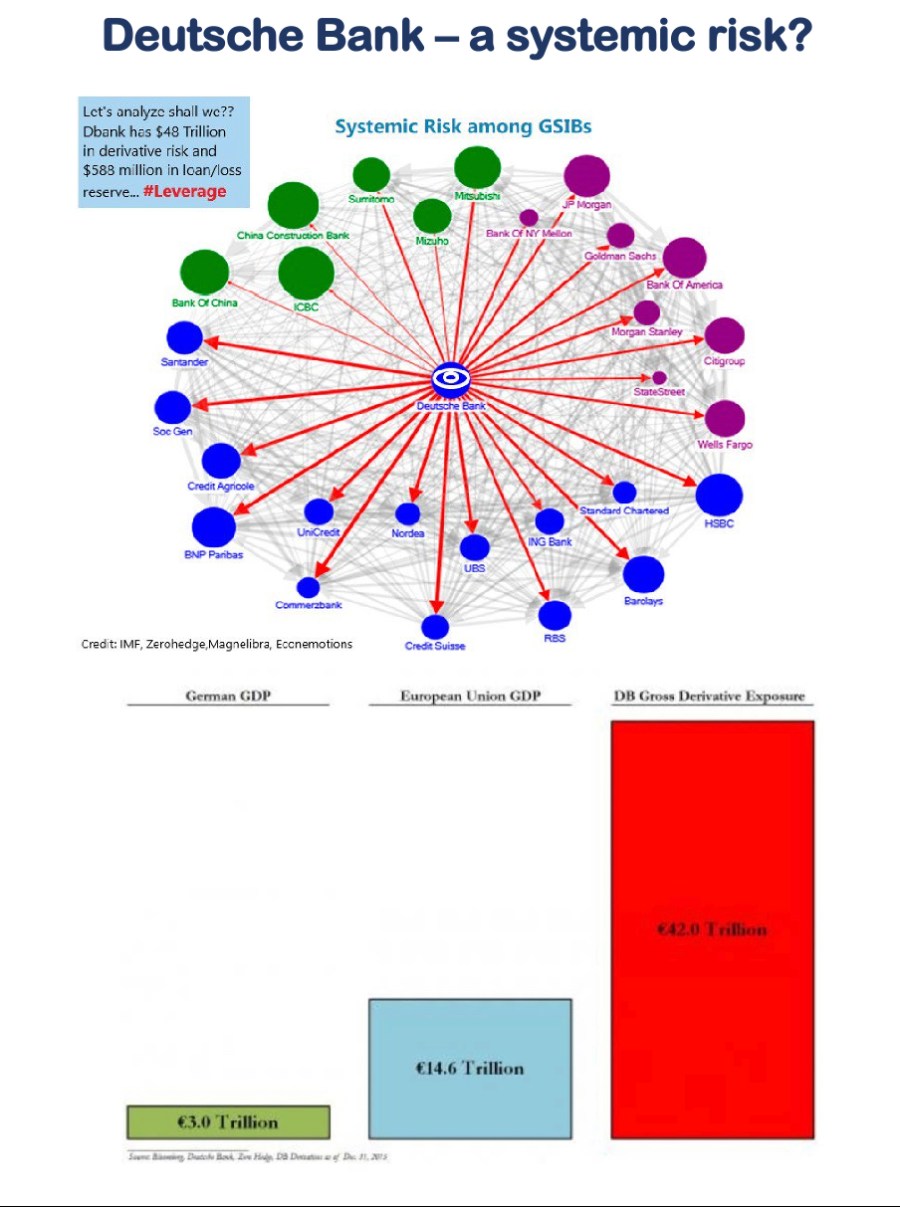

And that means, of course, citing Deutsche Bank’s notional derivative exposure, which as of Dec 31 2018, according to the bank’s annual report, stood at a terrifying €43.5 trillion (in German: „Billionen“).

Source: https://t1p.de/207j

As the following chart illustrates, €43.5 trillion is almost three times the European Union’s GDP of €14.6 trillion (including the UK) and almost 15 times the German GDP of €3.0 trillion.

As a result of the collapse of the stock markets in the wake of the Corona crisis in March 2020, Deutsche Bank’s share price fell temporarily to an all-time low of €4.45, so that Deutsche Bank’s market capitalization fell to just €9 billion. For € 4.5 billion plus 1 share, a competitor or a hedge fund could have acquired one of the former top 4 global systemically important banks (GSIB) according to the U.S. Financial Stability Board (FSB) ranking.

To set this market capitalization into a meaningful context: Apple Inc., for example, achieved a profit of around $55.3 billion in the 2019 fiscal year (from October 2018 to September 2019), which corresponds to approximately €49 billion. An amount of €4.5 billion is for Apple the famous „peanuts“, which the company earns in just over a month.

But Deutsche Bank was not taken over. And the reasons are most likely the risks on the balance sheet of Deutsche Bank.

2019 FSB list of GSIBs: https://t1p.de/pv12

Key data on Deutsche Bank’s stock: https://t1p.de/3aab

Refutations and relativizations

The derivatives market is, in a word, gigantic – often estimated at more than $1.2 quadrillion on the high end. How can that be? Largely because there are numerous derivatives in existence, available on virtually every possible type of investment asset, including equities, commodities, bonds and foreign currency exchange. Some market analysts even place the size of the market at more than 10 times that of the total world gross domestic product (GDP).

Other analysts argue that such a calculation doesn’t reflect reality – that the notional value of a derivative contract’s underlying assets, the financial instruments the derivative is pegged to, does not accurately represent the actual market value of derivative contracts based on those assets.

According to the most recent data from the Bank for International Settlements (BIS), the total notional amounts outstanding for contracts in the derivatives market is an estimated $542.4 trillion. But the gross market value of all contracts to be significantly less: approximately $12.7 trillion.

When the actual market value of derivatives (rather than notional value) is the focus, the estimate of the size of the derivatives market changes dramatically. However, by any calculation, the derivatives market is quite sizable and significant in the overall picture of worldwide investments.

Source: https://t1p.de/twum

The issue with banging on about Deutsche Bank’s notional derivative exposure, as ex-IMF economist Mark Dow pointed out […], is that the German business’s net exposure is infinitesimal compared to the notional number. The total in Deutsche’s report represents positions both long and short positions including hedging transactions.

Indeed, according to the International Swaps and Derivatives Association, the gross credit exposure of over-the-counter derivatives, which “ is a more accurate measure of counter party credit risk“, was just $2.3tn for the entire market at the end of 2018, a decline of 0.4 per cent from 2017.

So unless you think Deutsche’s risk management is so bad that it would expose €61.3bn of capital to €43.5tn of unhedged derivative positions, perhaps it’s time to start looking elsewhere for a market event that will pull the plug on the longest equity bull market in history.

Source: https://t1p.de/207j

Conclusions

You may question the downplaying refutations and relativizations provided by the Financial Times and the Bank for International Settlement. If a hedge fund pays $100 million to secure the default of an investment over $1 billion by means of derivatives, the counter parts of the derivative deal must compensate the $1 billion in case the default materializes. And at least in times of market crashes and disruptions where trading algorithms determine, which assets are bought and sold how quickly, the related risks in an intransparent, cascaded system can quickly become unmanageable.

While in 1970 world real assets and financial assets were still roughly the same size, in 2017 real assets of $80 trillion were facing financial assets of a whopping $300 trillion – a ratio of 1 to 3.75. This development is problematic insofar as real capital and financial capital usually pursue different, sometimes even conflicting, economic interests.

Investing capital in goods markets focuses on investment, innovation, production and trade, while investing capital in financial markets is often short-term speculation. Real capital is interested in stable general conditions and must pay much more attention to balancing the interests of politics and society in order to be able to use well-trained workers and a modern and efficient infrastructure. Financial capital focuses on the highest possible returns, which can be achieved above all in unstable markets with high volatility or by betting against currencies or commodities to the detriment of the company.

Source: https://t1p.de/uzlm

In course of the last 45 years we have seen far too many asocial, immoral or even illegal incidents caused by the financial industry with strong negative impact on the real economy. In many cases the taxpayers had to pay the bill. The list includes the burst of the US Subprime bubble in 2007/2008, the crash of the dot-com bubble in 1999/2000; the Asian crisis in 1997/98 caused by hedge funds (e.g. of the self-appointed „philanthropist“ George Soros); provision and management of illegal or at least immoral tax shelter schemes with or without utilization of Offshore Centers; deliberate bypassing of laws e.g. by cum-ex and cum-cum trades („dividend arbitrage“) to achieve an unrightful multiple reimbursement of capital gains; criminal manipulations of the LIBOR (London Interbank Offered Rate); huge manipulations of commodity prices (e.g. for oil, corn, coffee, cocoa, wheat) utilizing speculative bets with futures, e.g. by Goldman Sachs; manipulation of stock prices e.g. by high-frequency trading or short-selling starting around 1985 and massively expanded around 2000 depending on the availability of high-performance computer trading systems and complex trading algorithms; bypassing of existing financial regulations – the traditional Banking Sector has to comply with – by the Shadow Banking Sector comprising e.g. Asset Management companies (such as BlackRock, Vanguard or Fidelity), Private Credit Funds (such as Goldman Sachs Mezzanine, TCS Direct Lending Fund or KKR Lending Partners) or Crowdfunding platforms (such as Kickstarter, GoFundMe or Indiegogo); currency swaps designed by Goldman Sachs to disguise the real economic situation of Greece, which allowed the country to join the Euro Zone effective January 1, 2001; transfer of debt risks in a magnitude of several hundred billion Euro resulting from Greek national debt from private „investors“ to tax payers of the Euro Zone between 2010 und 2012; or unprecedented manipulations of the Euro currency rate performed by the European Central Bank (ECB) in a magnitude of €2.6 trillion (i.e. more than the GDP of France, Italy or Spain) in form of the „Quantitative Easing“ Program causing fatal negative side effects for small savers and old-age pensioners and taxpayers.

The aforementioned list is by far not complete. Worth reading to gather more comprehensive and detailed information are for example Matt Taibbi’s articles „The Great American Bubble Machine“ (https://t1p.de/m11g) and „Secrets and Lies of the Bailout“ (https://t1p.de/mtfa).

In this context it is important to know, that almost all of the major instruments for short-term speculations or other financial manipulations with negative impact on our societies have been invented, introduced or at least misused and perverted in course of the last 45 years as consequence of fateful deregulations approved by the US-Presidents Carter, Reagan, George Bush, Clinton and George W. Bush and various political leaders in Europe (e.g. Margret Thatcher, John Major, Tony Blair, Helmut Kohl, Gerhard Schröder).

The financial industry utilized the massively expanded leeway provided by this deregulations by introducing, upgrading or broadening various instruments for short-term speculations or other financial manipulations such as high-frequency trading, short-selling, hedging, speculations with commodities or against currencies based on long and short equity models, Credit Default Swaps (CDS), Asset Backed Securities (ABS) including Collateralized Debt Obligations (CDO), tax-avoiding transactions with Offshore Centers and so on …

All the listed instruments are neither God-given, nor will the global financial system collapse if these instruments become strictly regulated or even prohibited. In contradiction: A significant simplification of the global financial system and its instruments in combination with a harmonization and simplification of our tax systems will have a healthy and positive effect on our global economy.

Our global economy should by no means be a playground for unscrupulous gamblers and bettors. People, who want to gamble and bet, should satisfy their lucid drive in a gambling house with their own money and at their own risk and not at the account of taxpayers.

The negative consequences of these asocial, immoral or illegal behaviors of the global financial industry on our societies, economies and democracies are huge and disastrous. They cause unhealthy huge imbalances in the distribution of income and wealth, bubbles in the stock, real estate and commodity markets and are the worst role model for the man on the street, you can think of.

Source: https://t1p.de/qqli and https://t1p.de/3hqx

If I was in charge of the government, I would tax short term speculations without benefit for the society with more than 80 percent and long term investments with benefit for the society with less than 20% taxes. There is more capital than dirt on planet earth, however, if we want to turn the world into a better place, we need to make sure that „big money“ flows into the right directions and „big tech“ focusses on the right matters, where both deliver the highest impact for the UN’s sustainable development goals – and not where greedy individuals receives the highest profits.

So, are derivatives a systemic risk for the global economy? I look forward to the comments of advocates and profiteers of this business.

6 Kommentare zu „Derivatives as systemic risk for the global economy?“